Can Salesforce Acquisition revive confidence, or is Wall Street signaling a deeper AI-era problem for the software giant?

Why is Salesforce Acquisition not calming Wall Street?

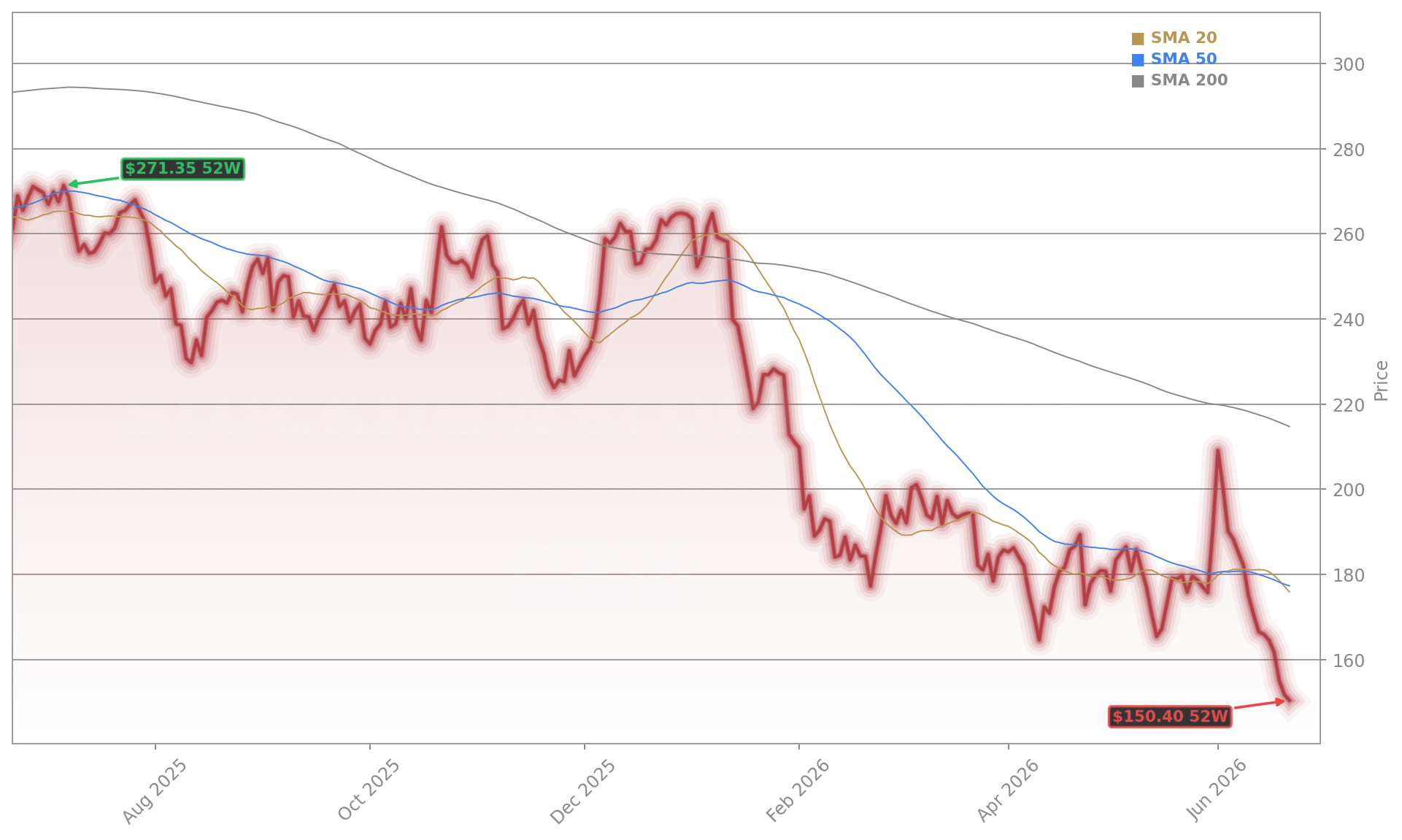

Salesforce Inc. announced its $3.6 billion acquisition of Fin — the AI agent platform formerly known as Intercom — to accelerate its Agentforce strategy and boost autonomous customer service resolution from 62% to 76%. Yet the deal has done little to arrest the bleeding: CRM shares plunged 2.3% on Monday, extending its losing streak to 14 consecutive sessions — the longest in the company’s 22-year public history, per Dow Jones Market Data. The stock now trades at $147.82, down 59.8% from its December 2024 all-time high of $367.87. With the NASDAQ up 12% YTD and the S&P 500 gaining 9%, Salesforce’s underperformance stands in stark contrast to peers like ServiceNow and Microsoft — both up over 25% this year.

What’s driving the record selloff?

The core issue isn’t execution — it’s existential. AI agents threaten the foundational SaaS pricing model. As Jefferies noted, Salesforce’s 15 acquisitions since May 2025 have fueled innovation, but investors now question whether per-seat licensing can survive in an era where customers build custom agents using open-source models. Salesforce’s shift toward consumption-based pricing is underway, yet revenue growth remains muted: Q1 2026 revenue totaled $11.1 billion — flat year-over-year — while free cash flow stood at $11 billion (26% of sales). Meanwhile, rival Oracle reported a $638 billion AI infrastructure backlog, highlighting divergent investor sentiment toward infrastructure vs. application-layer AI plays.

How do analysts view the Salesforce Acquisition?

Monness Crespi analyst Brian White upgraded Salesforce Inc. to ‘Buy’ from ‘Neutral’ on June 20, citing a ‘compelling’ valuation at just 10x next year’s expected earnings of $15.50. His $200 price target implies 34% upside from current levels. Yet White explicitly tied the call to the stock’s 42% YTD decline — calling CRM ‘the second-worst performing stock in our coverage universe in 2026.’ Similarly, Citigroup reiterated its ‘Neutral’ rating but raised its price target to $185, emphasizing integration execution risk. With 40 ‘Buy’ or equivalent ratings among 54 firms tracked by FactSet — and an average target of $244.58 — Wall Street remains bullish on long-term potential, even as short-term sentiment collapses.

Is this a buying opportunity — or a structural warning?

Institutional ownership now exceeds 80%, and the Employees Provident Fund Board recently acquired nearly 900,000 shares — a sign of deep-value conviction. Still, technicals remain dire: CRM is trading below both its 50-day ($99.24) and 200-day ($136.78) moving averages, with an RSI of 30 — officially oversold. Yet the selloff reflects more than sentiment: Salesforce Inc. faces structural headwinds shared with Intuit and Workday — AI commoditization, pricing pressure, and a 63-person layoff in San Diego that contradicted prior ‘no-layoffs’ pledges. With $25 billion in authorized share buybacks underway, capital discipline is intact — but earnings turnaround remains the missing catalyst.

What’s next for Salesforce Acquisition and Wall Street?

Integration of Fin is expected to complete by Q4 fiscal 2027, with Fin CEO Eoghan McCabe staying onboard to lead the rollout. Meanwhile, Salesforce Inc. must prove Agentforce can drive measurable revenue uplift beyond pilot deployments — especially as competitors like ServiceNow embed AI agents directly into workflow automation. For U.S. investors holding tech-heavy portfolios, the Salesforce Acquisition serves as both a warning and a test case: Can legacy SaaS leaders reinvent themselves before AI agents render their platforms optional? With Q2 2026 earnings due in late August, the next quarterly report will be the first real litmus test of whether the Fin acquisition delivers tangible traction — or merely delays the inevitable.

Salesforce has ‘earned the unflattering title as the second-worst performing stock in our coverage universe in 2026.’— Brian White, Monness Crespi

Related Coverage: For deeper analysis of Salesforce’s Q1 financials and AI revenue growth versus its strategic risks, see Salesforce Earnings: $11.1B Revenue Meets AI Warning. On how infrastructure-focused rivals like Oracle are capturing AI spend, read Oracle AI Infrastructure Hits $638B Backlog as Capex Jumps.