Can Salesforce Acquisition momentum in AI and Europe reverse CRM’s sharp slide, or is Wall Street still unconvinced?

What Does the Salesforce Acquisition Mean for AI Leadership?

Salesforce Inc. closed its $3.6 billion acquisition of Fin — an AI-native customer service platform — on June 15, marking its most significant Salesforce Acquisition since the $27.7 billion Informatica purchase in 2023. Unlike prior integrations, Fin delivers pre-built, compliant AI agents trained on enterprise support data, enabling immediate deployment across service clouds without custom model tuning. According to Needham, which raised its price target to $400 — the highest on Wall Street — the deal accelerates Salesforce’s path to $10 billion in AI-related annual recurring revenue by fiscal 2028. That ambition aligns with Nvidia’s recent enterprise agent push, where Salesforce joined Adobe and Cisco as foundational partners building ‘teams of specialized agents’ for treasury, compliance, and payments automation.

Why Is Europe Suddenly a $3 Billion Priority?

Just days after expanding its AI center in London, Salesforce Inc. pledged $2 billion to France through 2030 — including a new AI Innovation Hub in Paris — and separately announced a $1 billion investment in Italy to open a Milan-based AI engineering hub at Palazzo Missori. These moves reflect a deliberate recalibration: while U.S. cloud adoption matures, European enterprise AI spend is projected to grow at 38% CAGR through 2027 (per IDC), outpacing North America by 9 points. For investors, this isn’t just regional diversification — it’s infrastructure for GDPR-compliant, sovereign AI deployment, a critical advantage over rivals like Oracle and Microsoft as EU AI Act enforcement ramps up.

Is Salesforce Acquisition Fueling Real Revenue Acceleration?

Yes — but selectively. AI-related revenue from Agentforce and Data 360 hit $3.4 billion annualized in Q1 2026, up over 200% year over year. Excluding the $1.1 billion Informatica contribution, organic AI growth approached 100%. Crucially, Agentforce alone crossed $1 billion in annualized run rate — growing 205% YoY. That growth now accounts for over 40% of Salesforce’s incremental revenue. With current remaining performance obligations up 14%, management reaffirmed fiscal 2027 revenue guidance of $45.9–$46.2 billion (11% growth at midpoint) and signaled acceleration in H2 2027. Goldman Sachs, RBC Capital Markets, and Barclays all raised price targets in early June — Goldman’s $242 target implies 50% upside from current levels.

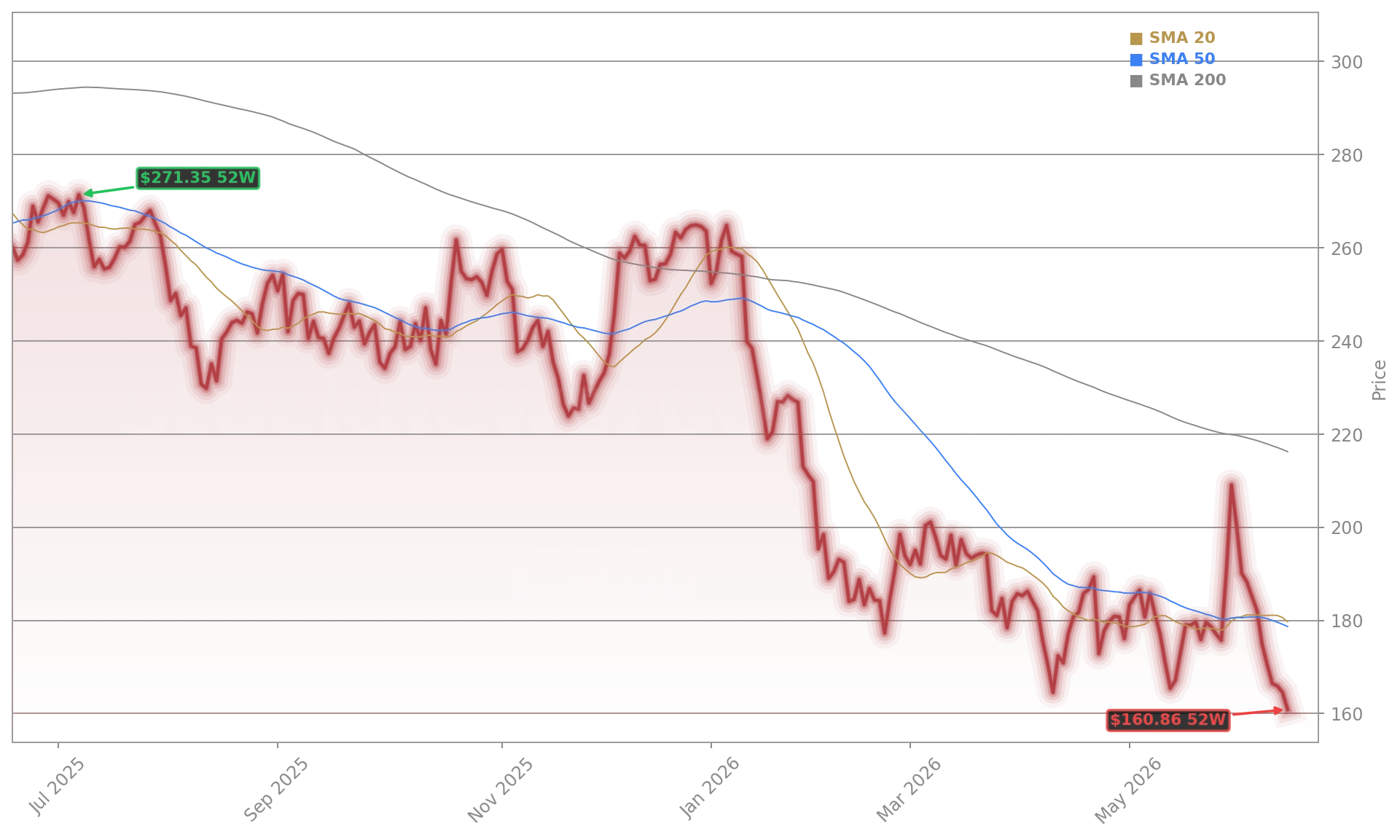

How Are Analysts Reacting to the Salesforce Acquisition & Slide?

Despite CRM’s 38.7% year-to-date drop and record 11-day losing streak — its worst since 2004 — analyst conviction remains strong. Cantor Fitzgerald reiterated its Buy rating with a $250 target. Canaccord Genuity maintained its Buy rating and $225 target. Needham’s $400 target reflects confidence that the Salesforce Acquisition strategy will drive margin expansion and revenue inflection by late 2026. As Dan Ives of Wedbush noted: ‘Data is the new oil — and Salesforce is securing the refineries.’ Still, the disconnect between fundamentals and price has widened: CRM now trades at under 12x fiscal 2027 EPS — cheaper than the S&P 500’s 21x average and below peers like Apple and NVIDIA.

We are proud to deepen our commitment to France with this significant investment. France has become one of the world’s great centers of AI innovation, combining extraordinary research talent, entrepreneurial energy, and a strong commitment to trusted technology.— Marc Benioff, Chair and CEO of Salesforce Inc.

Related Coverage: Salesforce’s $3.6 billion Fin deal is under intense scrutiny — Salesforce Acquisition $3.6B Deal Tests Its AI Strategy analyzes whether this move finally validates its agentic vision. Meanwhile, the broader AI infrastructure race is heating up — AMD AI Infrastructure Jumps +4% After Rackspace AI Deal shows how chip and software players are racing to lock in enterprise AI contracts before Q3 earnings season.