Can Taiwan Semiconductor keep climbing as AI demand explodes, or is too much optimism already priced in before Analyst Day?

What’s Driving the Taiwan Semiconductor Forecast?

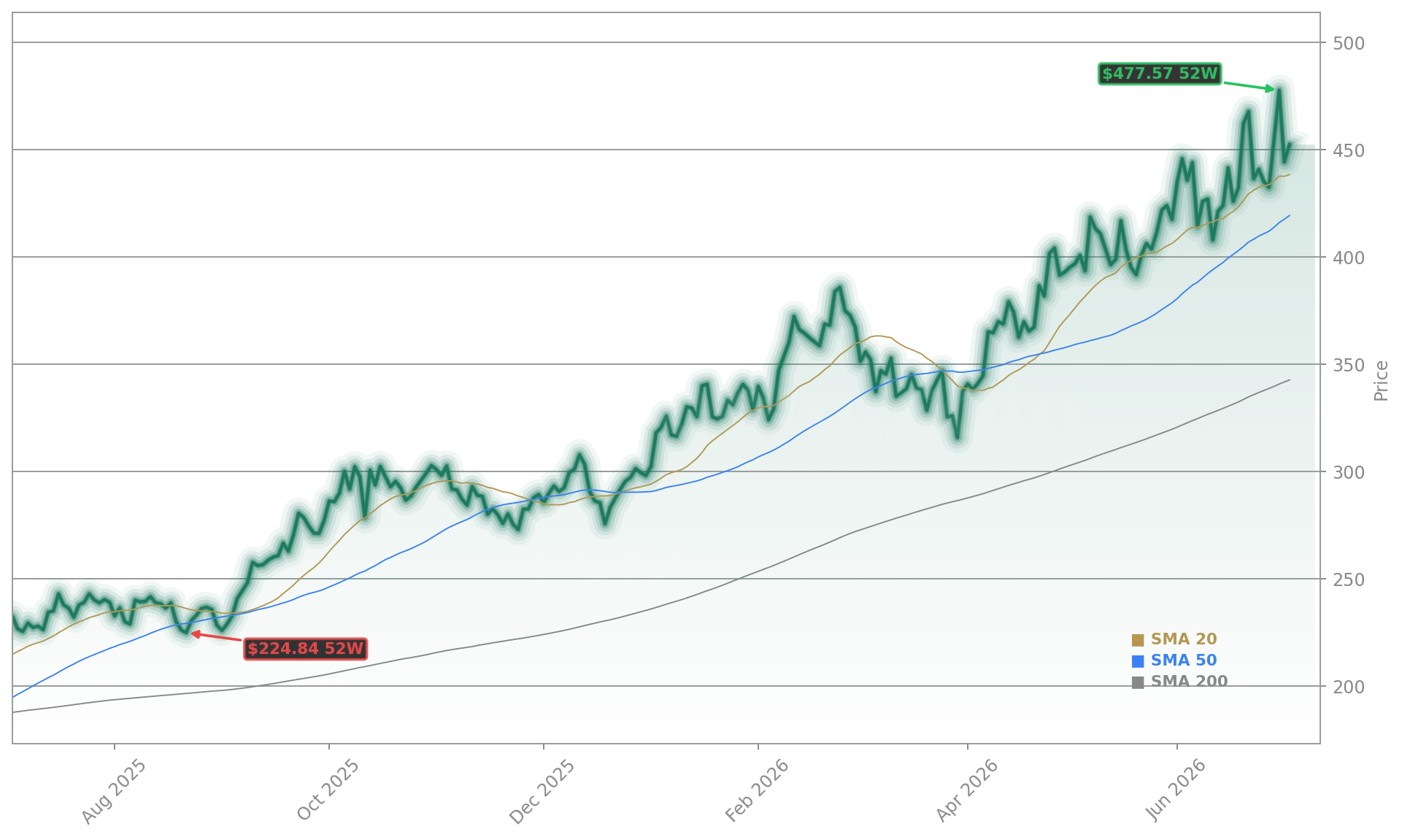

Taiwan Semiconductor Manufacturing Co. is surging amid accelerating AI infrastructure buildouts, with Q1 2026 revenue hitting $35.6 billion—up 35% year-over-year and well above consensus. Monthly revenue growth spiked to 45% year-over-year in March, underscoring relentless demand for 3nm and 2nm chips powering NVIDIA’s Blackwell and next-gen inference accelerators. Citigroup has issued a Buy rating ahead of the July 16 Analyst Day, projecting that management will raise both full-year 2026 revenue targets and long-term growth assumptions. The firm expects the Taiwan Semiconductor Forecast for 2026 to reflect upgraded capacity utilization, pricing power, and expanded exposure to high-margin AI logic and DRAM foundry services.

How Does Barclays Justify Its $625 Price Target?

Barclays reiterated its Overweight rating and hiked its price target to $625 from $470—implying 38% upside from current levels. Analyst Simon Coles emphasized that Taiwan Semiconductor Manufacturing Co. remains the irreplaceable manufacturing backbone of the global AI stack, fabricating over 90% of the world’s most advanced semiconductors. With capital expenditures set to jump from $56 billion in 2026 to $74 billion in 2027, the firm sees accelerating returns on R&D and scale advantages versus rivals like Samsung Foundry—especially as Meta shifts some MTIA chip production to Samsung due to near-term capacity constraints. That move, however, underscores Taiwan Semiconductor Manufacturing Co.’s strategic leverage: its lead in high-NA EUV lithography and yield stability remains unmatched, per Bernstein’s recent upgrade.

Is the Semiconductor Rally Sustainable?

The Philadelphia Semiconductor Index rose 2% today alongside Taiwan Semiconductor Manufacturing Co.’s 4.44% gain—reinforcing sector-wide conviction in AI-driven capex cycles. RiverPark Large Growth Fund cited Taiwan Semiconductor Manufacturing Co. as its second-largest Q1 2026 contributor, noting its January–March revenue growth outpaced even Apple and Tesla-linked suppliers. Still, valuation remains a watchpoint: the stock trades at a 2026 P/E of 28x, above the S&P 500’s 21x and the NASDAQ-100’s 25x. Yet with geopolitical risk partially mitigated by the January U.S.–Taiwan trade agreement and S&P Global maintaining its AA- credit rating, the risk-reward profile tilts bullish for institutional investors. Options data further supports upside conviction: the $480 call (Feb 2027 expiry) carries a 45% probability of expiring worthless—meaning a 19.4% total return if assigned, or 15% extra yield if it lapses.

What Does the Options Market Say About Taiwan Semiconductor Forecast?

Options activity reveals strong institutional interest in both hedging and yield generation. The $450 put (bid $65.60) offers a $384.40 effective cost basis—nearly 15% below current price—with a 61% probability of expiring worthless, implying a 14.6% return on cash committed (23.3% annualized). Implied volatility sits at 53%—well above the 39% trailing 12-month realized volatility—suggesting options traders anticipate elevated near-term catalysts, likely tied to the Analyst Day and upcoming Q2 earnings. That volatility premium, combined with tightening supply and expanding AI workloads across cloud and edge, makes the Taiwan Semiconductor Forecast one of the most actionable growth narratives on Wall Street today.

How Does TSMC Compare to U.S. Tech Giants?

Unlike vertically integrated players, Taiwan Semiconductor Manufacturing Co. benefits from exposure to multiple AI leaders: it manufactures chips for NVIDIA, Apple, AMD, and Qualcomm—without competing with them. That neutrality, combined with $2 trillion market cap scale and dominant 58% foundry market share, gives it pricing power rare among hardware suppliers. While semiconductor peers like Intel face execution risk, and ASML remains a critical enabler, Taiwan Semiconductor Manufacturing Co. sits at the center of the AI value chain—making its Taiwan Semiconductor Forecast a key barometer for the entire NASDAQ and S&P 500 tech cohort. Its Q1 performance outpaced the Russell 1000 Growth Index’s 9.78% Q1 decline—highlighting its defensive growth profile in volatile macro conditions.

Related coverage: For deeper analysis on recent forecast revisions, see TSMC Forecast -6.3%: Why Target Hikes Failed to Lift Shares. On broader AI-related sector dynamics, read Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears.

Taiwan Semiconductor Manufacturing Co. is the vital manufacturing backbone of the global AI industry.— Barclays analyst Simon Coles

Taiwan Semiconductor Manufacturing Co. remains the linchpin of global AI hardware execution. Its upcoming Analyst Day will set the tone for semiconductor capex and AI infrastructure spending through 2027—and the Taiwan Semiconductor Forecast is now the most closely watched guidance metric on Wall Street. For investors seeking exposure to AI’s physical layer, the stock offers scale, leadership, and structural tailwinds. The next quarterly earnings report will confirm whether the momentum holds.