Why did Adobe post record results and raise guidance, only to see investors send the stock sharply lower after hours?

Why Did Adobe Earnings Spark a Sell-Off?

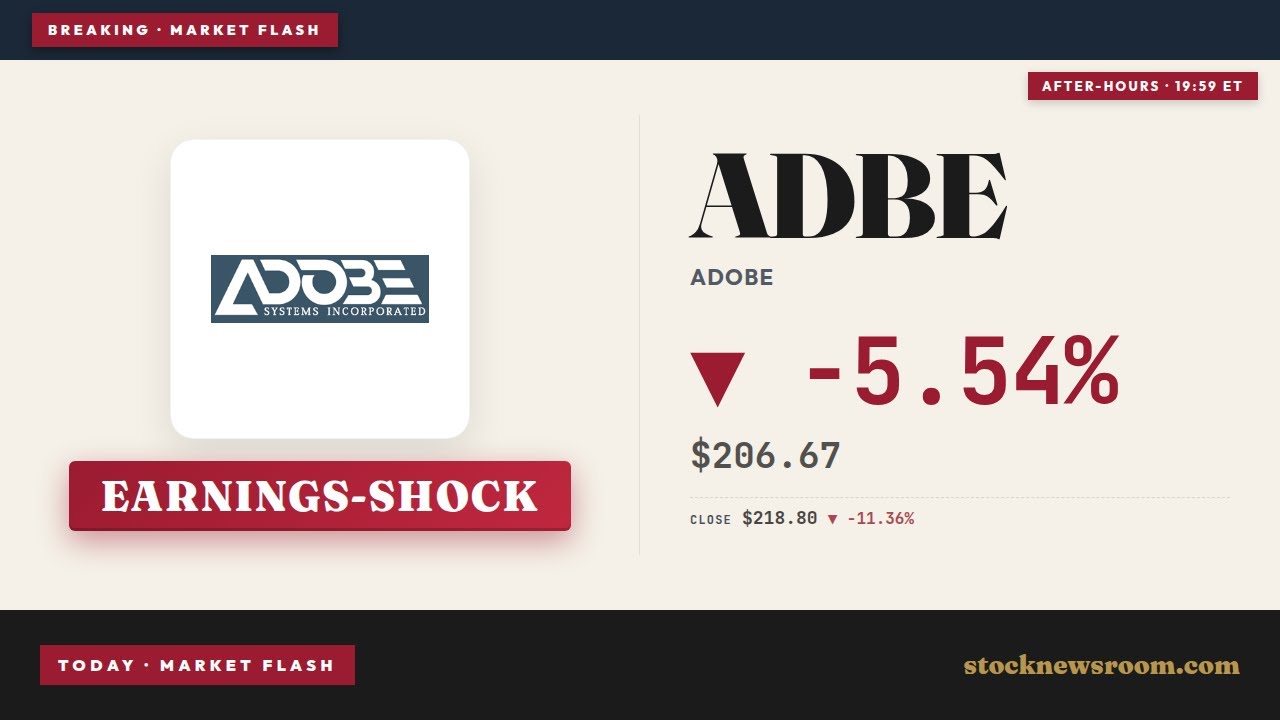

Despite record quarterly results — the highest revenue in Adobe’s history — the stock reacted negatively, dropping sharply in after-hours trading. The disconnect underscores a structural shift on Wall Street: earnings quality alone no longer suffices. Investors now demand confidence in AI strategy execution, leadership continuity, and long-term moat durability. Adobe’s $22.3 billion in remaining performance obligations signals strong underlying demand, and AI-related annual recurring revenue (ARR) rose 10% year-over-year, exceeding $500 million. Yet the departure of CFO Dan Dern on June 15 — just months after Narayen announced his exit — created a leadership vacuum that analysts say undermines near-term credibility. As Jefferies noted, the shift toward freemium AI offerings may boost monthly active users but delays recurring revenue recognition, adding transition risk.

How Does Adobe Earnings Compare to Peers?

While Adobe Earnings beat expectations, the broader software sector is under pressure. Shares of Apple and Oracle slid 10% and 5% respectively in recent sessions, reflecting broad-based rotation into hardware and infrastructure plays. Marvell Technology — where Dern is headed — is up 230% year-to-date, emblematic of Wall Street’s AI hardware bias. In contrast, Adobe has fallen 37% in 2026, trading near its lowest level since 2018. Analysts are divided: Citigroup raised its price target, RBC Capital Markets reiterated its ‘Outperform’ rating, while Stifel cut its target from $350 to $200 and downgraded Adobe to ‘Hold’. Piper Sandler also lowered its target to $240 and maintained a ‘Neutral’ stance — signaling growing caution among top-tier firms.

What’s Next for Adobe Earnings and AI Monetization?

Adobe’s Q3 guidance — $6.05–$6.10 EPS on $6.67–$6.72 billion revenue — significantly exceeds consensus, reinforcing confidence in Firefly’s commercial traction. Management emphasized AI-first product adoption across Experience Cloud Enterprise and Creative Cloud, with net new ARR accelerating in emerging markets. However, the ‘freemium’ pivot introduces near-term ARR headwinds, as Adobe prioritizes user acquisition over immediate monetization. Third Bridge analyst Dylan Koehler framed the central question starkly: ‘Can Adobe realistically position itself as the core orchestration layer for AI-driven enterprise creativity?’ With $26.5–$26.6 billion in full-year revenue guidance — above the $26.09 billion consensus — Adobe Earnings clearly reflect momentum. But execution risk remains elevated as the company navigates dual leadership transitions.

Adobe Earnings: What Does This Mean for S&P 500 and NASDAQ Investors?

Adobe delivered record revenue of $6.62 billion in Q2 reflecting strong AI-driven demand across our customer groups.— Shantanu Narayen, CEO of Adobe Inc.

Adobe Inc. is a key component of both the S&P 500 and NASDAQ Composite, and its underperformance weighs on tech-heavy indices. With software stocks broadly down — Autodesk fell 5.4% on sector-wide selloffs — Adobe’s weakness reflects a macro trend: investors favoring AI enablers (chips, cloud infrastructure) over AI application layer firms. The NASDAQ’s recent 2.1% pullback this week coincides with Adobe’s 15% five-day decline, underscoring its role as a sentiment barometer. For U.S. portfolios, Adobe Earnings highlight a critical inflection: valuation is now tethered less to earnings growth and more to leadership credibility and AI differentiation. As Barron’s observed, ‘A software executive leaving for a chip company feeds Wall Street’s downbeat narrative around software stocks.’