Can Adobe AI Strategy turn enterprise AI buzz into real growth before investors lose patience completely?

What Does Brand Visibility Mean for Adobe’s AI Strategy?

Adobe Brand Visibility is the first unified solution combining Semrush’s AI visibility intelligence with Adobe’s agentic content optimization — built directly into Adobe CX Enterprise. It gives marketers access to nearly 300 million real-world AI search prompts (the largest global database), audience reach metrics, competitive share-of-voice data, and owned-channel insights across ChatGPT, Google AI Mode, Microsoft Copilot, and Perplexity AI. Unlike legacy SEO tools, it closes the loop between insight and action: AI agents surface prioritized optimizations, teams deploy updates in minutes, and impact ties directly to bookings and pipeline via Adobe Analytics integrations. This isn’t incremental — it’s foundational infrastructure for Generative Engine Optimization (GEO), positioning Adobe not just as a creative toolmaker but as an AI surface operating system.

How Does This Compare to Meta and NVIDIA?

While Meta pours billions into AI infrastructure and open-weight models — and NVIDIA dominates the hardware layer powering those models — Adobe is carving a distinct enterprise moat: context-aware brand orchestration. Where Meta focuses on AI-native discovery and NVIDIA on compute scale, Adobe targets the $2.4 trillion digital experience stack — where brand consistency, compliance, and workflow integration matter more than raw inference speed. Competitors like Canva or Runway lack Adobe’s depth in rights management, approval workflows, and enterprise-grade governance — critical for Fortune 500 marketing teams. Still, Citigroup analysts note that Adobe’s current valuation premium over peers like Salesforce (CRM) remains unjustified without clear ARR lift from GEO within the next two quarters.

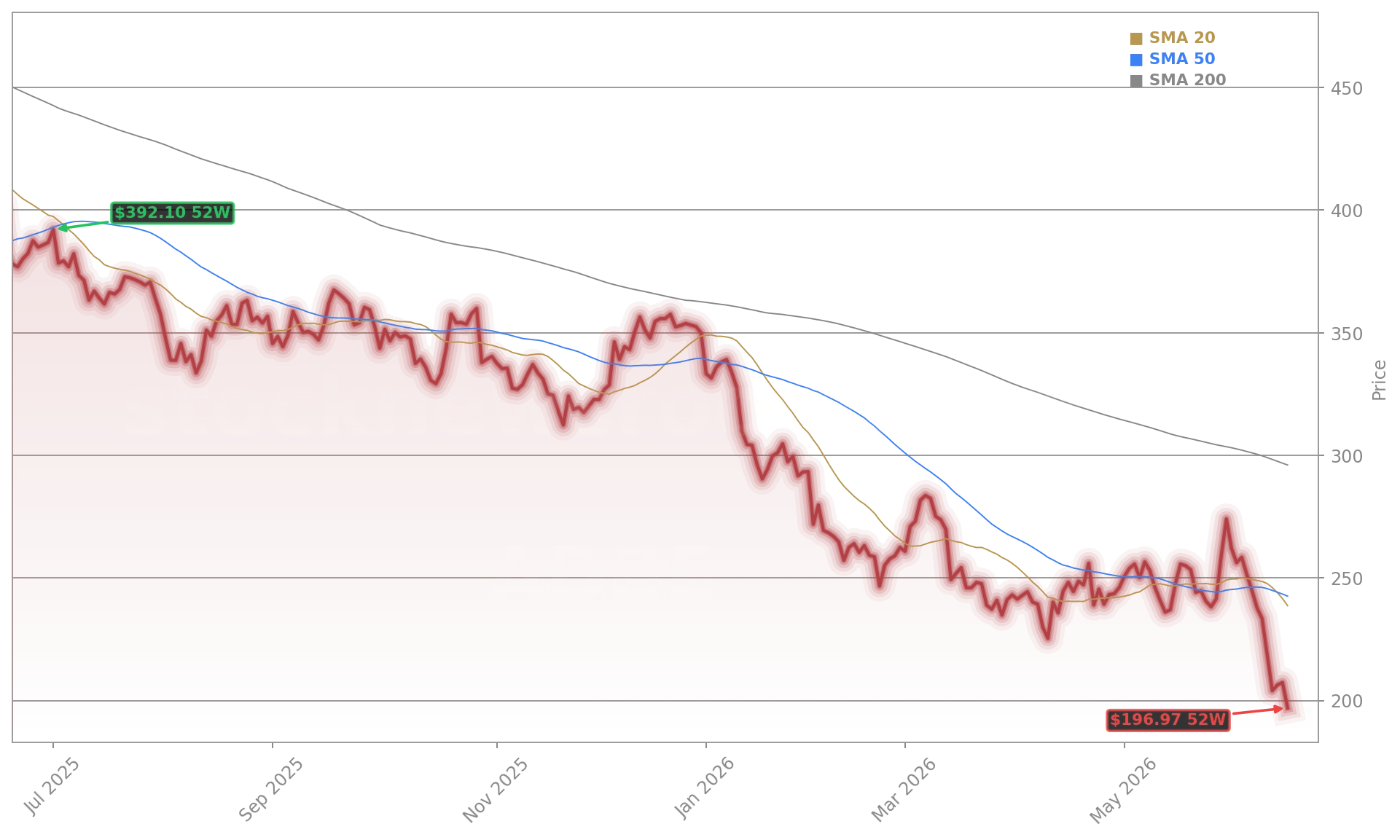

Why Did Wall Street Yawn at Record Q2 Results?

Adobe reported $6.62 billion in Q2 revenue — beating consensus — and raised full-year guidance to $20.5–$20.6 billion. Yet shares plunged 6.25% after hours on June 12. Why? Management confirmed a strategic pivot: accelerating freemium adoption on Creative Cloud and delaying price hikes to drive user acquisition — sacrificing near-term revenue for long-term AI engagement. Evercore ISI downgraded Adobe from Outperform to In Line and slashed its price target from $325 to $225. Piper Sandler’s Billy Fitzsimmons cut his target from $280 to $240 while maintaining Neutral. TD Cowen’s Derrick Wood held his Hold rating but warned that third-party credit card data shows only 1.5% YoY growth — down sharply from prior quarters — signaling softening demand momentum.

Is Adobe’s Adobe AI Strategy Enough to Reverse the Slide?

In a world where customers often interact with an AI tool before ever reaching a business’s website, visibility is everything now.— Anil Chakravarthy, President, Customer Experience Orchestration Business, Adobe

The answer hinges on execution velocity and monetization clarity. Adobe’s KI metrics are strong: Acrobat’s AI assistant ARR tripled; Firefly-generated assets quadrupled; GenStudio ARR grew >25%. But Wall Street wants to see those users convert — not just engage. The company’s new LinkedIn-powered ‘AI Essentials for Marketers’ initiative — available in 47 languages — signals urgency in upskilling the very buyers who must justify Adobe’s spend. Yet Goldman Sachs cautions that Adobe faces steeper competition in AI-powered marketing than in traditional creative software, especially from integrated stacks like HubSpot and emerging vertical AI vendors. With the stock down 48% over 12 months and trading near its 52-week low, investor patience is thin — and every quarter now carries make-or-break weight for the Adobe AI Strategy.