Can Taiwan Semiconductor keep climbing as AI demand and analyst upgrades collide ahead of its July 16 Analyst Day?

What’s Driving the Taiwan Semiconductor Forecast Upside?

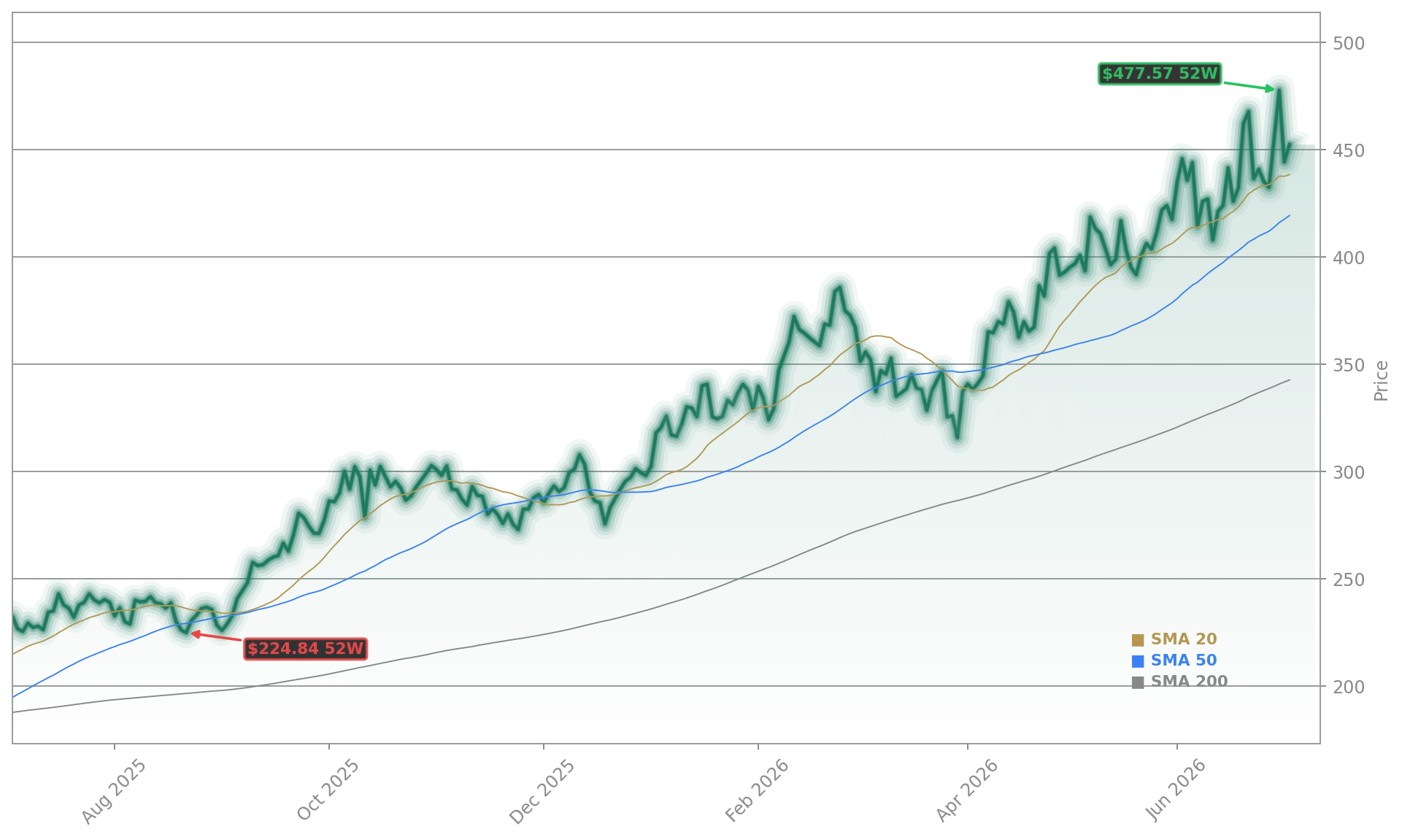

Taiwan Semiconductor Manufacturing Co. is riding a powerful confluence of structural tailwinds: surging AI infrastructure spending, sold-out advanced-node capacity, and aggressive capital expansion. The company reported Q1 2026 revenue of $35.6 billion — a 35% year-over-year jump — backed by triple-digit monthly growth in January (+37%), February (+22%), and March (+45%). With $56 billion in planned 2026 capital expenditures rising to $74 billion in 2027, the company is scaling capacity at an unprecedented pace. Crucially, management confirmed capacity is effectively sold out through year-end, underscoring pricing power and demand durability. This momentum directly supports the bullish Taiwan Semiconductor Forecast now emerging across major investment banks.

How Are Analysts Updating Their Taiwan Semiconductor Forecast?

Citigroup has reiterated its Buy rating and expects Taiwan Semiconductor Manufacturing Co. to raise long-term revenue targets and 2026 growth guidance at the July 16 Analyst Day. Barclays followed suit, with analyst Simon Coles noting that ‘the market is clamoring for advanced logic wafer supply’ — a dynamic that directly benefits Taiwan Semiconductor Manufacturing Co. as the dominant foundry partner for NVIDIA, Apple, and AMD. Barclays upgraded its rating and lifted the price target to $625 from $470 — the highest on record — citing expanding margins, leadership in 3nm and 2nm processes, and exposure to AI compute expansion. Bernstein also upgraded the stock, highlighting the company’s early adoption of high-NA EUV lithography by 2030 and its strategic role in DRAM and advanced logic capacity buildouts.

What Do Institutional Flows Say About the Taiwan Semiconductor Forecast?

Institutional buying activity confirms broad confidence in the Taiwan Semiconductor Forecast. Kathmere Capital Management LLC increased its stake by 30.1% in Q1, while Collaborative Fund Advisors LLC and Ascentis Independent Advisors initiated or expanded positions. DGS Capital Management LLC boosted holdings by 8.6%, and FUKOKU MUTUAL LIFE INSURANCE Co. raised its stake by over 2,500%. Even amid some selective selling — such as Hodges Capital Management reducing its position by 18.7% — TSM remains its 28th largest holding, reflecting continued strategic relevance. Collectively, institutional ownership now stands at 16.51%, and insider activity has been net positive, with VPs Lipen Yuan and Bor-Zen Tien adding shares. The company’s recent dividend increase to $1.1136 per quarter — supported by $3.11 earnings per share and $30.65 billion in quarterly revenue — further validates cash flow strength.

How Does Options Activity Reflect the Taiwan Semiconductor Forecast?

Options markets are pricing in continued upside — and intelligent entry points. The $450 put contract carries a 61% probability of expiring worthless, offering investors a potential 14.58% yield boost (23.33% annualized) if sold-to-open. Meanwhile, the $480 covered call presents a 19.43% total return if assigned, with a 45% chance of expiring worthless and delivering a 15.00% yield boost. Implied volatility sits at 53–54%, notably above the 39% trailing 250-day realized volatility — suggesting options traders are pricing in elevated near-term catalysts, including the July 16 Analyst Day and upcoming earnings. This options positioning reinforces the growing consensus around the Taiwan Semiconductor Forecast — not just for growth, but for disciplined execution amid geopolitical and supply chain complexity.

Related Coverage: For deeper analysis of today’s price action and near-term catalysts, see Taiwan Semiconductor Forecast: +4.4% Surge Before July 16. The article explores whether current momentum is sustainable or if valuation and legal risks could cap further gains ahead of Analyst Day.

Taiwan Semiconductor Manufacturing Co. remains the indispensable manufacturing backbone of the global AI revolution — producing over 90% of the world’s most advanced semiconductors. The Taiwan Semiconductor Forecast is now decisively tilted toward higher growth, margin expansion, and sustained capital leadership. For U.S. investors, this isn’t just a chip stock play — it’s core infrastructure exposure to AI compute, with direct leverage to NVIDIA, Tesla, and Apple’s next-generation hardware roadmaps. The July 16 Analyst Day will be the definitive test of whether Wall Street’s elevated expectations are justified — and whether the current Taiwan Semiconductor Forecast becomes reality.