Are Marvell Insider Sales just routine profit-taking, or a quiet warning as the stock whipsaws around its AI-fueled surge?

Why Are Marvell Insider Sales Accelerating?

Marvell Insider Sales have intensified across the C-suite in Q2 2026 — with Chairman Matthew J. Murphy, President Chris Koopmans, CFO Willem A. Meintjes, and VP Mark Casper collectively offloading over 140,000 shares since April. Murphy alone sold 7,500 shares on June 15 at $298.76, the highest price point yet in this wave — and all transactions were executed under pre-arranged Rule 10b5-1 plans, indicating planned, not reactive, exits. Notably, Koopmans sold 10,000 shares on June 1 — the same day Marvell confirmed strong AI networking bookings — suggesting timing reflects routine portfolio management rather than bearish sentiment. Still, volume and concentration raise flags for S&P 500 index watchers, given Marvell Technology, Inc. is widely expected to join the benchmark this quarter.

How Does This Compare to Peers Like NVIDIA and Intel?

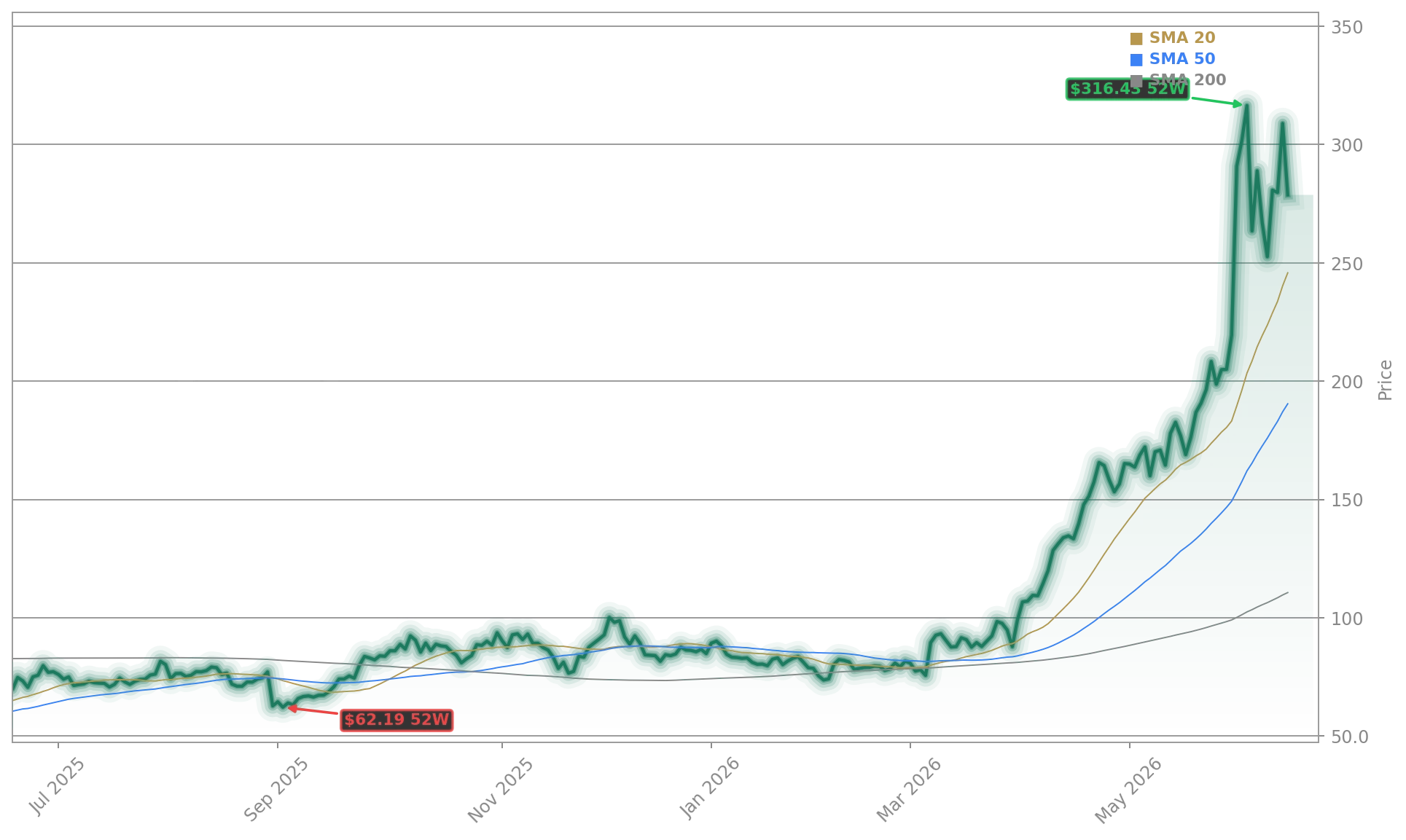

While NVIDIA shares surged 32% year-to-date amid AI infrastructure demand, its insider selling remains modest — just $8.4 million in reported sales over the past 90 days. Meanwhile, Intel (INTC) executives sold $21.7 million in Q2, but at sharply depressed valuations — underscoring Marvell Insider Sales’ uniqueness: they’re occurring near all-time highs. Marvell Technology, Inc. has climbed nearly 250% since early 2025, outpacing the NASDAQ Composite by 41% over five years. That outperformance — and Jensen Huang’s public nod calling Marvell Technology, Inc. a ‘next trillion-dollar company’ — makes recent insider activity especially noteworthy for U.S. portfolio managers benchmarked to the S&P 500.

What’s Driving the Stock’s Volatility?

Marvell Technology, Inc. plunged 9.78% during regular trading on June 16 but rebounded sharply to $305.32 in after-hours action — a 9.56% gain — after the company reaffirmed its AI-driven revenue outlook. Analysts at Citigroup recently raised Marvell’s price target to $335, citing ‘accelerating 800G optical interconnect wins with cloud hyperscalers’. RBC Capital Markets maintains an ‘Outperform’ rating, noting Marvell’s ‘structural advantage in AI networking over legacy players like Intel and Broadcom’. Yet the stock’s 52-week high remains $312.45 — just 2.3% above Monday’s after-hours print — meaning renewed insider selling could test resistance. With Marvell Insider Sales now totaling $15.3 million in Q2, momentum investors are weighing whether this reflects profit-taking or a subtle signal ahead of Q2 earnings.

Is Marvell Technology, Inc. Still a Buy for Long-Term Portfolios?

Yes — but with nuance. Marvell Technology, Inc. trades at 38x forward earnings, a premium to the S&P 500’s 21x, yet justified by its 47% projected AI-related revenue growth in FY2027. The company’s $255.63 billion market cap and $5.38 billion in cash position it as a core holding for tech-focused growth portfolios. Still, Morgan Stanley analysts warn that ‘insider liquidity events near highs warrant tactical trimming’, especially for investors holding over 1% of portfolio weight. The upcoming S&P 500 inclusion — widely expected in July — could add $2.1 billion in passive inflows, offsetting near-term selling pressure. For U.S. investors, Marvell Insider Sales are a data point, not a catalyst — but one that demands active monitoring.

We’re seeing exceptional AI-related bookings — especially in 800G optical and AI accelerator interconnects — and our long-term revenue model is now anchored to 25%+ CAGR through 2028.— Matthew J. Murphy, Chairman, Marvell Technology, Inc.

Related coverage: Marvell’s AI revenue outlook remains robust despite the recent pullback — Marvell Forecast After -8.9% Drop as AI Revenue Outlook Soars. Meanwhile, broader tech sentiment is being tested by enterprise software volatility — Salesforce Acquisition $3.6B Deal Meets CRM Stock Slide.