Can Adobe defend its creative empire as AI tools get cheaper, faster, and good enough for millions of users?

Is Adobe’s Core Business Under AI Siege?

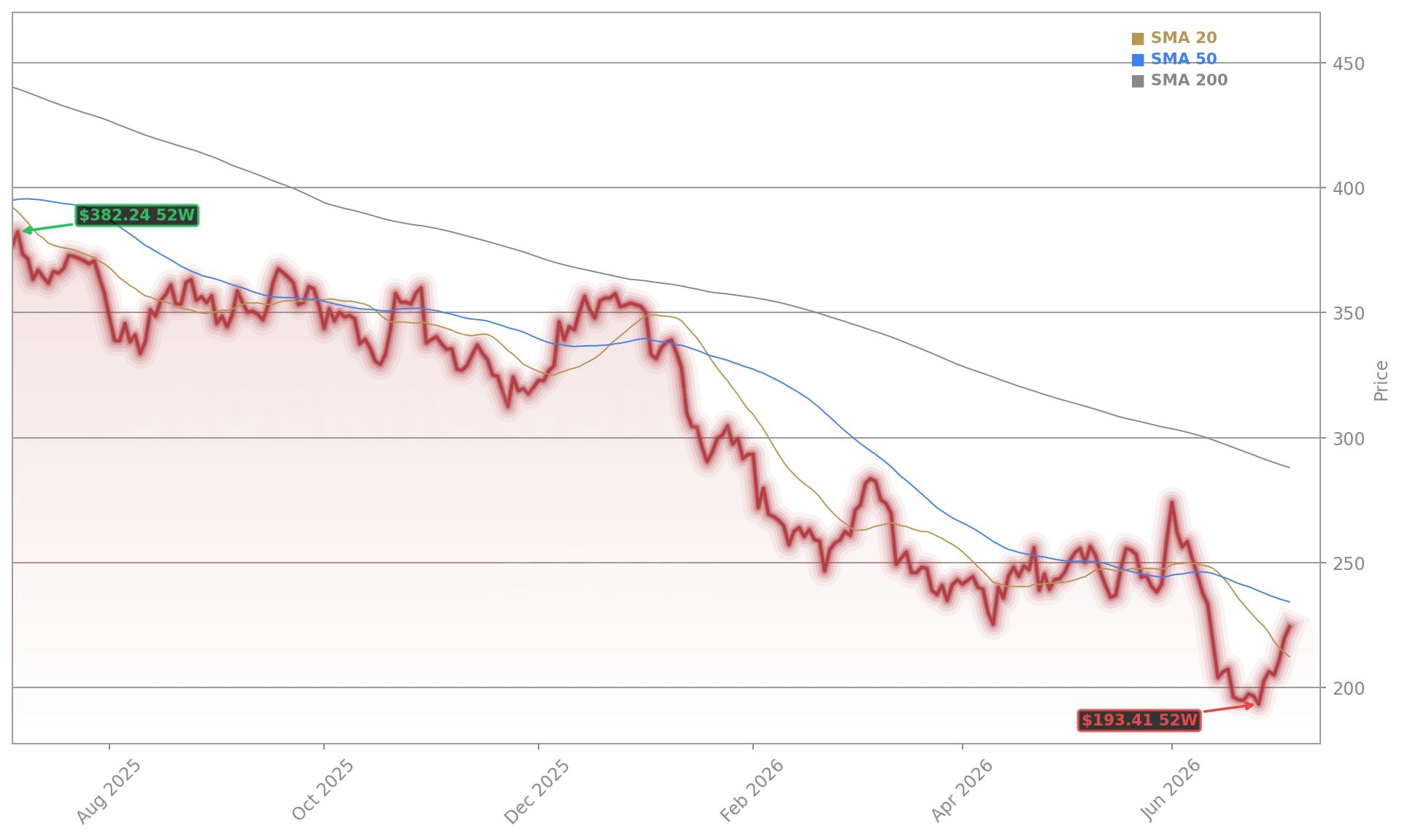

Bank of America’s Tuesday downgrade — led by analyst Tal Liani — marks a stark reversal from its prior Buy rating and signals growing consensus that Adobe’s traditional per-seat licensing model faces unprecedented headwinds. Liani argues that rapid advances in large-language models and AI-native tools now deliver ‘good enough’ creative output at zero or near-zero cost, eroding pricing power and seat expansion in enterprise accounts. This directly threatens Adobe’s core revenue engine: Photoshop, Premiere Pro, and Acrobat subscriptions remain dominant, but less sophisticated users and even some professionals are migrating to lower-cost alternatives. The warning isn’t theoretical — Adobe’s stock has fallen 38% year-to-date, significantly underperforming the NASDAQ and S&P 500.

What Does the Adobe AI Forecast Say About Growth?

The Adobe AI Forecast now projects decelerating annual recurring revenue (ARR) growth in Q3 2026, with management explicitly acknowledging that its freemium push — centered on Firefly and Express — is suppressing near-term individual subscriber growth. While user acquisition is surging, monetization lags. HSBC counters with a $308 price target, calling Adobe’s AI tools ‘additive, not cannibalistic,’ but that view remains in the minority: only 33% of analysts currently rate Adobe a Buy. Meanwhile, Figma — recently upgraded to Buy by Bank of America at $30 — is gaining traction with its usage-based AI monetization model, where 75% of over-limit enterprise users repurchased AI credits in Q1. That contrast sharpens the Adobe AI Forecast debate: can Adobe pivot from seat-based to consumption-based pricing without sacrificing margins?

How Does Adobe Compare to AI-Exposed Peers?

Adobe’s AI vulnerability stands in marked contrast to peers like NVIDIA, whose data center GPUs power the very AI models disrupting creative workflows. While NVIDIA (NVDA) surged 22% in Q2 2026 on AI infrastructure demand, Adobe’s software layer faces margin compression. Similarly, Meta’s AI-integrated ad tools and Apple’s on-device generative features highlight how incumbents are embedding AI without abandoning core revenue — a path Adobe is still navigating. Notably, AMD’s AI forecast was slashed to -6.7% amid valuation concerns, underscoring that AI exposure cuts both ways: enablers benefit, while legacy software faces scrutiny. Adobe’s 3.2x forward sales multiple — less than half of Figma’s 7.6x — reflects Wall Street’s skepticism about its AI monetization velocity.

Are Adobe Dips Historically Rewarding?

History offers caution: since 2010, Adobe has suffered 12 intramonth drops of 20% or more. Only six delivered positive 12-month returns, with a median loss of 4%. Buyers faced a median further drawdown of 17% before recovery — and waited 99.5 days on average for peak returns. That pattern suggests the current 38% YTD decline may not be a simple ‘buy-the-dip’ opportunity. Unlike cyclical tech pullbacks, this correction is tied to a structural shift — and the Adobe AI Forecast must now account for both competitive displacement and Adobe’s ability to re-architect its business model in real time.

What’s Next for Wall Street’s Adobe AI Forecast?

Investors await Adobe’s Q3 2026 guidance update in mid-August — a critical test of whether freemium adoption is translating into conversion or merely diluting ARR. With Bank of America’s $190 target representing a 15% downside from current levels, and HSBC projecting upside to $308, the Adobe AI Forecast remains sharply bifurcated. Yet the broader context is clear: in an AI-driven creative economy, defensibility no longer comes from feature depth alone — it comes from workflow integration, real-time collaboration, and adaptive pricing. Adobe’s ability to deliver on that triad will define its next chapter on Wall Street.

Rapid improvements in [large-language models] and AI-native tools increasingly deliver ‘good enough’ creative output at low or zero cost.— Tal Liani, Bank of America Securities

Related Coverage: Has Wall Street misread Adobe’s AI risk so badly that this Adobe Upgrade +4.9%: HSBC Turns Bullish on AI Fears could mark the start of a major rerating? Meanwhile, AMD AI Forecast -6.7% as Valuation Fears Hit AI Momentum shows how AI narratives are fracturing across the semiconductor and software sectors — a reminder that not all AI exposure is created equal.