Can Marvell’s AI-fueled growth story survive an after-hours sell-off even as management lifts its long-term revenue outlook?

What’s Driving the Marvell Forecast?

Marvell Technology, Inc. isn’t riding the AI wave — it’s building the infrastructure that keeps it flowing. Its custom XPU silicon, 1.6T optical interconnects, and 51.2T Ethernet switches are now embedded in hyperscaler GPU clusters at NVIDIA, Meta, and Microsoft. Unlike broader semiconductor peers, Marvell’s revenue is increasingly decoupled from consumer cycles and anchored to multi-year AI capex commitments. CEO Matt Murphy confirmed the shift during the May 27 earnings call: ‘We are seeing exceptional AI-related bookings, and as a result, we are significantly raising Marvell’s revenue outlook for both fiscal 2027 and fiscal 2028.’ That’s not incremental — it’s a structural re-rating.

How Does Marvell Compare to Peers?

While NVIDIA dominates AI compute and Tesla pushes edge inference, Marvell owns the critical ‘plumbing’ — the high-speed interconnect layer that determines whether GPU clusters scale or stall. That distinction matters. Micron Technology (MU) just lifted its AI memory forecast +7.4% on surging HBM demand, but Marvell’s interconnect solutions sit upstream — enabling the very bandwidth those memory stacks require. Meanwhile, Broadcom (AVGO) and Intel (INTC) are diversifying, but Marvell remains the cleanest pure-play on AI data center interconnect for retail and institutional investors alike. Citigroup recently raised its price target on Marvell to $265, citing ‘unmatched execution in custom silicon ramp’ and ‘multi-year visibility on 1.6T deployments.’

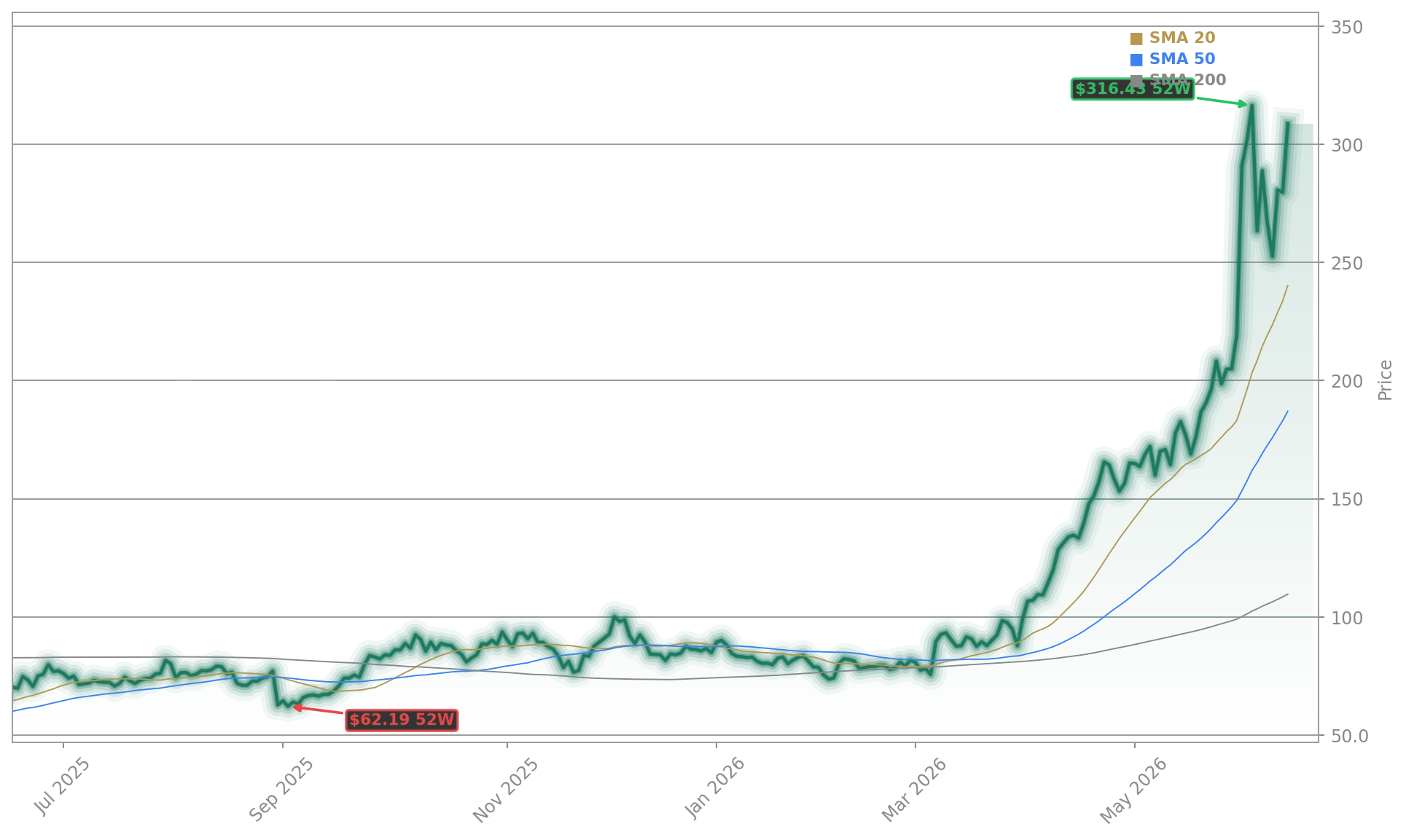

Is the Valuation Justified?

At $308.70 in after-hours trading — up sharply from $279.70 at Friday’s close — Marvell trades at a forward P/E near 70, well above the S&P 500 tech sector median of 28. But context is critical: this isn’t speculative froth. The Marvell Forecast reflects real, contracted demand — not guidance based on models. RBC Capital Markets upgraded Marvell to ‘Outperform’, noting ‘a 3–5-year runway of >25% CAGR in AI infrastructure revenue, with margins expanding as 5nm+ custom ASICs scale.’ Still, volatility remains baked in: the stock’s 230% YTD gain has compressed near-term risk-adjusted returns. Traders who chased the $1 trillion valuation call from NVIDIA CEO Jensen Huang may face consolidation — but long-term holders are betting on interconnect becoming as indispensable as GPUs themselves.

What’s Next for Wall Street?

With Q2 guidance pointing to $2.7 billion — and management explicitly stating growth will accelerate each quarter throughout fiscal 2027 — the Marvell Forecast signals a broader inflection for AI infrastructure stocks. The NASDAQ is up 14% YTD, and Marvell’s outperformance (230%) reflects its positioning at the center of the most capital-intensive part of the AI stack. Goldman Sachs sees Marvell as ‘the single most leveraged name to AI cluster scalability,’ with upside potential tied directly to hyperscaler CapEx acceleration in H2 2026 and beyond. Analyst consensus now stands at 8 Strong Buy, 31 Buy, and 5 Hold ratings — the most bullish coverage mix among pure-play chip stocks. Still, investors should watch inventory levels and 1.6T optics yield rates closely: any delay in optical transceiver ramp could pressure near-term margins.

We are seeing exceptional AI-related bookings, and as a result, we are significantly raising Marvell’s revenue outlook for both fiscal 2027 and fiscal 2028.— Matt Murphy, CEO of Marvell Technology, Inc.

Related Coverage: Marvell’s recent inclusion in the S&P 500 — despite a -2.3% dip on the index announcement day — may unlock fresh institutional demand as passive funds begin rebalancing; for deeper analysis, see Marvell S&P 500 Inclusion -2.3% as AI Momentum Builds. Meanwhile, Micron Technology Forecast +7.4% as AI Memory Demand Surges shows how memory and interconnect demand are converging — a dynamic that could amplify Marvell’s revenue tailwinds as HBM bandwidth requirements push optical interconnect adoption higher.