Can Salesforce’s booming AI revenue calm investors, or is Wall Street still too worried about what AI could do to software pricing?

What Did Salesforce Earnings Actually Show?

Salesforce Inc. reported fiscal Q1 2027 revenue of $11.1 billion, up 13% year over year—though 4.4 percentage points stemmed from the Informatica acquisition. Organic growth held steady in the high-single-digit range, consistent with recent trends. More compelling was the AI momentum: Salesforce’s AI and data products generated $3.4 billion in annual recurring revenue (ARR), a 200% jump from a year earlier. Its Agentforce agentic AI platform alone crossed $1 billion in ARR after more than tripling. Crucially, seat counts in core products—including Sales Cloud and Service Cloud—grew year over year, with both human users and AI agents expanding on the platform. As CFO Robin Washington stated on the earnings call, this dual growth pattern challenges the prevailing narrative that AI will cannibalize per-seat licensing.

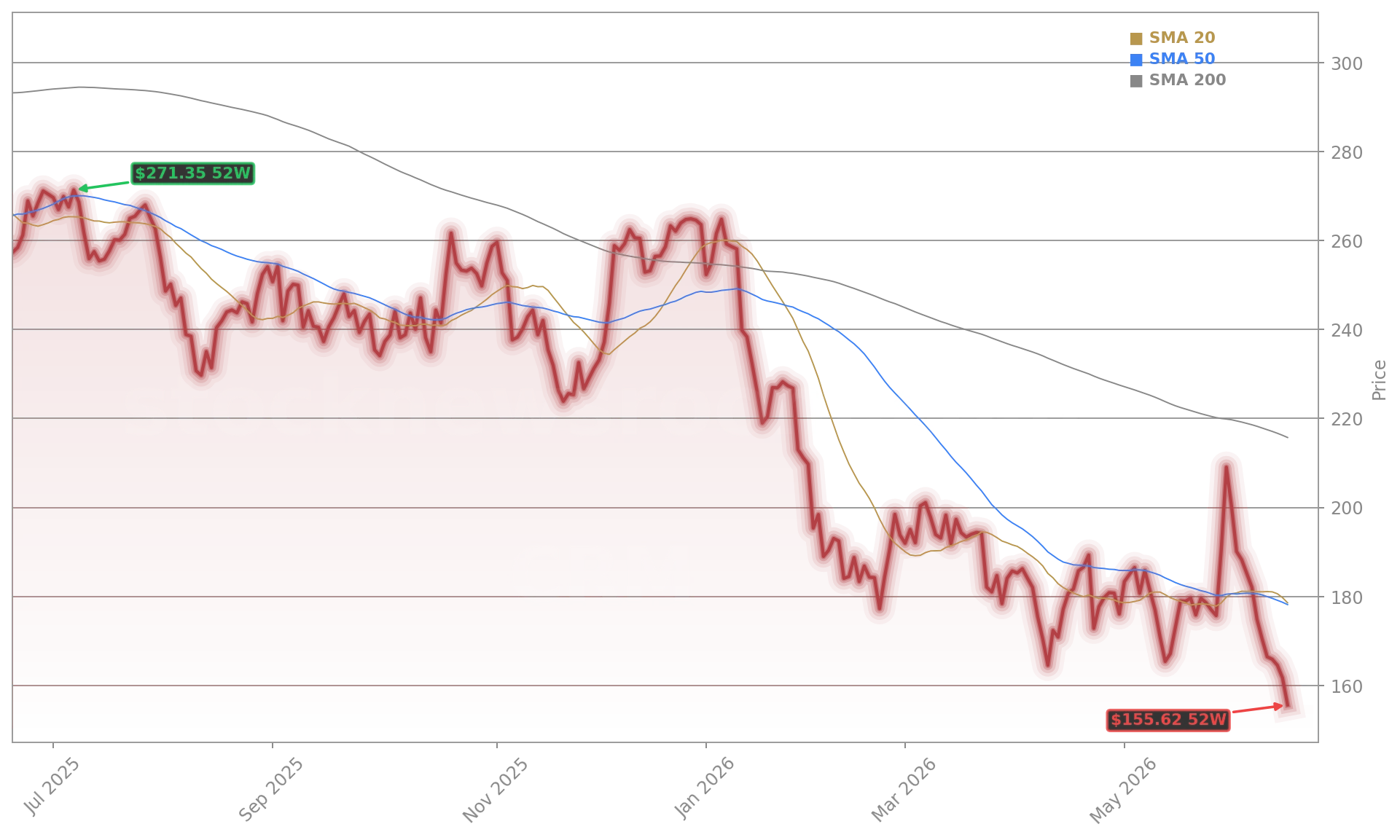

Why Is CRM Trading Near a 52-Week Low?

Despite strong Salesforce Earnings, Salesforce Inc. is down roughly 40% year to date and recently hit a fresh 52-week low. The selloff isn’t driven by fundamentals—it’s a valuation reset. Investors are pricing in long-term uncertainty around AI’s impact on enterprise software economics. The fear isn’t that AI won’t work—it’s that it will work *too well*, collapsing seat-based revenue models across the sector. That anxiety is contagious: Adobe’s AI strategy recently triggered a 5% stock plunge, and the broader software trade weighed on the Dow alongside Microsoft and Amazon.com Inc.. Salesforce’s forward P/E now sits near 12—low for a profitable, double-digit-growing tech leader—but reflects Wall Street’s demand for patience, not panic.

How Does Salesforce Compare to Peers on Margins and Cash Flow?

Salesforce Inc. outperformed peers on capital efficiency in Q1. Its non-GAAP operating margin hit a record 34.8%, surpassing both NVIDIA’s 58.2% (driven by chip scarcity) and Apple’s 30.1% (Q2 FY2026), though on a very different scale. Free cash flow totaled $6.6 billion—more than double the $2.9 billion generated by Adobe in its latest quarter. Salesforce also returned $27.5 billion to shareholders, including a $25 billion accelerated share repurchase—the largest in company history—shrinking the share count by ~10%. Citigroup maintains a ‘Buy’ rating on Salesforce Inc., citing its AI monetization velocity and margin expansion as unmatched among large-cap SaaS peers. RBC Capital Markets, meanwhile, recently upgraded Salesforce Inc. to ‘Outperform’, raising its 12-month price target to $185, citing improving ARR composition and reduced execution risk.

Is the AI Overhang Temporary—or Structural?

The AI overhang on Salesforce Inc. is both cyclical and structural. Cyclical: Wall Street is rotating out of high-multiple software names amid rising Treasury yields and Fed uncertainty. Structural: If AI agents truly replace human workflows at scale, per-seat pricing models across enterprise software could erode over time. Yet Salesforce’s Q1 results suggest the transition is additive—not substitutive—so far. The $3.6 billion acquisition of Fin, an AI customer service platform, reinforces its shift toward usage-based and outcome-based pricing. Still, management acknowledged ongoing softness in Commerce Cloud and Tableau—two segments where AI integration lags. That uneven progress means investors must weigh near-term execution against long-term platform risk. For now, the data shows AI is accelerating, not undermining, Salesforce’s growth engine—but patience remains essential.

How Are Analysts Positioning Ahead of Fiscal H2?

With management guiding for organic revenue reacceleration in the back half of fiscal 2027, Wall Street is watching for two catalysts: sustained AI ARR growth above $4 billion and evidence of cross-selling Fin’s capabilities across the installed base. Morgan Stanley recently reiterated its ‘Overweight’ rating, noting Salesforce Inc.’s AI monetization pace is now outpacing both Microsoft’s Copilot rollout and Palantir’s government-focused AI deployments. Still, Goldman Sachs cautions that valuation upside remains capped until broader software sector sentiment improves—particularly as the S&P 500’s tech-weighted index trades near all-time highs while enterprise software lags. The next major test arrives with Q2 earnings in late August, where guidance for full-year AI ARR and seat growth will be closely scrutinized.

Our largest applications, sales and service, saw year-over-year seat growth with humans and agents both expanding on the platform.— Robin Washington, COO and CFO, Salesforce Inc.

Related coverage: Salesforce’s $3.6 billion acquisition of Fin was widely seen as a defensive play to lock in AI customer service leadership—but can it reverse CRM’s sharp slide? Salesforce Acquisition $3.6B Deal Meets CRM Stock Slide. Meanwhile, Adobe’s AI strategy faces mounting investor skepticism after its stock dropped 5% on similar concerns about monetization timing and execution risk—raising questions about how the entire enterprise software cohort navigates AI’s promise and peril. Adobe AI Strategy: Stock Drops 5% as AI Push Faces Doubts.