Has Wall Street misread Adobe’s AI risk so badly that this Adobe Upgrade could mark the start of a major rerating?

Why Did HSBC Issue This Adobe Upgrade?

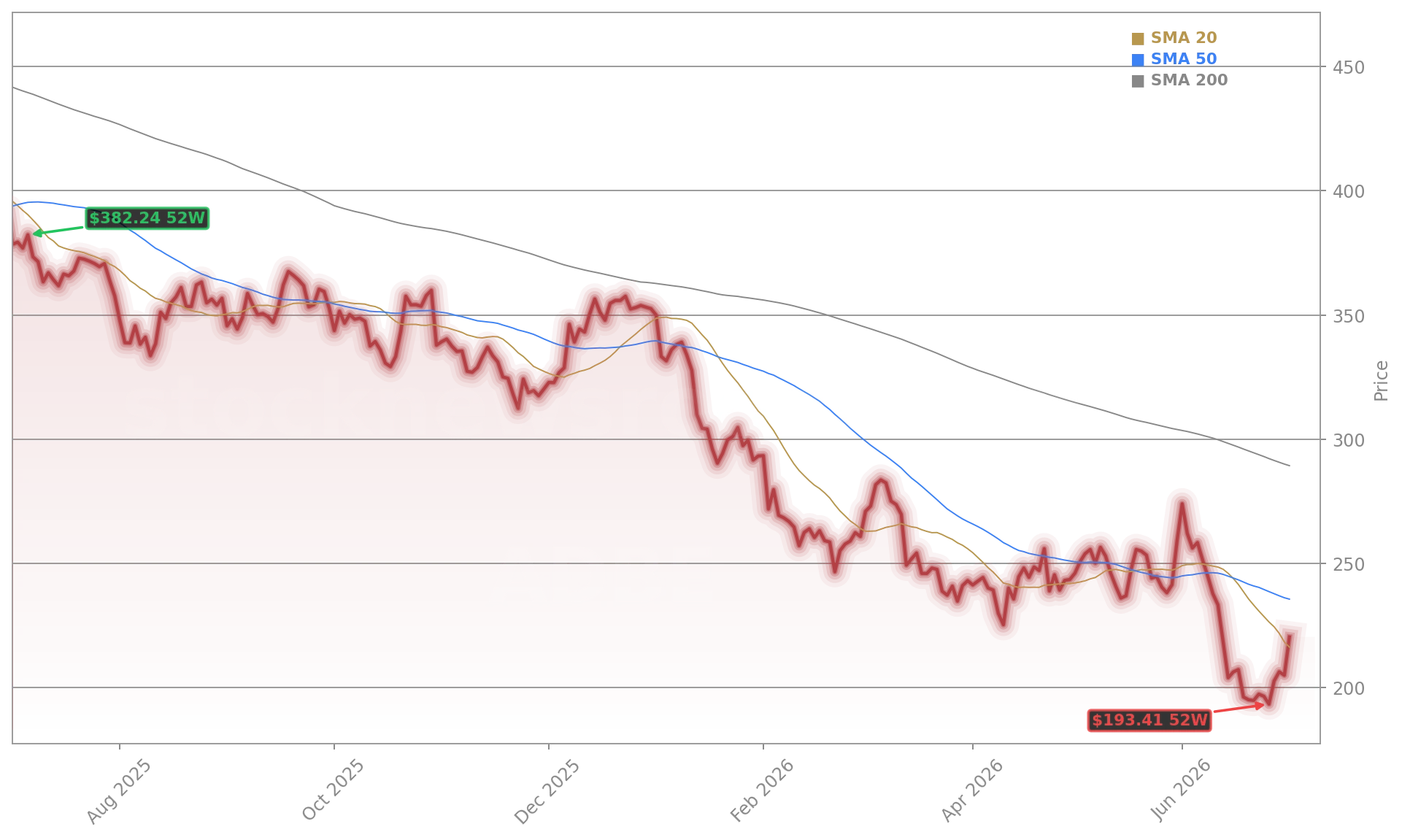

HSBC analyst Stephen Bersey upgraded Adobe Inc. to Buy from Hold on July 2, 2026, lifting the price target to $308 from $282 — implying 39% upside from the current $221.41 level. The decision follows a re-evaluation of AI competitive risk, with HSBC concluding the market has overestimated the threat from generative AI design tools. Unlike peers facing margin compression or customer churn, Adobe Inc. continues to grow revenue at 13% year-over-year, with Q2 fiscal 2026 revenue reaching $6.62 billion. Remaining performance obligations rose 13%, underscoring enterprise retention — a critical signal for S&P 500 software investors wary of AI-induced obsolescence.

Is Adobe Inc. Really Undervalued at 8x Forward P/E?

At 8.1x forward earnings, Adobe Inc. trades at a valuation rarely seen for a company of its scale, profitability, and cash flow discipline. Its non-GAAP operating margin remains robust at ~45%, well above peers like ServiceNow (NYSE:NOW) at ~32% and far ahead of newer AI-native entrants. While ServiceNow leverages agentic AI for enterprise IT workflows, Adobe Inc. anchors its AI strategy in creative continuity: Firefly-powered features embedded in Creative Cloud, plus the recent Topaz Labs acquisition to boost video and image enhancement. That contrast — workflow-centric evolution versus platform replacement — is central to HSBC’s thesis. Goldman Sachs has echoed similar themes, noting Adobe’s ecosystem is ‘sticky by design,’ not by default.

How Does This Adobe Upgrade Compare to Broader Tech?

The Adobe Upgrade arrives amid a sharp rotation in tech sentiment. Thursday’s weak June jobs report — just 57,000 jobs added — slashed Fed rate-hike odds to 20%, sending long-duration growth stocks soaring. Adobe Inc. rose 4.9%, outpacing the NASDAQ’s 1.8% gain and joining Palantir, Arm Holdings, and Robinhood in the top tier of rate-sensitive winners. By comparison, ServiceNow rose 2.1% and NVIDIA added 1.3% — underscoring how Adobe Inc.’s upgrade reflects a distinct narrative: value re-emergence, not just momentum. Unlike semiconductor or infrastructure AI names, Adobe Inc. offers near-term cash flow, $2.1 billion in quarterly buybacks, and a PEG ratio of just 0.6 — signaling deep undervaluation relative to its 14–15% earnings growth trajectory.

What’s the Real Risk — AI or Leadership?

HSBC acknowledges Adobe Inc.’s near-term headwinds: CEO succession planning and the June 15, 2026 CFO departure remain unresolved. Yet the firm sees those as manageable — not existential. More critical is the market’s misreading of competitive dynamics. Figma, Canva, and open-source AI tools haven’t dented Adobe Inc.’s ARR growth; instead, AI-first ARR crossed $500 million — tripling year-over-year. Semrush integration added $480 million in ARR, reinforcing Adobe Inc.’s marketing analytics expansion. Contrast this with Qualcomm’s recent acquisition struggles — where AI pivot execution is still unproven — and Adobe Inc.’s execution stands out. The Adobe Upgrade reflects confidence that workflow familiarity, not just feature parity, defines AI adoption in creative enterprise.

Will Other Banks Follow This Adobe Upgrade?

The market is overestimating the adverse impact of AI-based design tools on Adobe’s business. Adobe’s tools are deeply embedded in creative and enterprise workflows — users adopt AI features inside Adobe, not abandon it for competitors.— Stephen Bersey, HSBC analyst

Not all analysts agree: Phillip Securities downgraded Adobe Inc. to Neutral in late June, cutting its target to $203 from $385. But HSBC’s upgrade carries weight — especially given its track record in enterprise software analysis. With consensus earnings estimates holding steady and fiscal 2026 revenue guidance raised to $26.50–$26.60 billion, the valuation gap is widening. If Morgan Stanley or RBC Capital Markets echoes HSBC’s view on AI stickiness in the coming weeks, Adobe Inc. could become a focal point for S&P 500 rebalancing. For now, the Adobe Upgrade stands as a rare vote of confidence in a high-quality, high-margin software franchise trading at deep-cycle valuations.