Could a Qualcomm Acquisition of Tenstorrent finally turn its long-dismissed AI data center ambitions into a credible threat to Nvidia and AMD?

What Does Tenstorrent Bring to Qualcomm?

Tenstorrent — founded by legendary chip architect Jim Keller (ex-Apple, ex-Tesla Autopilot) — designs RISC-V-based AI accelerators optimized for efficiency, not just raw throughput. Its chips target data-center inference and edge AI workloads where power and thermal constraints matter more than peak FLOPs. A Qualcomm Acquisition would instantly bolster Qualcomm’s Oryon CPU roadmap and its Hexagon NPU architecture, while also reducing reliance on Arm licensing — a structural risk cited by Citigroup in its recent upgrade to ‘Buy’ with a $235 price target. The deal would position Qualcomm alongside NVIDIA and AMD in the $170 billion AI server CPU market projected to explode by 2030, per TradingView analysis.

How Does This Change Qualcomm’s Data Center Outlook?

Qualcomm’s data center ambitions have long been dismissed as aspirational — until now. CEO Cristiano Amon confirmed in April that custom AI chips, built using technology from last year’s Alphawave acquisition, will begin shipping later this year to a major tech client widely believed to be Amazon Web Services. J.P. Morgan now forecasts over $3 billion in data center revenue for fiscal 2027 — a 300% jump from fiscal 2025. That’s not speculative: it’s backed by hardware in production. The Tenstorrent acquisition would add scalability, software stack maturity, and engineering talent to make that forecast credible — and could unlock cross-selling into AWS’s AI agent infrastructure and ByteDance’s AI agent software, per Insider Monkey.

Is the Qualcomm Acquisition a Defensive or Offensive Move?

It’s both. Qualcomm faces a $5 billion annual revenue headwind as Apple phases out its modems by fall — a loss representing ~11% of total revenue. But instead of retreating, Qualcomm is executing a deliberate, multi-pronged offensive: automotive revenue grew 45% year-over-year in Q1 2026; IoT rose 9%; and Snapdragon Reality Elite — its new spatial computing platform — powers over 40 device designs, including AR glasses from XREAL and O’Neill. The Qualcomm Acquisition of Tenstorrent isn’t a Hail Mary — it’s the capstone of a five-year diversification strategy that’s already delivering. Wells Fargo raised its price target to $230, citing ‘catalyst density’ ahead of Investor Day.

What’s at Stake for the S&P 500 and NASDAQ?

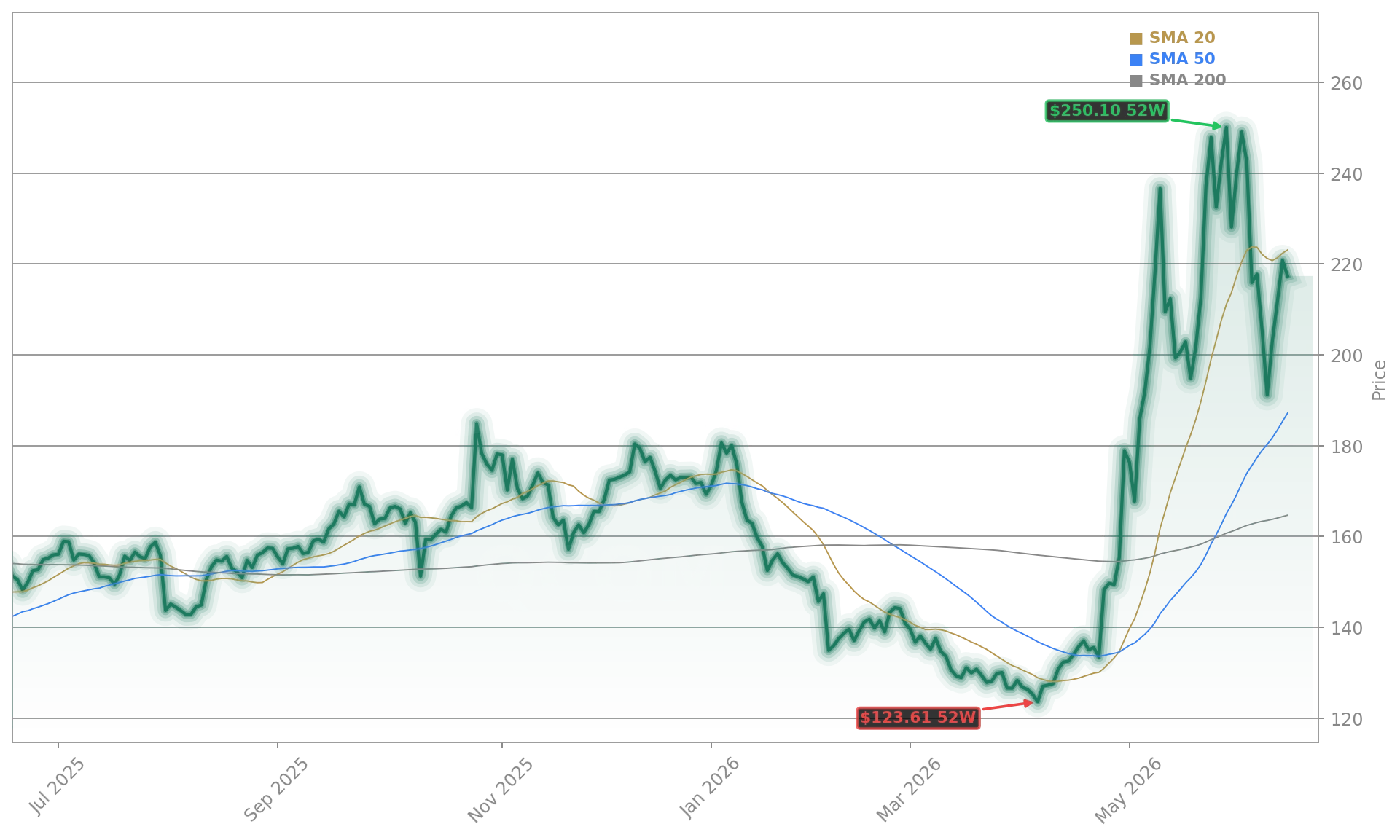

Qualcomm Incorporated remains one of the few semiconductor stocks in the S&P 500 trading below 21x forward earnings — a valuation that looks increasingly anomalous as AI infrastructure spending surges. With the PHLX Semiconductor Index up 150% over two years versus QCOM’s 5% return (including recent gains), the market has yet to price in its AI transition. A successful Qualcomm Acquisition would force index fund managers to reassess weightings, especially as Qualcomm’s exposure to AI infrastructure now rivals that of many ‘pure-play’ AI chip stocks. For NASDAQ investors, QCOM offers AI exposure with lower volatility — and a dividend yield of 1.8%, a rarity among AI enablers.

Qualcomm Acquisition: What Comes Next?

Unlike other speculative AI chip plays, investors aren’t placing a crazy bet that Qualcomm will succeed — they’re finally pricing in what it’s already built.— Asa Fitch and Dan Gallagher, The Wall Street Journal

The June 24 Investor Day will be the critical test. Qualcomm is expected to detail its data center roadmap, reveal its first major customer for custom AI chips, and clarify timelines for Tenstorrent integration. Analysts from RBC Capital Markets and Morgan Stanley are forecasting a 2027 inflection point — with data center and automotive together contributing over 25% of total revenue, up from just 12% in 2024. The Qualcomm Acquisition isn’t just about $10 billion — it’s about reshaping Qualcomm’s identity from smartphone chipmaker to AI infrastructure partner. For U.S. portfolios, that’s a structural upgrade — not a tactical trade.