Can Adobe’s AI pivot justify investor patience before leadership changes and freemium pressure turn a bold strategy into a valuation trap?

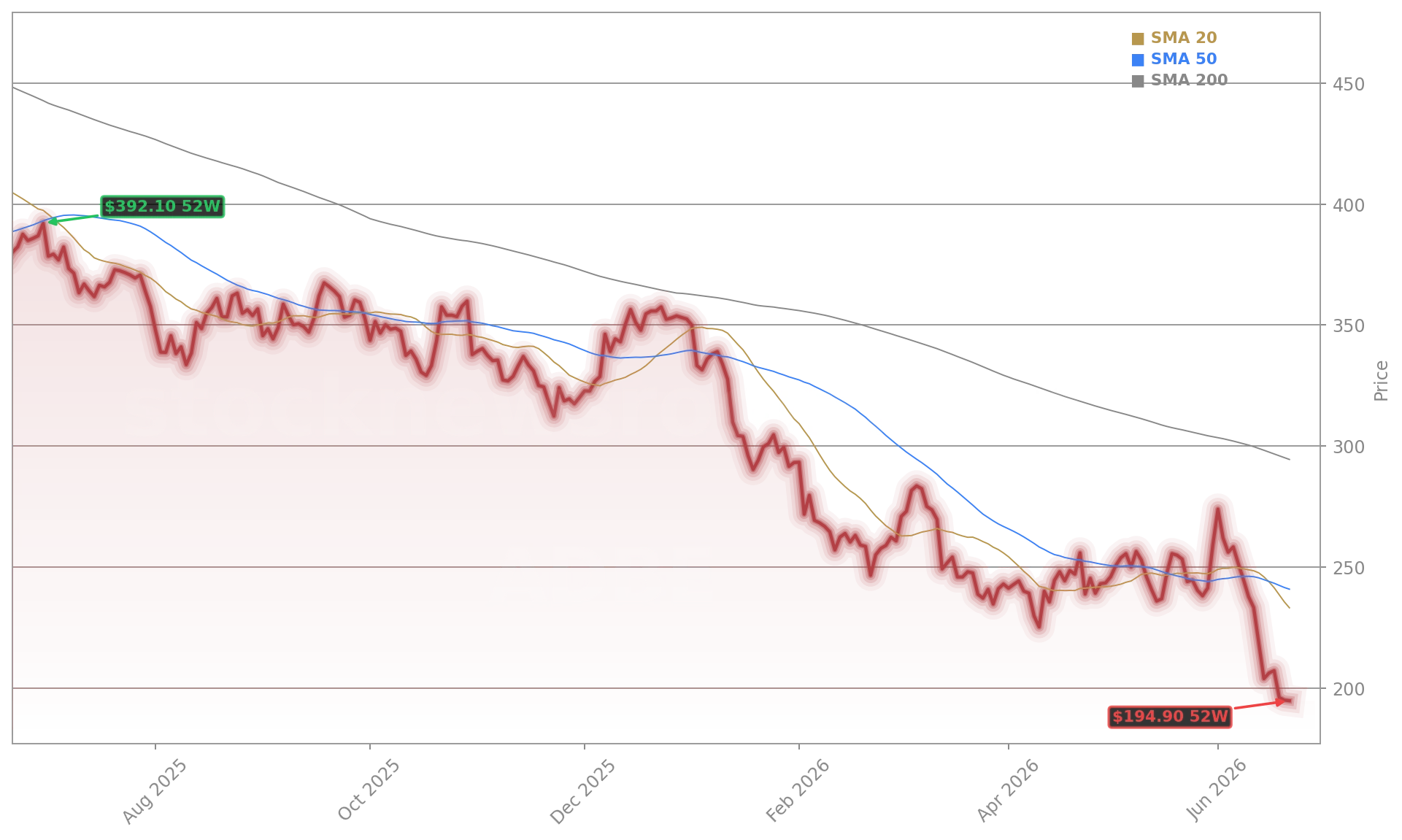

Why is Adobe Inc. trading near its 52-week low?

Adobe Inc. closed Tuesday at $194.90 — down 0.13% — and remains 31.6% below its 200-day moving average. That’s stark contrast to the S&P 500, which trades near all-time highs. The underperformance isn’t driven by macro weakness but by company-specific headwinds: CFO Dan Durn’s June 15 departure, CEO Shantanu Narayen’s announced transition after 18 years, and a deliberate shift toward freemium AI tools that’s cutting into near-term annual recurring revenue (ARR) growth. Citi analyst Tyler Radke cut his price target from $264 to $228 and cited ‘more signs of disruption,’ estimating a $500 million reduction in Adobe’s organic 2026 ARR outlook. UBS followed with a $225 target and neutral rating, citing weakening pricing power. The market isn’t punishing Adobe for missing numbers — it’s punishing the company for trading short-term cash flow for long-term AI scale.

What does the new Adobe AI Strategy actually deliver?

The Adobe AI Strategy now centers on two pillars: embedded generative AI in core creative tools and enterprise-grade agentic infrastructure. On June 18, Adobe launched Firefly-powered AI assistants in public beta across Photoshop, Premiere, Illustrator, InDesign, and Frame.io — with After Effects in private beta. More significantly, Adobe unveiled CX Enterprise Coworker, a new platform designed to let brands automate content creation, activation, and measurement across channels. Integrated with Microsoft Copilot, Anthropic’s Claude, Google Gemini, and Slack, it positions Adobe as the ‘agentic infrastructure layer’ — not just a toolmaker but an orchestration hub. That vision attracted major partners: Accenture, WPP, Omnicom, and Stagwell’s Code and Theory are co-innovating on AI-powered customer experience solutions. Yet monetization remains opaque: Adobe has not announced pricing for Firefly’s advanced workflows, and conversion metrics from its 90 million Creative Freemium users remain unaudited.

How do peers like NVIDIA and Apple frame Adobe’s AI risk?

While NVIDIA powers the AI stack and Apple embeds on-device intelligence, Adobe faces a dual threat — disruption from vertical AI tools (like Canva’s AI design suite) and commoditization by foundational models. Value investor Tobias Carlisle framed Adobe alongside Booking Holdings as a ‘platform facing existential AI questions,’ arguing its 8x forward P/E and 0.53 PEG ratio reflect excessive discounting of adaptation risk. J.P. Morgan analysts lowered their target from $420 to $340 but affirmed the pivot is ‘deliberate’ — trading near-term ARR for long-term upside. That contrasts sharply with how Wall Street views AI enablers: NVIDIA trades at 32x trailing P/E with consensus expecting 35% revenue growth, while Adobe’s 13% YoY top-line growth is viewed as fragile. The divergence highlights a key portfolio dynamic: investors reward AI infrastructure, but demand proof of AI monetization from application-layer players.

Is Adobe Inc. still a buy for U.S. investors?

With $27.1 billion in total ARR, 35.3% operating margins, and $2.17 billion in Q2 operating cash flow, Adobe’s fundamentals remain elite. Its $25 billion buyback program — $2.1 billion executed in Q2 alone — signals deep confidence. Yet investor hesitation is rational: the consensus ‘Hold’ rating from 38 S&P Global analysts reflects uncertainty, not disapproval. Phillip Securities analyst Paul Chew maintains a ‘Buy’ rating, citing ‘solid ARR momentum and attractive valuation.’ But Freedom Broker downgraded to ‘Hold’ from ‘Buy,’ slashing its target from $510 to $250 and declaring Adobe is now in a ‘show-me phase.’ With Q3 guidance ($6.67–6.72B revenue) matching consensus and the next earnings report due September 10, the next 90 days will test whether freemium users convert — and whether new leadership can execute the Adobe AI Strategy without losing core enterprise trust.

Maybe that’s where Adobe really shines, that you can do all of the idea creation and really simple stuff in ChatGPT or whatever LLM you use, while complex editing remains Adobe’s domain.— Tobias Carlisle

Related Coverage: Adobe’s AI ambitions face mounting scrutiny — Adobe AI Strategy: Stock Drops 5% as AI Push Faces Doubts. Meanwhile, enterprise software peers like Salesforce are confronting similar monetization challenges — Salesforce Acquisition: Why the $3.6B Deal Isn’t Helping.