Can AMD’s TensorWave gamble turn AI infrastructure ambition into durable demand, or is Wall Street right to punish the stock first?

What Does AMD TensorWave Funding Mean for Wall Street?

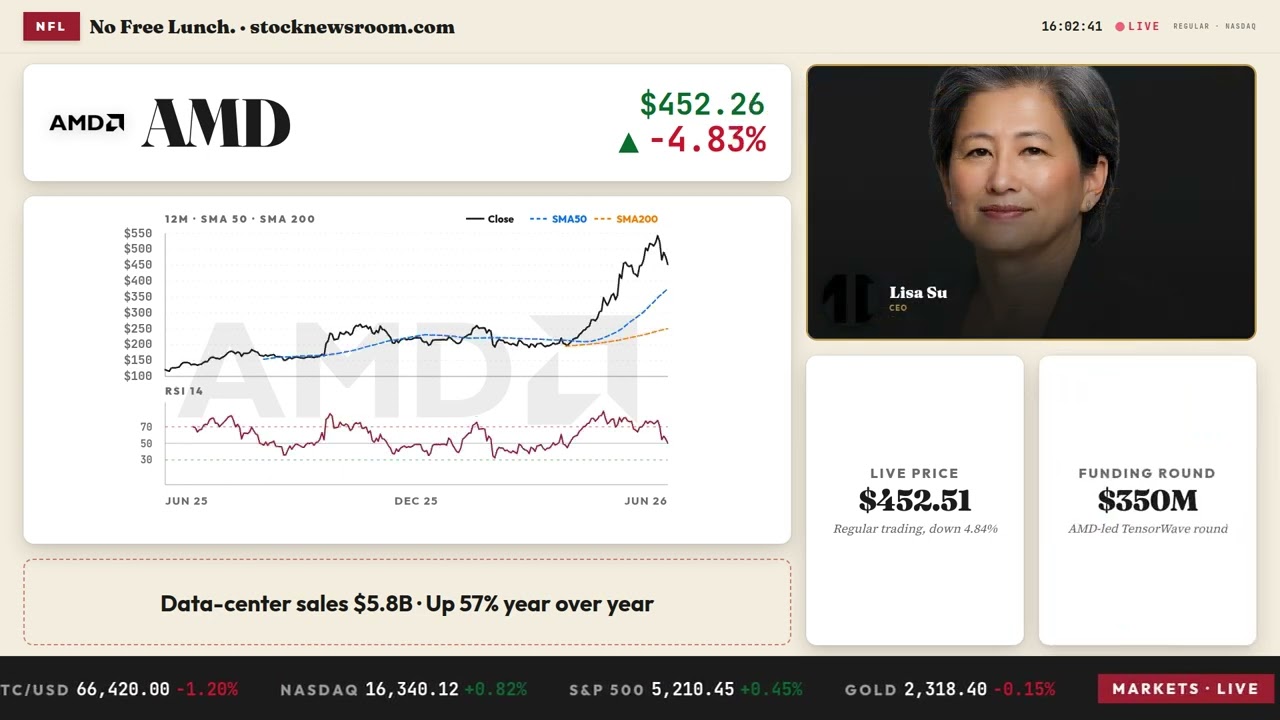

Advanced Micro Devices, Inc. has led a $350 million funding round for TensorWave, a Las Vegas-based cloud-computing startup exclusively deploying AMD hardware. Valued at $1.55 billion, TensorWave plans to scale from 500 megawatts to two gigawatts of data-center capacity — a strategic counterweight to NVIDIA-backed CoreWeave and Nebius. Unlike NVIDIA’s neoclouds, which already operate over one gigawatt, TensorWave remains early-stage. Still, the AMD TensorWave Funding move signals a decisive pivot: AMD is no longer just selling chips — it’s locking in demand, controlling stack integration, and building infrastructure moats. The timing is notable: the deal closed just as Broadcom’s softer AI guidance triggered a broad semiconductor selloff, pulling AMD down 4.99% to $451.76 — though pre-market rebounded 3.53% to $467.70.

How Does This Compare to NVIDIA and Meta?

While NVIDIA dominates AI training with an ~80% data-center GPU share, AMD is gaining traction in inference and agentic AI — where its chiplet-based EPYC CPUs and MI450 GPUs offer memory- and efficiency-optimized advantages. Meta Platforms has already committed to deploying 6 gigawatts using AMD hardware, and OpenAI has signed a parallel agreement. That’s a stark contrast to NVIDIA’s reliance on hyperscalers for demand validation. Still, AMD’s $108.7 trailing P/E remains nearly triple NVIDIA’s $36.1 multiple — a valuation gap analysts say reflects execution risk, not just growth potential. RBC Capital Markets recently reiterated its ‘Outperform’ rating on AMD, citing the MI450 ramp and Helios rack architecture as key catalysts for 2027 data-center revenue growth of over 80%.

Is the Chip Sector Correction Temporary or Structural?

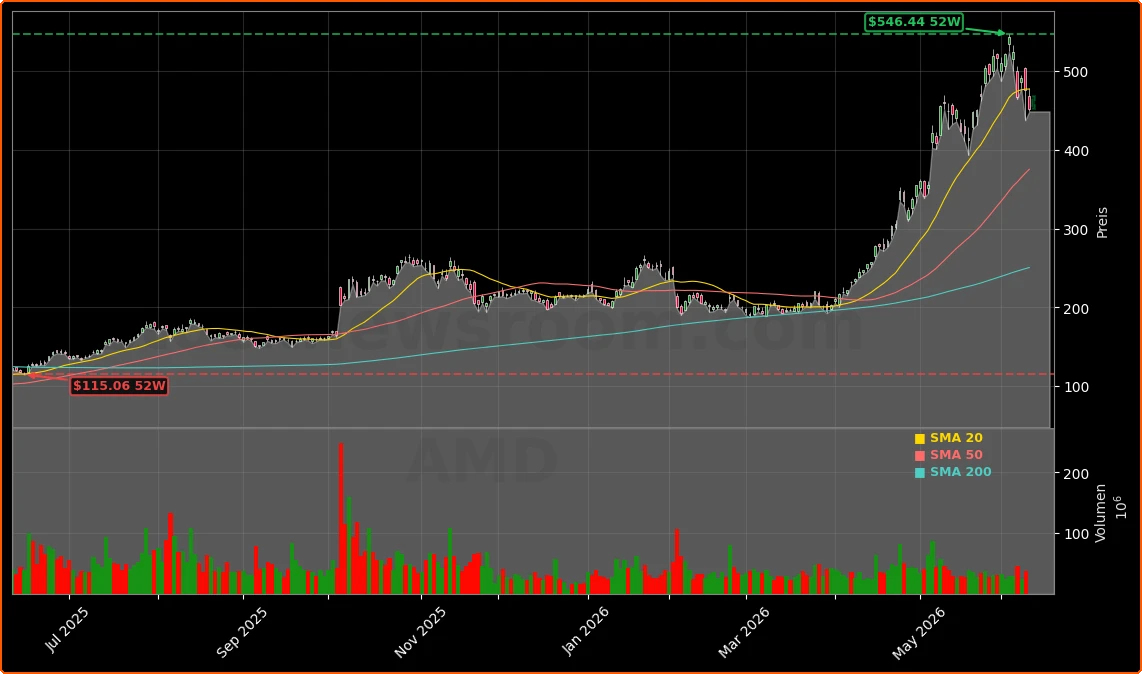

Wednesday’s selloff wasn’t isolated: Broadcom (AVGO), Micron, and Tesla all declined alongside AMD, as the VIX spiked 26% in one week to 19.87. The iShares Semiconductor ETF (SOXX) fell 1%, reflecting broad risk-off sentiment — particularly for high-multiple AI enablers. Yet fundamentals remain strong. AMD’s fiscal Q1 2026 revenue hit $10.25 billion — up 38% YoY — with data-center sales surging 57% to $5.8 billion. Analysts at Barclays raised their price target to $665.00, TD Cowen to $600.00, and Mizuho to $615.00 — all on June 1. Their consensus price target now stands at $475.17, implying ~5% upside from current levels. Still, as Morningstar strategist Brian Colello noted, investors remain wary of ‘circular financing’ dynamics — even as AI infrastructure demand surges globally.

What’s Next for AMD’s AI Infrastructure Strategy?

Anyone scarred by the dot-com bubble bursting is keenly aware of the risks of a circular deal in which firms pass funds back and forth to prop up a business… we don’t think this risk is present today, and we’re skeptical this will occur in the long term, since AI demand is both real and booming, but it bears watching.— Brian Colello, Morningstar

Beyond TensorWave, AMD is expanding its AI platform stack. Its partnership with Oriole Networks — integrating photonic interconnects into the Scaling Inference Lab — aims to slash data-center network power use by up to 81% and reduce GPU idle time to under 1%. Commercial rollout is slated for 2027. Meanwhile, Samsung collaboration on HBM4 memory and expanded cloud deployments with AWS, Google Cloud, Microsoft Azure, and Tencent reinforce AMD’s full-stack ambitions. The AMD TensorWave Funding is just one node in a broader architecture: from silicon to software to infrastructure. With 12-month returns still up 285.84%, AMD remains one of the strongest performers in the NASDAQ — even as it navigates valuation scrutiny and competitive pressure from NVIDIA and Apple’s growing in-house silicon efforts.