Can Salesforce Earnings keep investors patient if AI momentum is rising but revenue guidance still leaves Wall Street wanting more?

Why did Salesforce Earnings disappoint investors?

Salesforce Inc. delivered fiscal first-quarter results that looked solid on the surface. Revenue reached $11.13 billion, up 13% year over year, while adjusted earnings per share came in at $3.88, well ahead of consensus expectations cited across Wall Street coverage. Non-GAAP operating margin expanded to 34.8%, a record high, and operating cash flow hit $6.7 billion.

Yet the market reaction was muted. The main issue was guidance. Salesforce projected second-quarter revenue of $11.27 billion to $11.35 billion, a touch below expectations near $11.36 billion. Full-year guidance was raised to $45.9 billion to $46.2 billion, but even that midpoint landed slightly shy of some analyst models. That left investors asking whether strong Salesforce Earnings are being flattered by acquisitions and buybacks rather than organic acceleration.

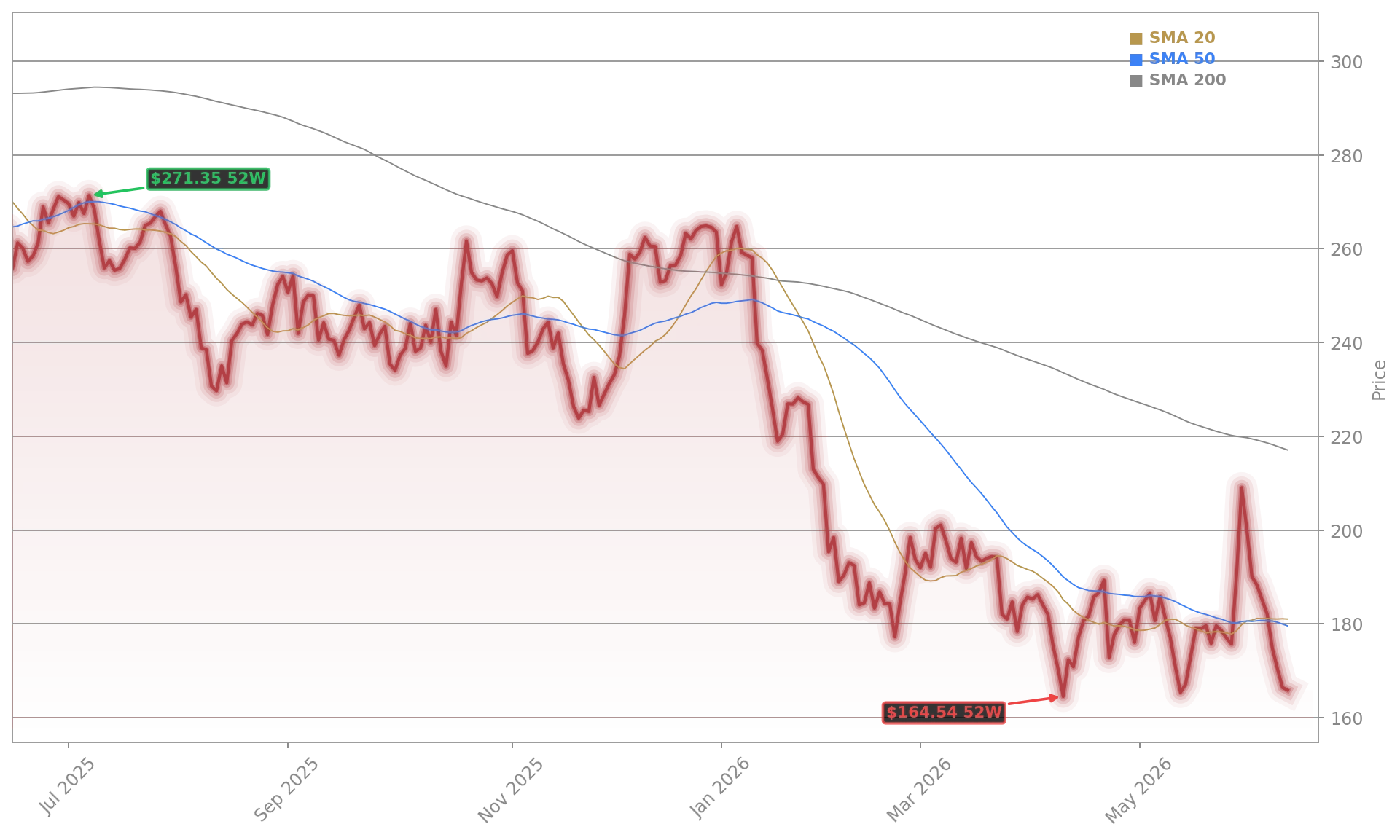

As of Thursday evening, Salesforce shares were trading at $176.17, down 0.75% from the prior close of $175.30, before edging up to $176.75 in after-hours trading.

Is Salesforce proving AI can move the needle?

The most closely watched part of the report was Agentforce, Salesforce’s AI offering. Management said Agentforce annual recurring revenue moved past $1 billion, with some reports placing the figure near $1.2 billion. That is fast growth from roughly $800 million discussed earlier this year, but it still represents only a small slice of a company generating more than $11 billion in quarterly revenue.

Salesforce also highlighted $3.4 billion in AI and data ARR, heavy token growth, rising agentic work units, and strong Slack adoption. Premium SKU bookings rose nearly 60% year over year, and Slack accounted for almost half of million-dollar-plus wins. Those metrics suggest customers are engaging with the AI stack, but investors want clearer evidence that usage is becoming material revenue growth.

That skepticism matters because rivals including Oracle, Snowflake, and SAP are also pitching enterprise AI platforms. In a market where NVIDIA remains the clearest AI winner, software names need to show not just adoption, but monetization.

What are analysts saying about Salesforce?

Analyst commentary after the report stayed mixed. Barclays cut its price target to $236 while keeping an overweight rating. Bernstein maintained a Sell rating with a $173 target, arguing AI momentum has not yet translated into enough visible growth. BMO Capital Markets set a $215 target and framed the story as more of a wait-and-see setup. KeyBanc remained more constructive with a $290 target.

Guggenheim analyst John DiFucci also stayed skeptical, pointing to disappointing new business value and organic growth estimated near 7.5%. His concern is that management’s forecast for a stronger second half may be harder to achieve if underlying bookings do not improve. That debate sits at the center of the current Salesforce Earnings narrative: strong execution on margins, but lingering doubt on demand quality.

Salesforce did try to answer part of that concern with capital returns. The company launched a $25 billion accelerated share repurchase, and buybacks had a meaningful impact on diluted share count and EPS. Marc Benioff also emphasized AI-driven productivity gains, saying hiring remains focused mainly on sales rather than engineering.

Can Salesforce rebuild confidence from here?

The bull case is straightforward. Salesforce is still growing at a double-digit pace, margins are expanding, and large enterprise deal activity remains healthy. Management says Informatica helped headline growth, while CRPO rose to $33.6 billion, up about 14%. If organic trends improve in the second half, today’s valuation could look undemanding.

The bear case is also clear. Weakness in marketing, commerce, and Tableau bookings shows softness in parts of the portfolio. Investors also worry that AI could compress parts of traditional software rather than simply expand them. That is why Salesforce Earnings drew a more cautious response than a simple beat-and-raise quarter might normally deserve.

Related Coverage: Investors looking for the broader setup around sentiment and valuation can also read this breakdown of the latest Salesforce forecast and Bank of America’s warning. That piece explores whether the recent bearish turn is a contrarian signal or a sign that Wall Street is still repricing the stock after repeated questions around growth quality and AI monetization.

Salesforce Earnings showed a company executing well operationally, but still struggling to fully win over a skeptical market. For investors, the next key test is whether AI revenue and organic bookings can accelerate enough to validate management’s second-half optimism. If that happens, Salesforce may finally shift the conversation from cautious guidance to durable growth.