Can Adobe Earnings finally break the post-report selloff pattern, or will AI promises and leadership uncertainty keep investors on edge?

Will Adobe Earnings Break the Sell-the-News Cycle?

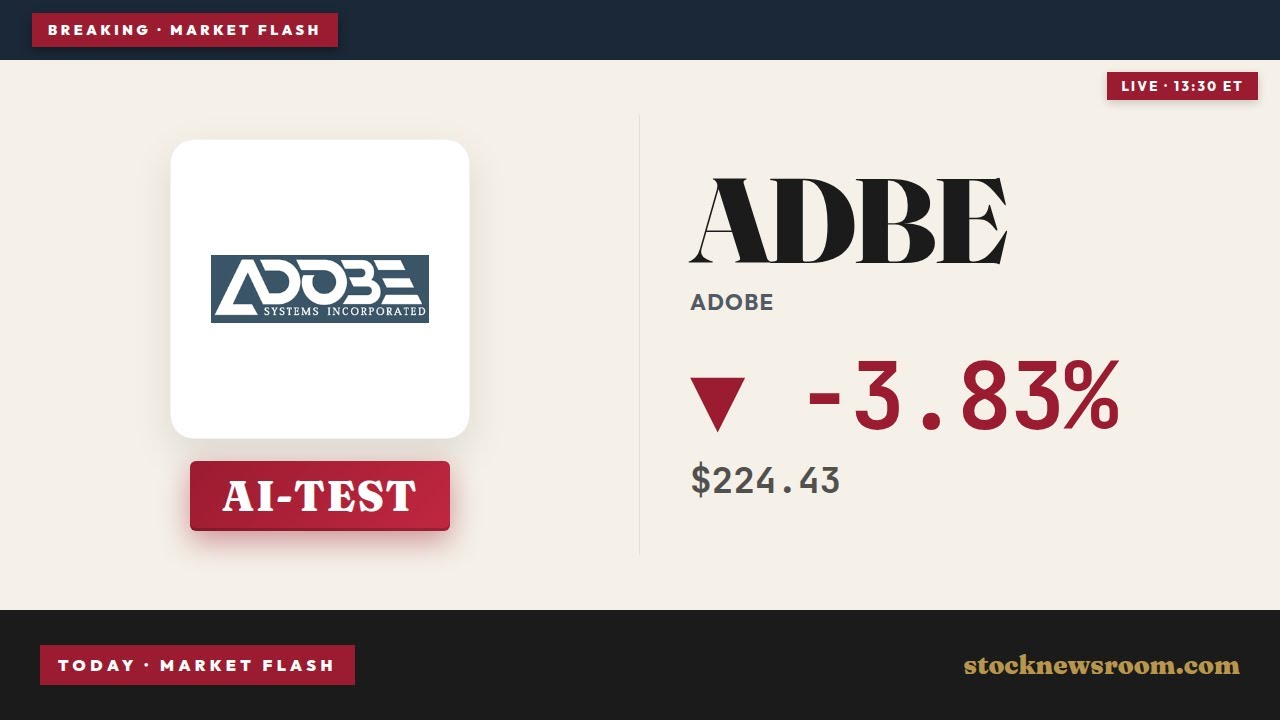

Adobe Inc. has beaten revenue estimates for 13 consecutive quarters—but shares have fallen after eight of the last 10 earnings reports. Tonight’s Adobe Earnings release arrives as the stock trades at $224.67, just above its 52-week low of $220.17 and 22.9% below its 200-day moving average. Analysts expect $5.83 in non-GAAP EPS on $6.45 billion in revenue, up 10% year-over-year—slower than Q1’s 12% growth. The real test isn’t whether Adobe hits consensus, but whether management delivers a clear ‘beat-and-raise’ and articulates a credible path for AI monetization without cannibalizing Creative Cloud’s $26.06 billion in total annual recurring revenue.

How Does Adobe Earnings Compare to Software Peers?

Relative to its Software sector peers, Adobe Inc. stands out for quality—not growth. Its 16.39% ROE is 8.7 percentage points above the industry average; EBITDA ($2.66 billion) is nearly 3x the peer median; and its debt-to-equity ratio of 0.58 is among the lowest in the group. Yet revenue growth at 11.97% lags the 23.57% sector average—dragged by deceleration in legacy publishing and competitive erosion in entry-level creative tools. Salesforce Inc. grew 13.27% on similar margins, while Palantir Technologies Inc. posted 84.71% growth—albeit on a much smaller base. Crucially, Adobe’s P/E (13.6) and P/S (4.01) ratios sit below sector averages, suggesting valuation compression rather than fundamental deterioration.

Is the CEO Transition the Real Catalyst?

Longtime CEO Shantanu Narayen’s announced retirement—coupled with insider sales of ~75,000 shares in late April—has amplified uncertainty. Anurag Rana of Bloomberg Intelligence stated that naming a successor would be ‘a big weight off the shoulders’ for investors. The leadership vacuum coincides with Adobe’s aggressive AI rollout: CX Enterprise Coworker, launched June 10, aims to automate marketing workflows across campaigns and analytics—directly competing with Microsoft and Meta’s AI-powered ad platforms. Yet without a clear successor, the market remains skeptical. Stifel analyst J. Parker Lane maintained a Buy rating but cut his price target to $350 from $400, citing ‘execution risk around leadership transition and AI integration.’

What Do Analysts Say Ahead of Adobe Earnings?

Of the 37 analysts covering Adobe Inc., 17 rate it Buy, 17 Hold, and 3 Sell—reflecting deep division. TD Cowen’s Derrick Wood lowered his target to $285 from $310 while holding a Hold rating, noting ‘AI momentum is real, but it will take time to bend the growth curve.’ Mizuho Securities reiterated a Hold with a $321.32 average price target. Meanwhile, UBS trimmed its target to $260 from $290 on April 17, citing ‘macro headwinds and AI-related competitive intensity.’ Notably, no major firm has upgraded Adobe Inc. ahead of tonight’s print—underscoring Wall Street’s wait-and-see stance. The options market implies an 8–9% move post-earnings, with key resistance at $259 and support near $224.

What’s at Stake for the S&P 500 and NASDAQ?

Longer term, the key question is whether Adobe can realistically position itself as the core orchestration layer for AI-driven enterprise creativity.— Dylan Koehler, Third Bridge analyst

Adobe Inc. is a core NASDAQ-100 constituent and a bellwether for enterprise software sentiment. Its 5% intraday drop today led the index’s losers—outpacing declines from Salesforce and Intuit. With the 10-year yield near 4.53% and macro pressures mounting, high-duration software names face mounting multiple compression. If Adobe Earnings confirm AI-driven ARR expansion without revenue trade-offs—and if management provides clarity on leadership—the stock could catalyze a broader rotation into quality software names ahead of H2. But failure to reset expectations risks deepening the ‘SaaSpocalypse’ narrative and dragging down peers like Autodesk and Workday.