Can Salesforce finally turn AI hype into visible growth, or are investors right to keep doubting the story?

Why are Salesforce Earnings still under pressure?

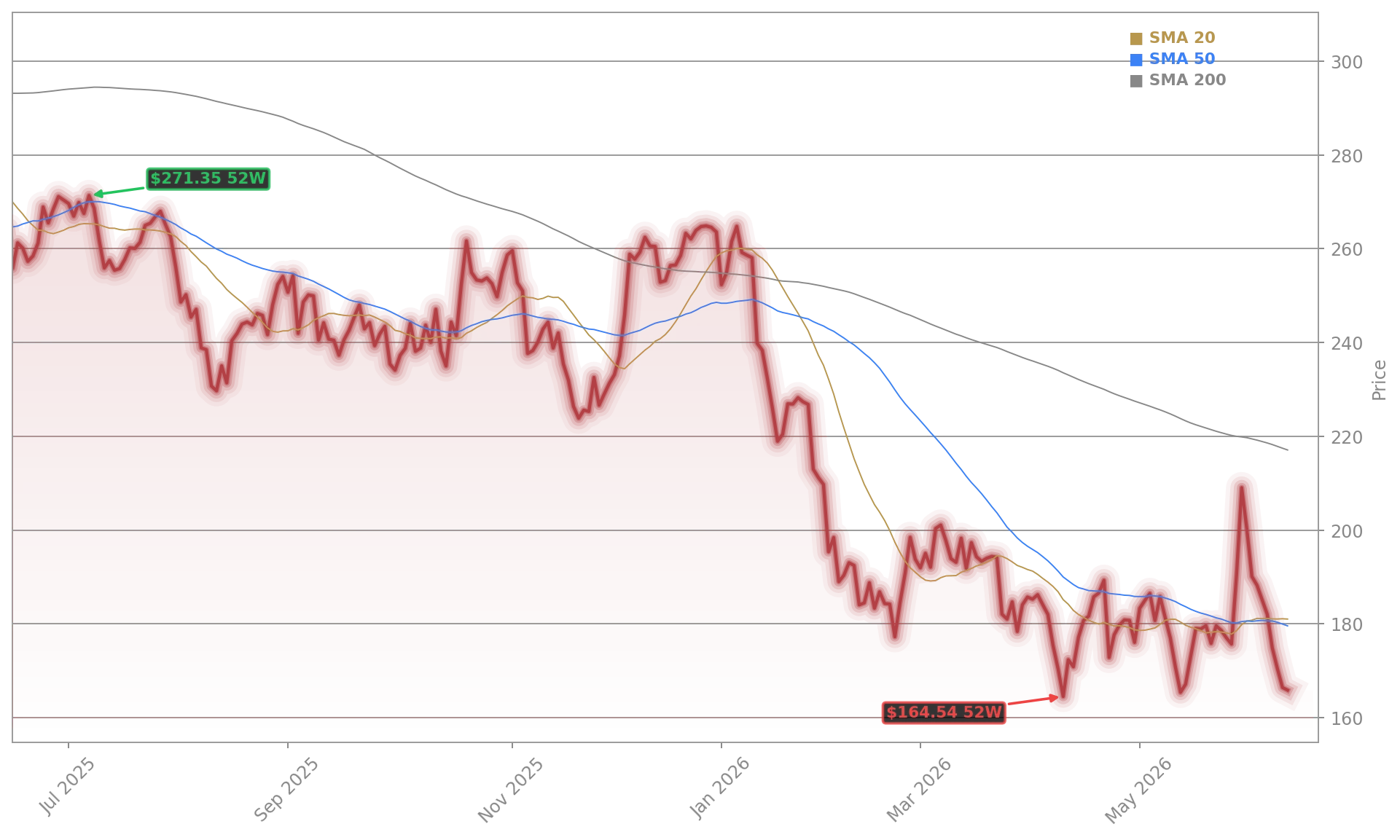

Salesforce Earnings looked solid on the surface. The company delivered revenue of about $11.2 billion, reported net income of roughly $1.94 billion, raised its full-year profit outlook, and paired the report with a major repurchase authorization that has been described at up to $25 billion, while commentary around buybacks has also highlighted a broader $27 billion figure. Yet the stock reaction around the release showed investors wanted more than financial engineering and headline beats.

The core issue is growth quality. Organic revenue growth in constant currency was around 7.5%, and annual contract value trends disappointed. That fed a broader concern that Salesforce is still struggling to reaccelerate its core enterprise sales engine even as AI enthusiasm lifts much of the software sector. Investors appear willing to reward cleaner AI winners, especially platform and infrastructure leaders such as NVIDIA, while demanding clearer proof from application software names.

Can Salesforce prove its AI revenue story?

Management said annualized AI revenue has reached about $1.2 billion, with Marc Benioff pointing to more than $1 billion in recurring revenue tied to AI and agents. That sounds meaningful in isolation, but the market is asking a tougher question: why is that momentum not yet obvious in reported growth, bookings, or customer expansion?

That skepticism has centered on Agentforce. Some enterprise users testing agent-based tools have not yet seen compelling return on investment, and the company’s AI narrative remains more promotional than visible in the numbers. In a market that increasingly compares software claims with large real-world AI spending, Salesforce’s figures look modest next to infrastructure-heavy demand seen elsewhere. That is one reason the company keeps getting asked to explain AI monetization more carefully, even as customers like CVS Health expand deployments in regulated industries using Agentforce Health and Slack.

The debate also touches execution. Several investors still see go-to-market issues lingering from the period after former co-CEO Keith Block left, especially in large enterprise selling. For Wall Street, that makes Salesforce Earnings less about one quarter and more about whether management can rebuild confidence in durable demand.

What are analysts saying about Salesforce?

Analyst reactions have been mixed rather than uniformly negative. Guggenheim maintained a Hold rating on Salesforce. Truist Financial analyst Terry Tillman reiterated a Buy rating and a $280 price target, arguing the company still has meaningful upside despite the post-report questions. William Blair also maintained a Buy view, while broader consensus data compiled in market coverage continues to show a Moderate Buy profile with an average target near $259.47. TradingView data published this week showed the 12-month average target falling to $248.67, still implying notable upside from recent levels.

That gap between bullish price targets and skeptical trading action helps explain today’s setup. Shares are bouncing intraday, but investors remain unconvinced that Salesforce deserves the same premium multiple as faster AI-linked software names like Snowflake or ecosystem leaders such as Apple and Tesla that are easier to frame within broader technology leadership narratives.

Related Coverage: StockNewsRoom recently examined the first-wave market reaction in Salesforce Earnings at $11.13B: Strong Quarter, AI Doubts. That piece argued the quarter itself was not disastrous, but that guidance and AI visibility were the real tests for investor patience. The same tension remains in focus today as Wall Street weighs earnings stability against a still-unproven acceleration story.

Salesforce Earnings show a company that is profitable, shareholder-friendly, and still highly relevant in enterprise software, but not yet winning the AI credibility battle. For investors, the next key test is whether AI revenue starts showing up in stronger bookings and organic growth. If management can turn Agentforce adoption into visible top-line momentum, sentiment could improve quickly.

Fazit folgt.