Can Taiwan Semiconductor AI Growth keep accelerating as AI demand and U.S. expansion redraw the global chip map?

How Is Taiwan Semiconductor AI Growth Reshaping U.S. Chip Strategy?

Taiwan Semiconductor Manufacturing Co. isn’t just riding the AI wave — it’s building the infrastructure that powers it. In Q1 2026, wafer revenue surged to NT$968 billion from NT$714 billion a year earlier, fueled almost entirely by AI accelerator demand. The company’s forward P/E of 28 sits comfortably against projected 28% compound annual EPS growth — yielding a PEG ratio of just 1.4, a compelling valuation for a company delivering 58.1% operating margins and 36.2% return on equity. With $35.9 billion in quarterly revenue and $18.2 billion in net income, Taiwan Semiconductor Manufacturing Co. outperformed SpaceX — now valued at over $2.5 trillion despite reporting a $4.94 billion net loss in 2025 — underscoring the market’s growing preference for cash-flow clarity over speculative scale.

Why Are Hedge Funds Racing to Add TSMC?

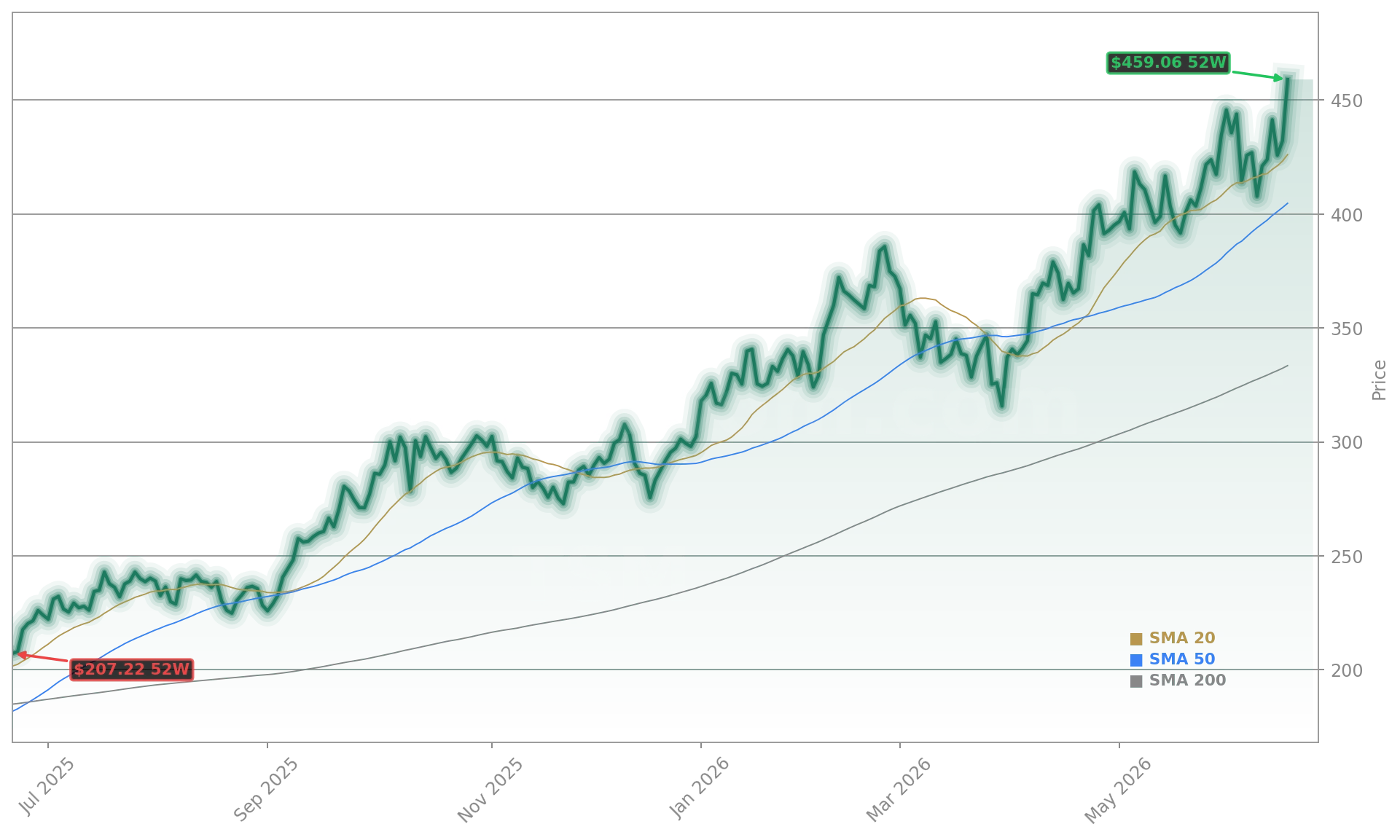

At the end of Q1 2026, 234 hedge fund portfolios held Taiwan Semiconductor Manufacturing Co., up from 224 in Q4 2025 — cementing its position as the sixth-most-held stock among elite U.S. managers. Giverny Capital Asset Management highlighted the company as a top contributor to its Q1 performance, noting that TSMC held up strongly even as major customers like NVIDIA and Apple faced valuation pressure. ‘TSMC has long traded at a PE multiple discount to its customers, but the gap is narrowing,’ the firm stated — a signal that Wall Street is finally pricing in its strategic centrality. With a $2.24 trillion market cap and 104.21% one-year share gain, the stock now trades just below the $467.84 consensus price target set by 17 of 19 analysts — including Citigroup, which recently raised its target to $472, citing ‘unmatched capacity execution in 3nm and 2nm nodes.’

What’s Driving the U.S. Expansion Push?

Taiwan Semiconductor Manufacturing Co. is executing the most ambitious U.S. manufacturing buildout in semiconductor history — anchored by its $40 billion Arizona fab complex. The 2026 U.S. CHIPS Act tax credit increase — from 25% to 35% of qualified investments — has accelerated timelines and de-risked capital allocation. That move, paired with parallel investments in Japan (ESMC) and Japan Advanced Semiconductor Manufacturing (JASM), positions TSMC to supply 90% of the world’s leading-edge chips across three geopolitical zones. Crucially, the Arizona facility isn’t just symbolic: it’s already producing chips for NVIDIA under a co-investment agreement announced earlier this year — directly supporting the Phoenix-based AI infrastructure buildout. This isn’t diversification for optics; it’s capacity diversification for resilience.

How Does TSMC Compare to Rivals Amid AI Demand?

While Intel Foundry seeks validation through its partnership with Apple, Taiwan Semiconductor Manufacturing Co. continues to widen its technology lead — shipping 3nm chips at scale while rivals remain in pilot phases. AMD and Broadcom rely on TSMC for their latest AI chips, and even as Broadcom’s forecast drew a bullish upgrade from JPMorgan, TSMC’s role as the sole high-yield manufacturer remains irreplaceable. RBC Capital Markets recently reiterated its ‘Outperform’ rating on TSMC, stating, ‘No other foundry combines this scale, yield, and node leadership — especially in AI-optimized packaging like CoWoS.’ That structural advantage explains why top-10 customers represent 84% of accounts receivable: they have no viable alternative. The risk isn’t competition — it’s execution at scale, which TSMC has delivered for three consecutive quarters.

What’s Next for Taiwan Semiconductor AI Growth?

TSMC has long traded at a PE multiple discount to its customers, but the gap is narrowing.— Giverny Capital Asset Management

With Q2 2026 already underway and AI capex commitments from cloud providers surging past $200 billion this year, Taiwan Semiconductor AI Growth shows no signs of plateauing. The company’s 60% projected AI revenue CAGR through 2029 — from 2024 baseline — remains intact, and its dividend policy continues to mature, with a NT$6.00 per share payout confirmed for October 8, 2026. As geopolitical tailwinds align with AI infrastructure demand, Taiwan Semiconductor Manufacturing Co. is no longer just a supplier — it’s the linchpin of America’s AI sovereignty strategy.