Can Adobe’s record quarter and AI surge finally break the market’s skepticism around slowing organic growth?

What Did Adobe Earnings Reveal?

Adobe Inc. reported Q2 2026 revenue of $6.62 billion — up 12.7% year over year and beating consensus — with non-GAAP diluted EPS of $5.96, marking the fifth consecutive earnings beat. Annual recurring revenue (ARR) stood at $27.10 billion, while AI-first ARR tripled year over year to $500 million. Firefly ARR alone approached $300 million, growing 50% quarter over quarter. Crucially, subscription revenue rose 14% to $6.39 billion. Gross margins held firm at 88–89%, and operating cash flow totaled $2.165 billion — more than 37x capital expenditures. These Adobe Earnings confirm Adobe Inc. is not just adapting to AI — it’s monetizing it at scale.

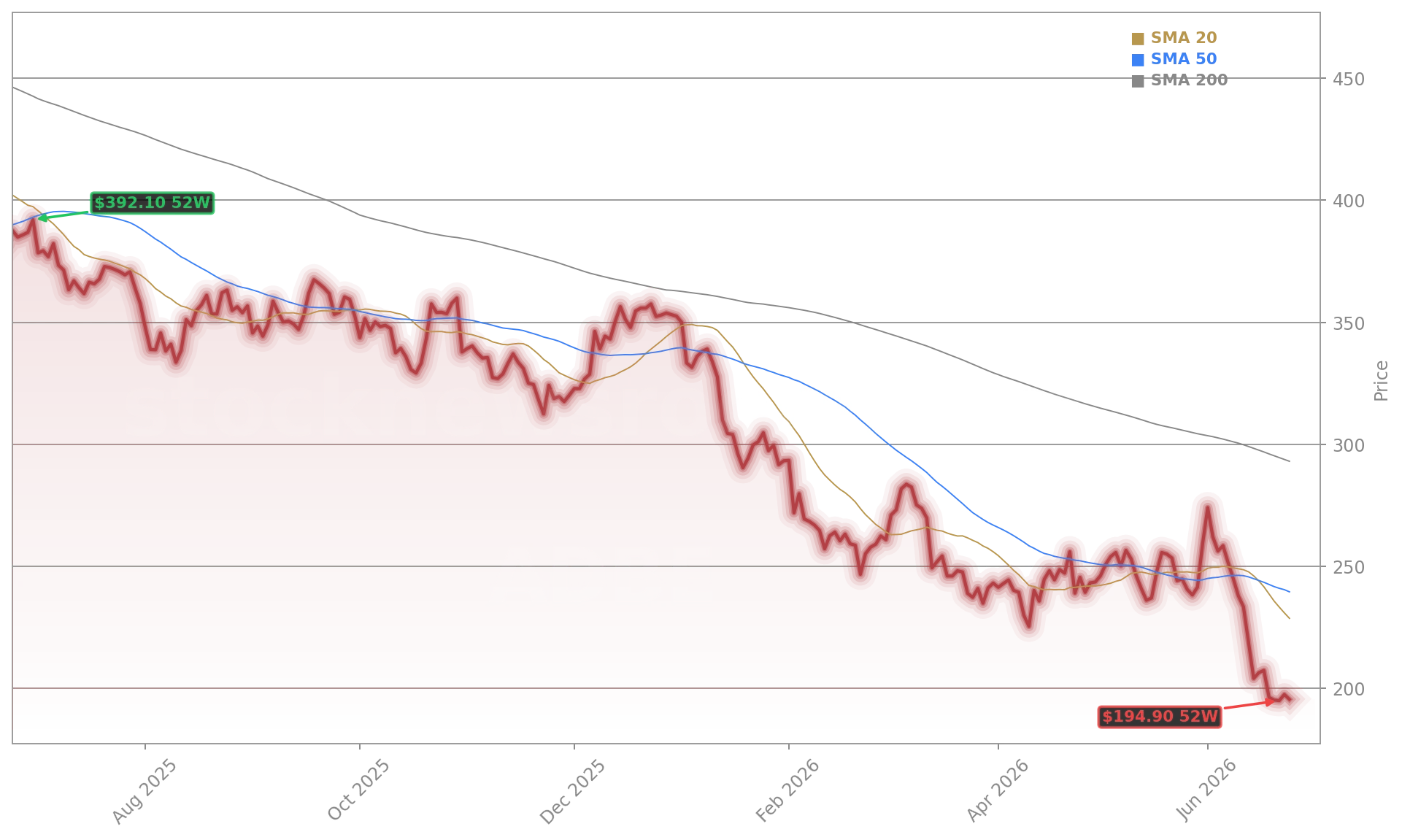

Why Is Adobe Inc. Trading at an 8x Forward P/E?

Despite robust fundamentals, Adobe Inc. trades at a forward P/E of just 8x — a multiple more typical of mature industrials than a software leader with 35.3% operating margins and a 11.2% five-year revenue CAGR. Analysts at Citigroup maintain a $282 price target, while Morgan Stanley rates the stock ‘Overweight’ citing ‘AI-driven pricing power and unmatched creative workflow integration.’ The discount reflects three near-term headwinds: the Semrush acquisition ($1.9 billion) muddying organic growth signals, a strategic pivot toward freemium user acquisition (slowing short-term ARR growth), and the CFO transition — all of which are priced in, but none of which impair the underlying cash engine.

How Does Adobe Inc. Stack Up Against Peers?

In a broader software selloff — with Salesforce, Workday, and Oracle all down over 40% year to date — Adobe Inc. stands out for operational resilience. While peers struggle with AI monetization clarity, Adobe’s AI-first ARR grew 300% YoY, dwarfing early-stage contributions from rivals. Its ROIC has risen above 9% since early 2025, a durable signal of capital efficiency. By contrast, Seeking Alpha notes Adobe’s organic ARR growth has slowed to ~8.3% — a concern echoed by bearish commentary — yet that figure still exceeds the sector median. Crucially, Adobe’s revenue per employee is widening versus peers, signaling real operational leverage — not cost-cutting optics.

What Moves the Stock Next?

Two metrics will drive near-term re-rating: organic ARR disclosure and freemium conversion velocity. Adobe Inc. has not yet separated Semrush-attributed ARR from organic growth in public filings — a transparency gap Wall Street is demanding. Meanwhile, management’s shift from ARR maximization to user acquisition hinges on conversion proof. Any quantified commentary on paid conversion rates during the Q3 earnings call will be pivotal. The AI-native valuation model from Ian Financial Vision projects a one-quarter price target of $253 — a 25% upside from current levels — contingent on clarity around those two levers. Without it, the stock may consolidate near $230, as modeled for the two-quarter horizon.

Adobe Earnings and the Broader Market Context

Creativity is an area where Adobe is uniquely qualified.— Shantanu Narayen, CEO of Adobe Inc.

Adobe Inc.’s performance matters beyond its own ticker: it’s a barometer for AI’s impact on enterprise software. As NVIDIA powers the infrastructure and Apple integrates generative tools into creative workflows, Adobe Inc. sits at the monetization nexus — turning AI capability into recurring revenue. Its $26.3 billion Amazon Prime Day sales forecast — the highest ever — also highlights Adobe’s role in measuring real-time consumer demand. That data, embedded in Adobe Analytics, feeds commerce media networks like the new LiveRamp-Adobe GenStudio integration — a $25 billion buyback-backed bet on AI-driven ad targeting. In the S&P 500’s tech-heavy rally, Adobe Inc. remains an unloved but fundamentally sound anchor.