Did Adobe just prove its AI strategy is finally turning investor skepticism into real revenue growth?

Did Adobe Earnings Beat Analyst Expectations?

Yes — decisively. Adobe Inc. reported adjusted earnings per share of $5.96, exceeding the FactSet consensus estimate of $5.82 — a 2.4% beat. Revenue totaled $6.62 billion, well above the $6.45 billion analysts had forecast, representing a 13% year-over-year increase. The $170 million revenue beat and $0.14 EPS beat mark Adobe’s 14th consecutive quarter of revenue outperformance. Notably, the company’s non-GAAP EPS of $5.96 also surpassed the $5.83 estimate cited across multiple pre-earnings summaries, including those from Barrons and Bloomberg Intelligence.

How Did the Stock React to Adobe Earnings?

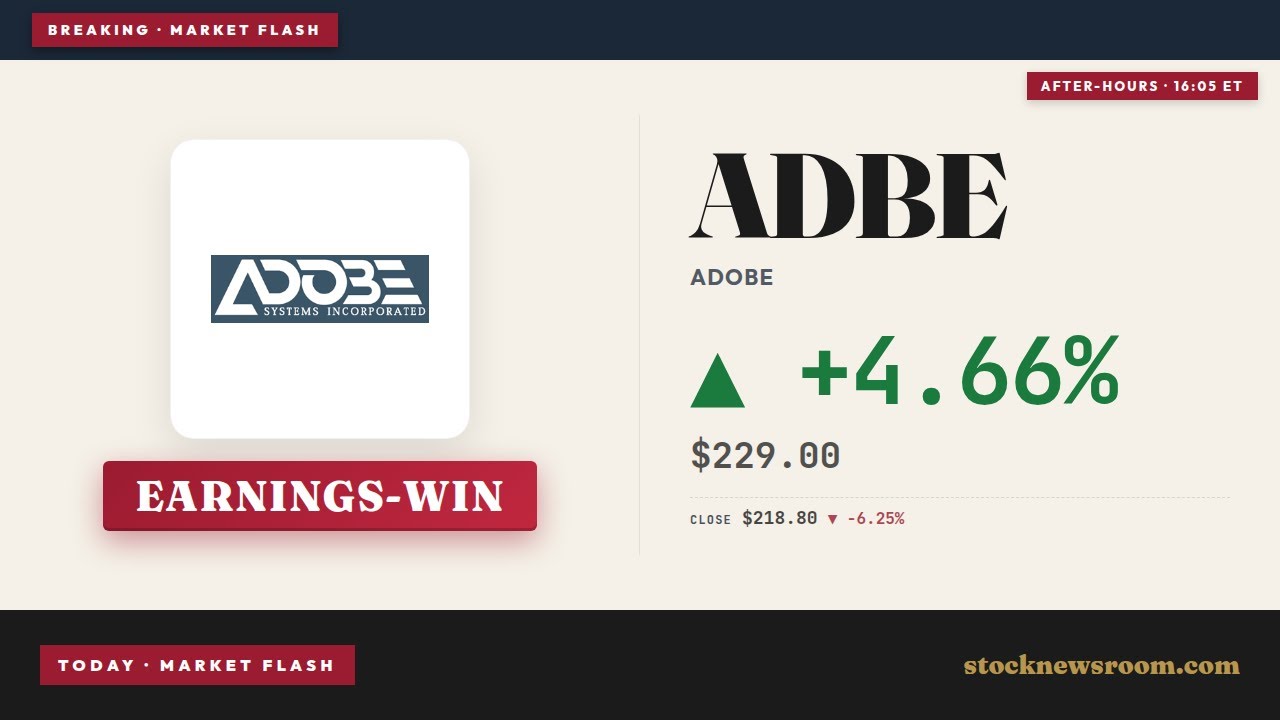

Adobe Inc. (ADBE) rose 4.66% in after-hours trading to $229.00, following an intraday close at $218.80 — a 6.25% decline. The post-earnings rebound reversed an initial dip and marked a notable departure from Adobe’s recent pattern: the stock had fallen after eight of its last 10 earnings reports, with an average day-of decline of nearly 5%. The positive reaction appears tied directly to the magnitude of the beat and the raised outlook — not just headline numbers, but tangible evidence of AI monetization accelerating. The $229.00 after-hours price remains well below the 52-week high of $328.21 but sits above the 52-week low of $220.17, signaling renewed technical stability.

What Guidance and Metrics Did Adobe Provide?

Adobe Inc. lifted its full-year fiscal 2026 outlook: revenue guidance was increased to $26.5 billion–$26.6 billion, up from $25.9 billion–$26.1 billion, and adjusted EPS guidance rose to $24.35–$24.45, from $23.30–$23.50. For Q3, Adobe forecast adjusted EPS of $6.05–$6.10 on revenue of $6.67 billion–$6.72 billion — both ranges meaningfully above Wall Street’s $5.77 EPS and $6.52 billion revenue estimates. Annualized recurring revenue (ARR) stood at $27.1 billion, including $480 million from the April-acquired Semrush Holdings. Remaining performance obligations (RPO) totaled $22.3 billion, up year-over-year. CEO Shantanu Narayen stated: “Adobe delivered record revenue of $6.62 billion in Q2 reflecting strong AI-driven demand across our customer groups.” Separately, CFO Dan Durn announced his departure effective June 15; Steve Day, SVP of Corporate Finance, will serve as interim CFO.

How Did Analysts and Media React to Adobe Earnings?

Citigroup raised its price target on Adobe Inc. and reiterated a Buy rating, citing “stronger-than-expected AI monetization and resilient core subscription growth.” RBC Capital Markets reiterated its Outperform rating and upgraded its FY26 EPS forecast, calling the guidance raise “a clear signal of confidence in AI-first execution.” In contrast, Stifel and TD Cowen maintained their Buy and Hold ratings respectively but lowered price targets — Stifel to $350 and TD Cowen to $285 — citing ongoing valuation pressure and leadership uncertainty. Barrons highlighted the paradox: “Adobe reported record results… yet shares slid initially,” reflecting investor fatigue with AI promises absent leadership clarity. CNBC analysts emphasized the “double beat-and-raise” as a rare catalyst in a subdued software sector, while Bloomberg Intelligence underscored the Adobe Earnings as “the first clear inflection point for AI revenue traction in enterprise creative software.”

What Does This Mean for Adobe’s AI Strategy?

Adobe Earnings confirmed AI is no longer just a feature — it is becoming a revenue engine. AI-first annual recurring revenue grew meaningfully, with Firefly-powered tools and CX Enterprise adoption accelerating across enterprise clients. Total AI-related ARR increased 10% year-over-year, and the $27.1 billion ARR figure — $450 million above consensus — validates Adobe’s “flywheel” strategy integrating rights-cleared, commercially safe AI into Creative Cloud, Acrobat, and Experience Cloud. While rivals like Alphabet, Canva, and Figma pressure the entry-level creative market, Adobe’s enterprise moat, deep integration, and monetization of AI-as-a-service appear intact. The Semrush acquisition further strengthens Adobe’s brand visibility and marketing analytics stack — a strategic hedge against AI commoditization. With $25 billion in authorized buybacks remaining and margins holding near 30%, Adobe’s fundamentals remain elite — even as its valuation stays compressed at ~14x forward P/E.

Related Coverage: Analysts are closely comparing Adobe’s AI execution to Alphabet’s massive $85 billion AI funding push — Alphabet AI Funding: $85B Raise Fuels Google AI Boom explores whether compute scale can translate to enterprise monetization. Meanwhile, Adobe Earnings +3.6% After Hours: Can AI Calm Bears? examines whether this quarter finally breaks Adobe’s post-report selloff pattern — and whether investors will reward durability over disruption. These narratives converge on one question: can Adobe’s flywheel outpace AI-native competition?

Adobe delivered record revenue of $6.62 billion in Q2 reflecting strong AI-driven demand across our customer groups.— Shantanu Narayen, CEO of Adobe Inc.

Adobe Earnings for Q2 2026 represent a pivotal validation — not just of financial resilience, but of Adobe’s ability to embed generative AI into high-value, mission-critical workflows without cannibalizing its core. The raised outlook, robust ARR, and strong AI monetization metrics position Adobe Inc. for renewed investor confidence heading into the second half. With leadership transition now in motion and AI revenue crossing meaningful thresholds, the next catalyst is clear: sustained execution in Q3. For long-term investors, Adobe Earnings confirm the company remains a high-quality compounder — and Adobe Earnings may finally catalyze the re-rating the stock has long deserved.