Is this Salesforce Upgrade the start of a real rerating, or just a brief rebound after Wall Street priced in too much AI fear?

Why did Guggenheim issue a Salesforce Upgrade?

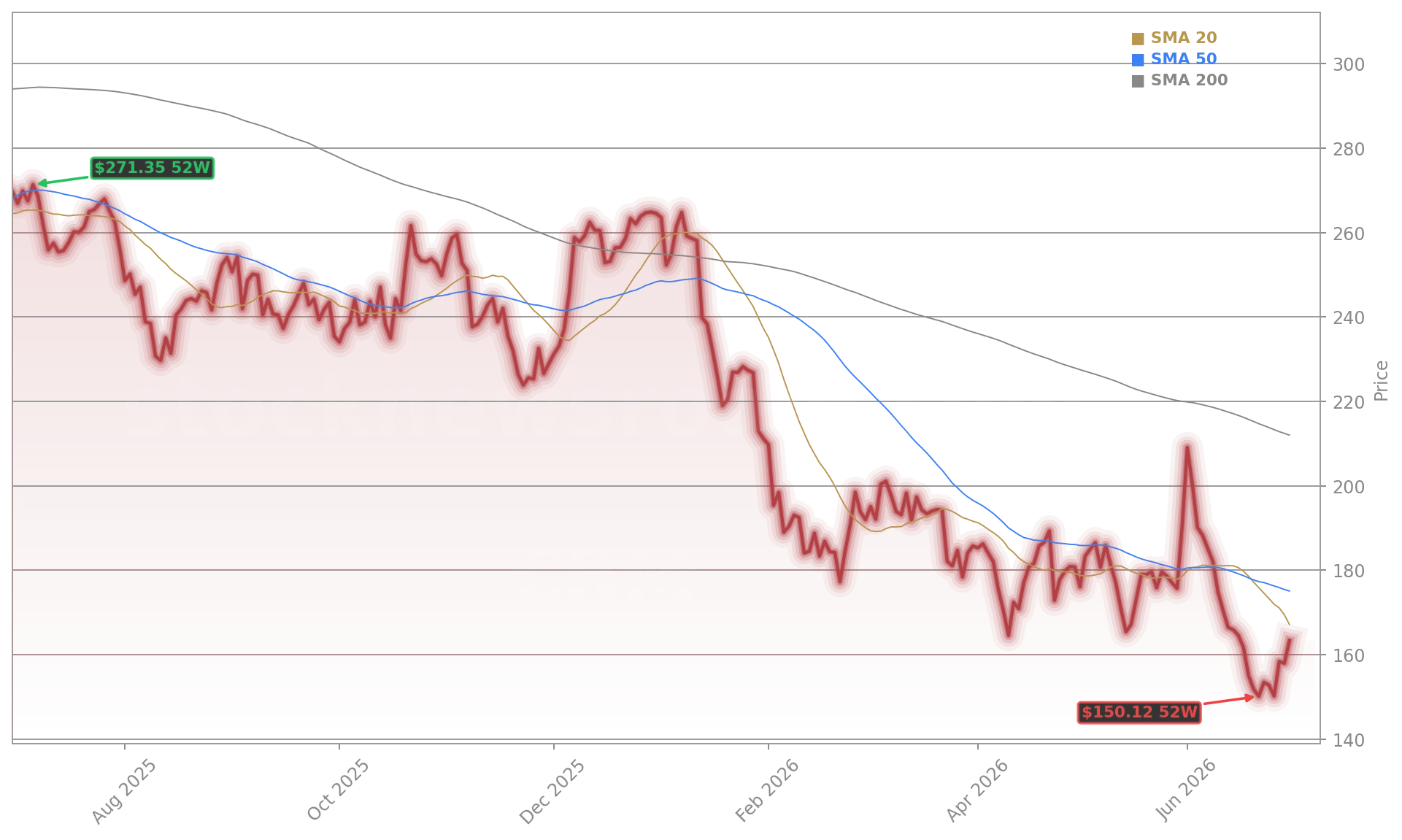

Guggenheim analyst John DiFucci upgraded Salesforce Inc. to Buy from Neutral on July 1, 2026, setting a $228 price target — a 38% premium to its $164.40 close. DiFucci explicitly dismissed the ‘Armageddon scenario’ priced into CRM, calling it ‘misaligned with reality’ and labeling AI-doom narratives ‘a hallucination.’ His call wasn’t rooted in AI optimism — he conceded AI agents pose ‘a significant risk’ to legacy SaaS models — but in valuation discipline: CRM trades 43% below its July 2025 52-week high of $209.06 and 12.3% above its March 2026 low of $146.32, creating what DiFucci termed ‘an attractive entry point.’ The upgrade coincided with a broader rebound in enterprise software, as ServiceNow gained 7.2% on its own Guggenheim Buy rating and $125 target.

How does CRM compare to AI winners like NVIDIA and Meta?

While NVIDIA fell 9.4% and chip stocks broadly declined — with Applied Materials down 9.9% and Lam Research off 11% — CRM surged alongside Meta, which jumped 9.7% on news of its cloud-AI capacity play. The divergence highlights Wall Street’s recalibration: AI isn’t a monolithic tailwind. Where hardware and neoclouds like CoreWeave (-13%) faced pressure, software firms adapting to AI — not just enabling it — gained traction. Salesforce’s $3.6 billion acquisition of Fin, announced June 15, is central to this narrative: Fin’s agentic AI models will integrate into Agentforce 360, accelerating deployment for SMBs. Unlike Palantir, which benefits directly from AI’s complexity, Salesforce faces cloning risk — yet Guggenheim argues its scale, data moat, and Slack-powered workflow integration create defensibility.

What does the Salesforce Upgrade mean for the S&P 500?

Salesforce Inc. contributed approximately 57 points to the Dow Jones Industrial Average’s 132-point intraday gain — underscoring its outsized role in blue-chip tech. Its rally helped lift the broader S&P 500 software cohort: Workday and AppLovin ranked among the index’s top gainers, while the iShares Expanded Tech-Software ETF outperformed the VanEck Semiconductor ETF despite broad tech weakness. This isn’t isolated — Citigroup recently reiterated its Overweight rating on Salesforce Inc., citing ‘resilient renewal rates and cross-sell momentum in Data Cloud,’ while RBC Capital maintains a ‘Sector Perform’ rating but acknowledges ‘strong Q2 2026 execution in commercial segments.’ The Salesforce Upgrade thus reflects not just CRM-specific optimism but a sector-wide reassessment: AI disruption is real, but survivable for incumbents with embedded workflows and trusted data layers.

Is the Salesforce Upgrade justified by fundamentals?

Yes — but conditionally. Salesforce Inc. reported Q2 2026 revenue of $9.2 billion, up 11% year-over-year and 3% above consensus, with operating margin expanding to 28.4%. Its Customer 360 platform now serves over 150,000 customers, and Agentforce adoption grew 40% quarter-over-quarter. Yet growth in new logo acquisition slowed to 7% — down from 14% in Q1 — validating AI concerns. Guggenheim’s thesis rests on two pillars: first, CRM’s current 22x forward P/E is near a 5-year low, discounting zero AI upside; second, acquisitions like Fin and partnerships — such as the Visa Cash App Racing Bulls Formula One deal — prove rapid AI integration is operational, not theoretical. The $228 target implies 26x forward P/E, still below the S&P 500 software sector median of 29x.

What’s next after this Salesforce Upgrade?

Investors now await Salesforce Inc.’s Q3 2026 guidance update on August 20, where management will address Fin integration timelines and Agentforce monetization. Near-term catalysts include the anticipated Q4 2027 close of the Fin acquisition and expanded Slack-AI co-selling with Microsoft. Longer term, Salesforce Inc. must prove it can monetize AI agents faster than startups like Bending Spoons — whose IPO surged 13% Wednesday — can replicate core workflows. For now, Guggenheim’s Salesforce Upgrade has shifted the narrative: CRM isn’t AI-proof, but it’s AI-resilient — and priced for failure, not adaptation.

The Armageddon scenario currently priced into the stock is misaligned with reality.— John DiFucci, Guggenheim analyst

Related Coverage: Analysts are split on whether Salesforce’s $3.6 billion Fin acquisition signals strategic agility or desperation — read Salesforce Acquisition: Why the $3.6B Deal Isn’t Helping. Meanwhile, as chip stocks waver, Wall Street’s AI target surge continues: AMD Forecast -5.2%: Warning as Wall Street Lifts Targets explores whether semiconductor weakness is a pause or a pivot.