Can Broadcom’s explosive AI growth finally silence Wall Street’s doubts, or is the market still demanding even bigger numbers?

What Do Broadcom AI Earnings Reveal About AI Infrastructure Leadership?

Broadcom Inc. posted Q2 FY2026 semiconductor revenue of $22.19 billion, with AI-related chips accounting for $10.8 billion — over 48% of the total. That figure dwarfs the $4.44 billion reported a year earlier and exceeds the combined AI revenue of Marvell Technology and Credo Technology Group. Free cash flow hit $10.26 billion (46% of revenue), enabling a $10 billion share repurchase program through 2026. Crucially, CEO Hock Tan guided Q3 AI semiconductor revenue to $16.0 billion — a staggering 200% year-over-year increase. This isn’t incremental growth; it’s compounding leverage across custom ASICs, AI networking, and infrastructure software — positioning Broadcom as the indispensable ‘second brain’ behind NVIDIA’s processing power.

How Does the Turnberry Agreement Boost Broadcom’s Margins?

The European Parliament’s ratification of the Turnberry Agreement on June 16, 2026, eliminates U.S. industrial import tariffs into the EU through at least 2029. For Broadcom Inc., which exports high-margin chips and infrastructure software across Europe, this removes a direct cost headwind. With net margins already at 38.8% and return on equity at 33.4%, the tariff removal unlocks immediate margin expansion potential — especially as demand for AI networking gear accelerates across EU cloud providers and telecoms. Unlike commodity chipmakers, Broadcom’s custom silicon contracts are long-dated and pricing-resilient — making tariff relief a pure earnings tailwind, not just a cost offset.

How Does Broadcom Compare to Peers on Growth and Valuation?

Broadcom Inc. posted 47.87% revenue growth — above the industry average of 46.15% — and $13.07 billion in EBITDA, more than double the sector average. Its ROE of 11.11% outpaces peers, and gross profit of $15.41 billion is 2.43x the industry norm. Yet valuation metrics tell a different story: a P/E of 62.68, P/S of 24.35, and P/B of 20.44 all sit above industry averages — prompting caution. RBC Capital Markets analyst Srini Pajjuri maintains a ‘Sector Perform’ rating with a $400 price target, citing Broadcom’s decision not to raise its 2027 AI revenue targets despite Q2’s blowout performance. That restraint contrasts sharply with Tesla and Apple-linked AI infrastructure plays, where guidance revisions have triggered immediate re-ratings.

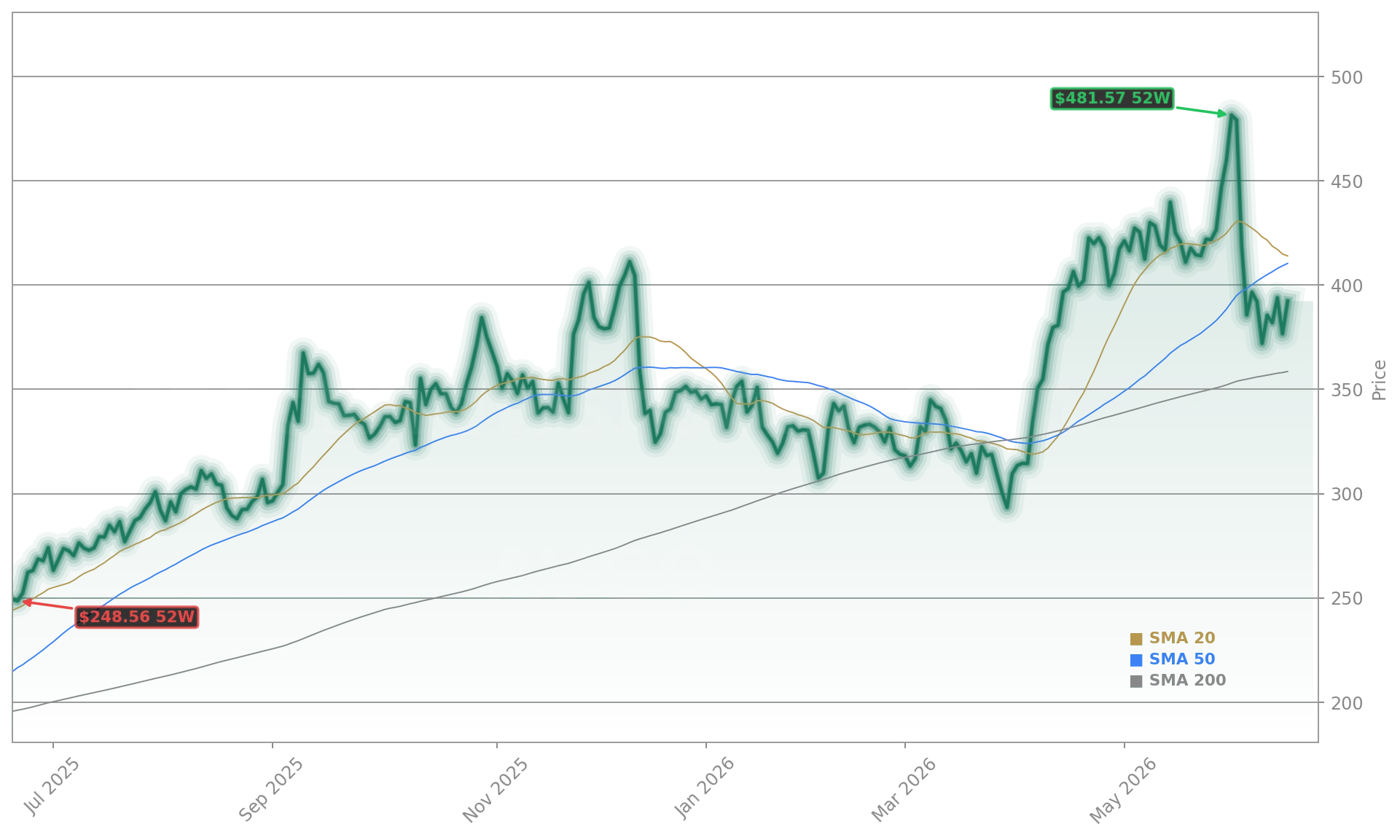

Why Did Wall Street Sell Off Despite Strong Broadcom AI Earnings?

On June 16, 2026, shares of Broadcom Inc. fell 3.01% — part of a broader Nasdaq selloff led by chip stocks including NVIDIA and Micron Technology. TradingKey attributed the move to ‘weaker-than-expected third-quarter artificial intelligence revenue guidance’ — a misreading of Tan’s $16 billion Q3 forecast, which Wall Street interpreted as conservative relative to AI hype. Technical indicators turned neutral-to-oversold, and sentiment on retail forums collapsed into bearish territory. Yet institutional cash flow tells another story: $10.26 billion in free cash flow, $19.6 billion in liquidity, and aggressive buybacks signal confidence. The dip reflects valuation anxiety — not business weakness — as Broadcom AI Earnings continue to outpace consensus and competitor execution.

What’s Next for Broadcom’s AI Infrastructure Dominance?

Broadcom Inc. is co-building an ‘AI XPV platform’ with Apollo Global Management, Blackstone, and others to deploy over 20 GW of AI compute by 2028 for Anthropic and OpenAI — a direct challenge to Microsoft’s and Google’s in-house silicon strategies. With custom AI accelerators now the bulk of its semiconductor business, and infrastructure software (ex-VMware) stabilizing post-integration, Broadcom is transitioning from consolidation play to AI infrastructure orchestrator. Competitors like Qualcomm and AMD remain focused on client and edge AI, while Broadcom owns the data center’s connective tissue. The next catalyst? Confirmation that Q3 hits the $16 billion AI revenue target — a milestone that would cement Broadcom AI Earnings as the most reliable growth vector in the NASDAQ’s AI cohort.

Related coverage includes Broadcom Forecast: $18 After-Hours Shock on AI Guidance, which analyzes the market’s overreaction to forward commentary, and Qualcomm Acquisition +1.8%: Tenstorrent AI Push Builds, highlighting how Broadcom’s dominance is raising the bar for rivals entering the data center AI race. Investors watching the S&P 500’s tech weighting should treat Broadcom not as a chip stock — but as a critical AI infrastructure tollbooth.

We expect semiconductor revenue from AI to grow over 200 percent year-over-year to $16.0 billion in Q3.— Hock Tan, CEO of Broadcom Inc.

Broadcom Inc. remains the most profitable and scalable enabler of AI infrastructure outside of NVIDIA. Its Q2 results affirm leadership in custom silicon and networking — a role increasingly vital as data centers confront power, latency, and interconnect bottlenecks. For U.S. portfolios, Broadcom AI Earnings represent a rare combination of hypergrowth and cash flow discipline. The next quarterly earnings will test whether Wall Street upgrades its view from ‘expensive but essential’ to ‘indispensable at any price’.