Will Marvell S&P 500 Inclusion extend the AI trade, or is the stock already priced for perfection?

What Does Marvell S&P 500 Inclusion Mean for Index Funds?

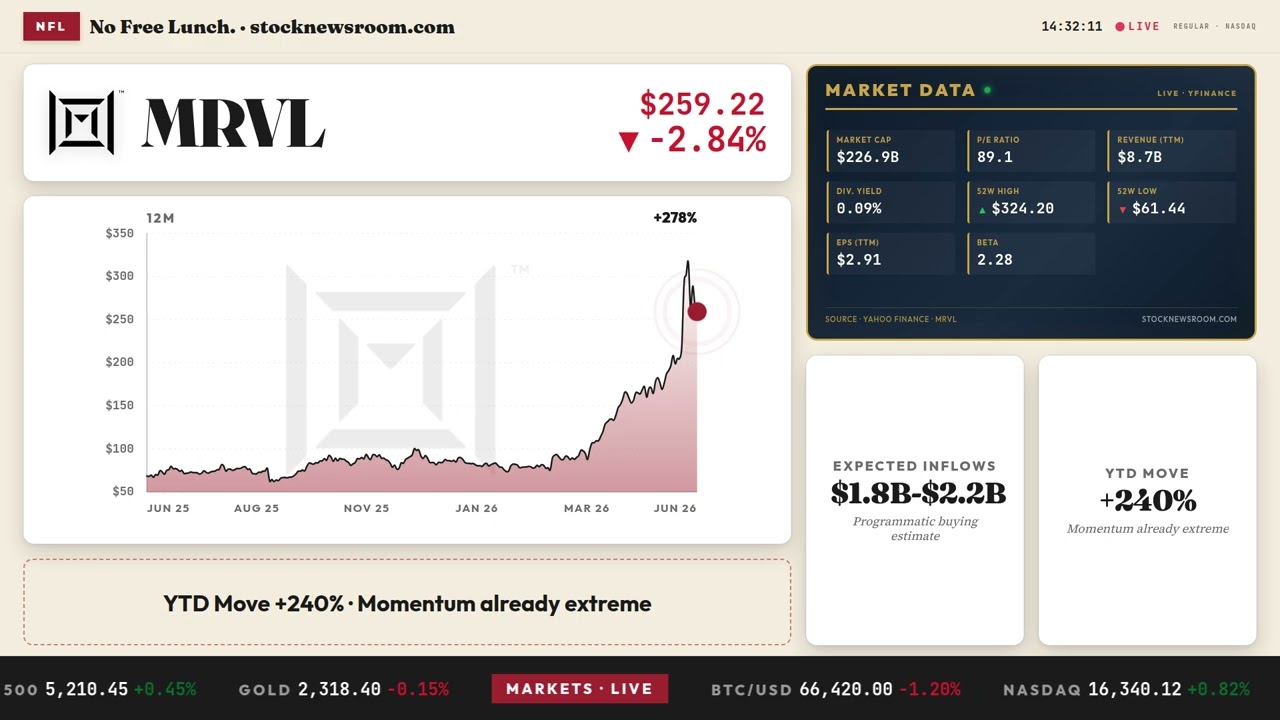

Marvell Technology, Inc. joins the S&P 500 on June 22—replacing PoolCorp (POOL) in the quarterly rebalancing. This triggers mandatory buying from over $6.5 trillion in assets tracking the index, including the SPDR S&P 500 ETF Trust (SPY). According to Barchart.com, the move is expected to generate $1.8–$2.2 billion in programmatic inflows over the next 10 trading days. Unlike typical additions, Marvell’s inclusion comes with unusually high momentum: the stock is up 240% year-to-date and trades at a forward P/E of 66—reflecting Wall Street’s premium on AI infrastructure exposure. Deutsche Bank recently raised its price target to $295, citing ‘exceptional AI-related bookings’ and sustained design wins with Microsoft and Amazon.

Why Is Marvell’s Role in AI Infrastructure Non-Replaceable?

While NVIDIA dominates compute, Marvell Technology, Inc. owns the data pipes. Its Teralynx T100 switch chip—shipping in Q2—solves latency bottlenecks in AI clusters with hundreds of thousands of accelerators per rack. As Jensen Huang declared publicly, Marvell’s silicon is ‘essential for data centers’—a rare endorsement that elevated MRVL to the ‘next trillion-dollar company’ narrative. That’s not hyperbole: cloud giants are committing over $400 billion annually to AI infrastructure, and every new server rack allocates 12–15% of its silicon budget to networking, optical DSPs, and custom ASICs—the exact domains where Marvell Technology, Inc. holds leadership. RBC Capital Markets upgraded MRVL to ‘Outperform’, noting ‘structural pricing power emerging in optical interconnects.’

How Is the Market Pricing Marvell’s Execution Risk?

Marvell Technology, Inc. trades 140% above its 200-day moving average—a sign of extreme conviction and vulnerability. Though Q1 revenue hit $2.4 billion (+28% YoY) and guidance calls for 35% growth in Q2, the stock’s volatility (124% annualized) reveals investor anxiety: Can it scale without margin compression? Can it defend against rivals like Broadcom and Cisco in AI networking? Citigroup sees upside to $310 but warns that ‘any delay in Teralynx ramp or softness in hyperscaler capex could trigger a 20% correction.’ That said, bullish options activity surged on June 10—16 call contracts struck at $310 expiring July 17—suggesting sophisticated players are betting on post-inclusion momentum.

Where Does Marvell Stand Versus Key Semiconductor Peers?

Marvell is no longer a peripheral chip supplier. Rather, the company is swiftly becoming a core enabler of the AI economy.— Jensen Huang, CEO of NVIDIA

Among AI infrastructure enablers, Marvell Technology, Inc. occupies a unique niche. Unlike Micron Technology (MU), which supplies memory, or Advanced Micro Devices (AMD), which competes on compute, Marvell’s entire portfolio is purpose-built for data movement—Ethernet controllers, optical DSPs, and custom XPUs. It outperformed peers in 2026: MRVL is up 240%, versus Micron (+192%) and AMD (+137%). Yet valuation remains stretched: MRVL trades at 11x forward sales, versus 6x for Broadcom and 4x for Intel. Still, Goldman Sachs argues that ‘Marvell’s AI interconnect TAM is growing at 42% CAGR—justifying a premium multiple if execution holds.’