Can Broadcom’s AI boom still justify its premium valuation after a sharp sell-off and a surprisingly strong after-hours rebound?

Why Did Broadcom Fall After Strong Earnings?

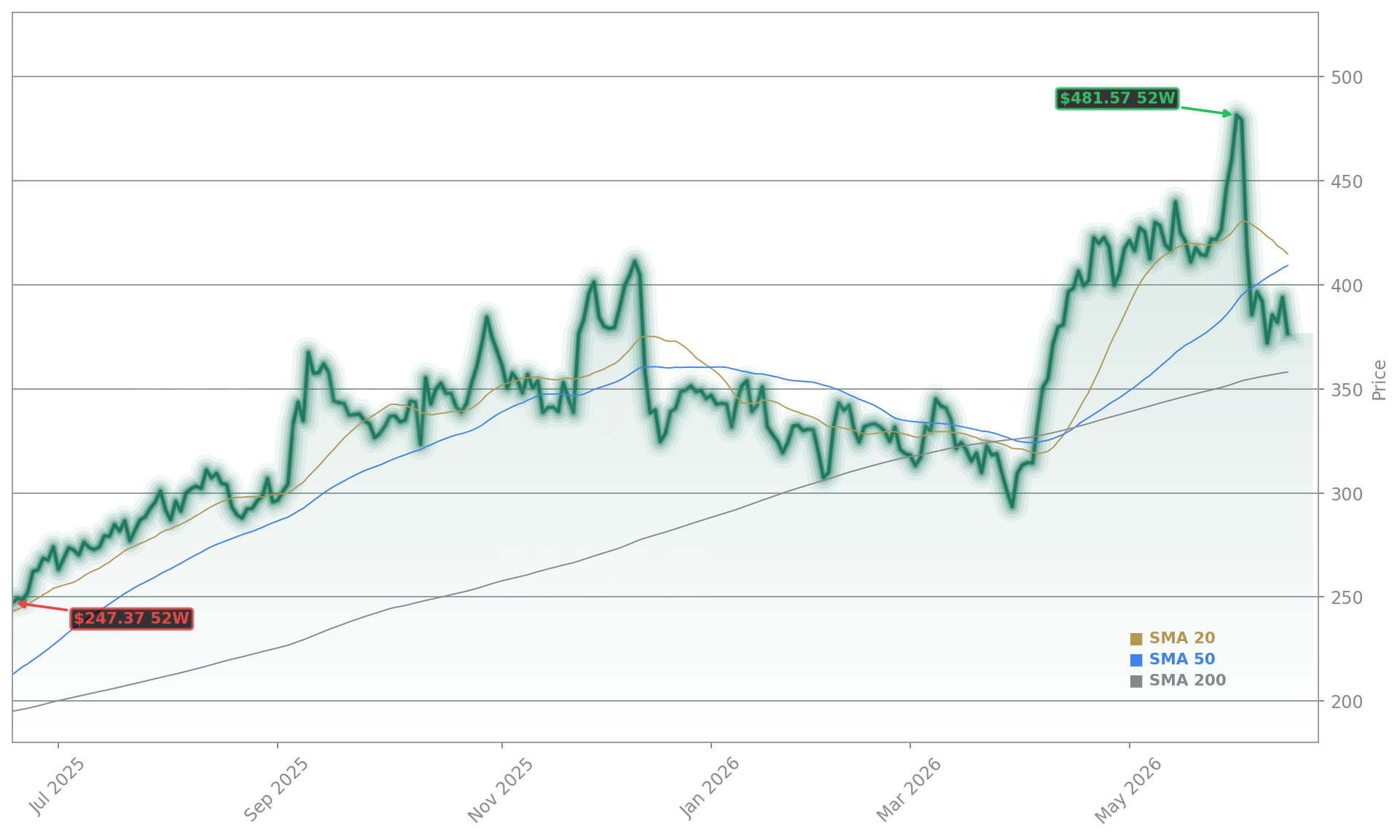

Broadcom Inc. closed Tuesday at $376.71 — 4.37% lower than its prior close — despite reporting fiscal Q2 2026 results that would have thrilled most S&P 500 peers. Revenue surged 48% year over year to $22.2 billion, adjusted EPS jumped 54% to $2.44, and free cash flow soared 60% to $10.3 billion. The standout was AI semiconductor revenue: $10.8 billion, up 143% YoY. Yet the stock underperformed peers including NVIDIA, Tesla, and Apple, falling more than 23% below its $495.00 52-week high set just days after its June 3 earnings release. The disconnect underscores how Wall Street now prices AI exposure not on absolute growth, but on sequential acceleration — and Broadcom’s guidance for Q3 AI revenue — while still massive at $16 billion — missed consensus by a narrow but critical margin.

What Does the Broadcom Forecast Say About AI Chip Competition?

The Broadcom Forecast for Q3 2026 projects AI semiconductor revenue will grow more than 200% year over year — a staggering figure that, paradoxically, triggered concern. Analysts at RBC Capital Markets noted the guidance implies ‘moderating sequential momentum’ versus prior quarters, especially as rival chipmakers like AMD and Credo Technology (CRDO) post sharper YTD gains. Broadcom’s custom AI chips serve hyperscalers like Alphabet and Meta — offering cost-efficient inference and networking solutions — but lack the general-purpose versatility of NVIDIA’s GPUs. That niche strength is becoming both a competitive moat and a growth constraint. Citigroup recently reiterated its ‘Neutral’ rating, citing ‘customer concentration risk’ — five end customers represent ~40% of revenue — and a forward P/E of 33, well above the IT sector average of 22.3.

Is the Dip a Buying Opportunity?

Yes — but with conditions. Broadcom’s PEG ratio stands at 0.72, suggesting the stock is undervalued relative to its projected five-year growth, per Bloomberg consensus. Its $1.8 trillion market cap remains the sixth-largest on the NASDAQ, and its dividend yield (1.1%) is modest but stable. More telling: insider activity resumed last week. Chairman Harry You purchased 1,000 shares at $373.57 — a symbolic but meaningful signal following the $10 billion buyback authorization announced in April 2025. That move helped double shares from post-tariff lows. While Morgan Stanley maintains an ‘Overweight’ rating, it warns that ‘execution on custom AI ramp must accelerate to sustain premium valuation.’ The after-hours rebound to $394.81 suggests institutional buyers are stepping in — especially as semiconductor stocks broadly corrected amid sector rotation into industrials and financials.

How Does Broadcom Compare to the Broader Tech Landscape?

Broadcom’s willingness to step in when it thinks sellers are wrong is why we’ve been keeping a close watch on it.— Ben Gran, The Motley Fool

In a market where mega-cap tech drove the 2025–2026 rally, Broadcom’s 11% YTD gain trails Credo (+74%), AMD (+32%), and even Micron (+18%). Yet its cash flow generation — $10.3 billion in Q2 alone — dwarfs most peers. Its enterprise infrastructure business (networking, storage, security) remains highly profitable and stable, insulating it from AI volatility. That duality — high-growth AI segment paired with mature, cash-rich legacy operations — makes Broadcom uniquely positioned to weather sentiment shifts. Still, its valuation premium remains a headwind: at 66x trailing P/E, it’s cheaper than its $500 peak, but still expensive versus the S&P 500’s 22x multiple. Analysts at Goldman Sachs see ‘room for rerating’ only if Q3 execution exceeds guidance — a key catalyst investors will watch closely.