Can Broadcom AI Infrastructure turn a post-earnings selloff into a much bigger long-term AI platform win?

Why Did Broadcom Stock Drop After Strong Earnings?

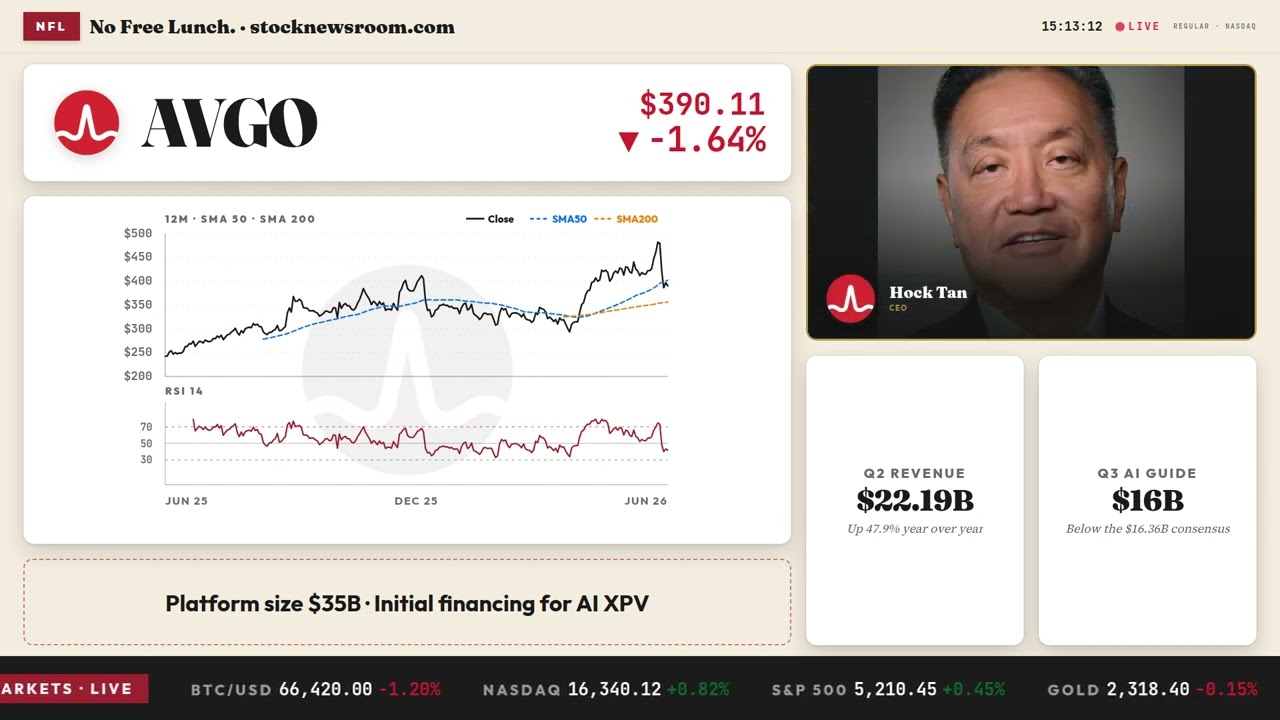

Broadcom Inc. shares fell 13.78% over the week ending June 5 despite delivering fiscal Q2 revenue of $22.19 billion — up 47.9% year over year — and AI semiconductor revenue of $10.8 billion, a 143% surge. The selloff wasn’t about performance; it was about optics. Management maintained its $100 billion AI revenue target for fiscal 2027 rather than raising it, and guided Q3 AI revenue to $16 billion — slightly below the $16.36 billion consensus. For investors pricing in relentless acceleration, the unchanged outlook triggered a rotation out of mega-cap AI names. The Nasdaq dropped 2.06% on Tuesday, and semiconductor ETFs like SOXX shed 7%, pulling down Meta, NVIDIA, and Tesla by association.

What Does the $35 Billion AI XPV Platform Mean for Broadcom AI Infrastructure?

The answer lies in execution — and scale. On June 9, Broadcom Inc. announced the AI XPV Platform with Apollo and Blackstone, an initiative backed by an initial $35 billion to finance over 20 gigawatts of AI compute capacity through 2028. The first tranche will fund Anthropic’s 1-gigawatt expansion at Fluidstack-operated sites starting mid-2026. Crucially, this isn’t just financing: it embeds Broadcom’s custom AI chips, networking silicon (including Tomahawk 6), and VMware Cloud Foundation software into the stack. As Wall Street Journal reported, the platform merges long-term capital with Broadcom’s roadmap to lower AI training and inference costs — a direct response to enterprise concerns over public cloud economics.

How Is Broadcom AI Infrastructure Reshaping Enterprise Cloud Strategy?

Enter the Private Cloud Outlook 2026 report — published the same day — which documents a decisive shift: 56% of enterprises now run or plan to run production AI inference on private cloud, up from 41% on public cloud. Cost has overtaken security as the top public cloud concern (31% vs. 26% in 2025), and 97% of IT leaders believe some portion of their public cloud spend is wasted. Broadcom’s VMware Cloud Foundation division is now central to this pivot, enabling secure, sovereign, and cost-predictable AI deployments — especially in financial services, healthcare, and public sector. This isn’t a niche: it’s the foundation of Broadcom AI Infrastructure’s next $50 billion growth wave.

How Do Analysts View Broadcom’s AI Trajectory Now?

Despite the volatility, analyst conviction remains strong. Bank of America Securities reiterated its Buy rating and raised its price target to $530 on June 4. Mizuho upgraded its rating to Outperform and lifted its target to $530. UBS maintained Buy but adjusted its forecast to $485. The consensus price target stands at $513.68 — implying roughly 29% upside from Tuesday’s $391.84 close. Citigroup analyst Atif Malik called the selloff a healthy correction and reaffirmed his positive view on Broadcom Inc., noting its unmatched integration of custom ASICs, networking, and infrastructure software. With 44 analysts issuing Buy or Strong Buy ratings and zero Sells, the Street sees today’s pullback as mispricing — not a fundamental reset.

What’s Next for Broadcom AI Infrastructure and Wall Street?

The path forward hinges on two near-term catalysts: Q3 execution against the $29.4 billion revenue guide and tangible evidence of customer diversification beyond the current six core partners — Google, Meta, OpenAI, Anthropic, Microsoft, and a sixth unnamed hyperscaler. Broadcom’s bookings-to-shipments ratio remains highly favorable at over 3:1, and free cash flow hit $10.26 billion last quarter — 46% of revenue. With Apollo and Blackstone now de-risking infrastructure deployment, Broadcom AI Infrastructure is no longer just selling chips; it’s enabling the entire AI stack. For S&P 500 and NASDAQ investors, this is a structural upgrade — not a cyclical play.

Related Coverage: Broadcom’s earnings report triggered Wall Street’s first real pause in AI infrastructure spending — but the rebound is already underway. Broadcom Earnings +2.8% After AI Demand Warning Shook Tech analyzes how the selloff exposed valuation sensitivity, not demand weakness. Meanwhile, SiliconANGLE’s deep dive on Broadcom’s private cloud strategy explains why enterprises are repatriating AI workloads — and how Broadcom’s VMware integration is capturing that shift. Finally, The Wall Street Journal’s coverage of the AI XPV Platform confirms this is the largest coordinated infrastructure financing of its kind — and a watershed moment for AI capital markets.

“We are at a historic inflection point where the demand for AI compute is fundamentally reshaping the global economic landscape.”— Hock Tan, CEO of Broadcom Inc.

Broadcom AI Infrastructure has moved decisively beyond component supply into full-stack enablement. For investors, this means exposure to both AI compute growth and enterprise infrastructure modernization — two of Wall Street’s most durable secular trends. The next quarterly earnings will confirm whether the market’s skepticism has cleared — and whether Broadcom Inc. can convert $35 billion in capital into $100 billion in AI revenue. With strong technical support near $324.50 and a buy-rated consensus, the setup favors disciplined accumulation — not panic.