Can Oracle’s massive AI spending spree turn backlog into dominance, or is Wall Street right to fear the bill?

Why Did Oracle Earnings Spark a 22% Selloff?

Despite beating top- and bottom-line expectations, Oracle Corporation’s fiscal Q4 2026 results triggered Wall Street’s sharpest one-week decline in over two decades. The culprit wasn’t weak performance — it was the scale of ambition. With cloud infrastructure revenue surging 93% YoY to $5.79 billion and multicloud AI database growth exploding 404%, investors recoiled at the $55.7 billion in fiscal 2026 capex — $23.7 billion in negative free cash flow — and the $90–95 billion FY27 capex guidance. The company’s plan to raise ~$40 billion in debt and equity amplified concerns about balance sheet strain, even as co-CEO Clay Magouyrk emphasized that capacity is ‘all already contracted for at a very profitable rate.’

How Does Oracle Earnings Compare to Hyperscaler Peers?

Oracle Corporation is now spending more on AI infrastructure than any other U.S. tech firm — outpacing even NVIDIA-enabled capex by hyperscalers like Amazon and Microsoft. While Amazon’s AWS is investing $35 billion in India alone, Oracle’s 211+ live and planned cloud regions — including 72 embedded inside Amazon, Google, and Microsoft — represent a structural multicloud bet. Its cloud revenue now comprises 52% of total revenue (up from 43% YoY), contrasting with Salesforce’s slower cloud transition and Adobe’s AI monetization focus. Meanwhile, Tesla and Apple remain largely uninvolved in hyperscale infrastructure, widening Oracle’s strategic divergence in the AI stack.

Oracle Earnings: Is the Market Pricing in Risk or Ignoring Revenue Certainty?

Oracle’s Remaining Performance Obligations hit $638 billion — up 363% YoY — with $75 billion tied to prepaid or customer-supplied GPU arrangements. That backlog dwarfs peers: Salesforce’s RPO stood at $28.4 billion in its latest quarter; Meta’s infrastructure commitments remain opaque. Yet the market’s reaction suggests skepticism about execution risk and capital discipline. Morningstar trimmed its fair value estimate to $207 from $220, citing capex overhang. But BofA analyst Tal Liani reiterated a Buy rating and $240 price target, while Goldman Sachs analyst Gabriela Borges raised her forecast to $239 — noting that net cash outlay is closer to $70 billion after prepayments and bring-your-own-cloud deals.

What Do Analysts Say About Oracle’s AI Financing Plan?

RBC Capital Markets maintains a Hold rating on Oracle Corporation with a $190 price target — the lowest among major banks — citing leverage concerns. Oppenheimer’s Brian Schwartz, however, reiterated a Buy with a $275 target, calling Oracle ‘the most underappreciated AI infrastructure play.’ Cantor Fitzgerald and Seeking Alpha contributors echo that view, upgrading Oracle to Strong Buy on the basis of RPO visibility and margin resilience. Notably, the $0.50 quarterly dividend — declared June 10 and payable July 24 — adds income appeal rare among high-growth cloud builders, reinforcing its appeal for retirement portfolios amid rising rate uncertainty.

Where Is Oracle Stock Headed Next?

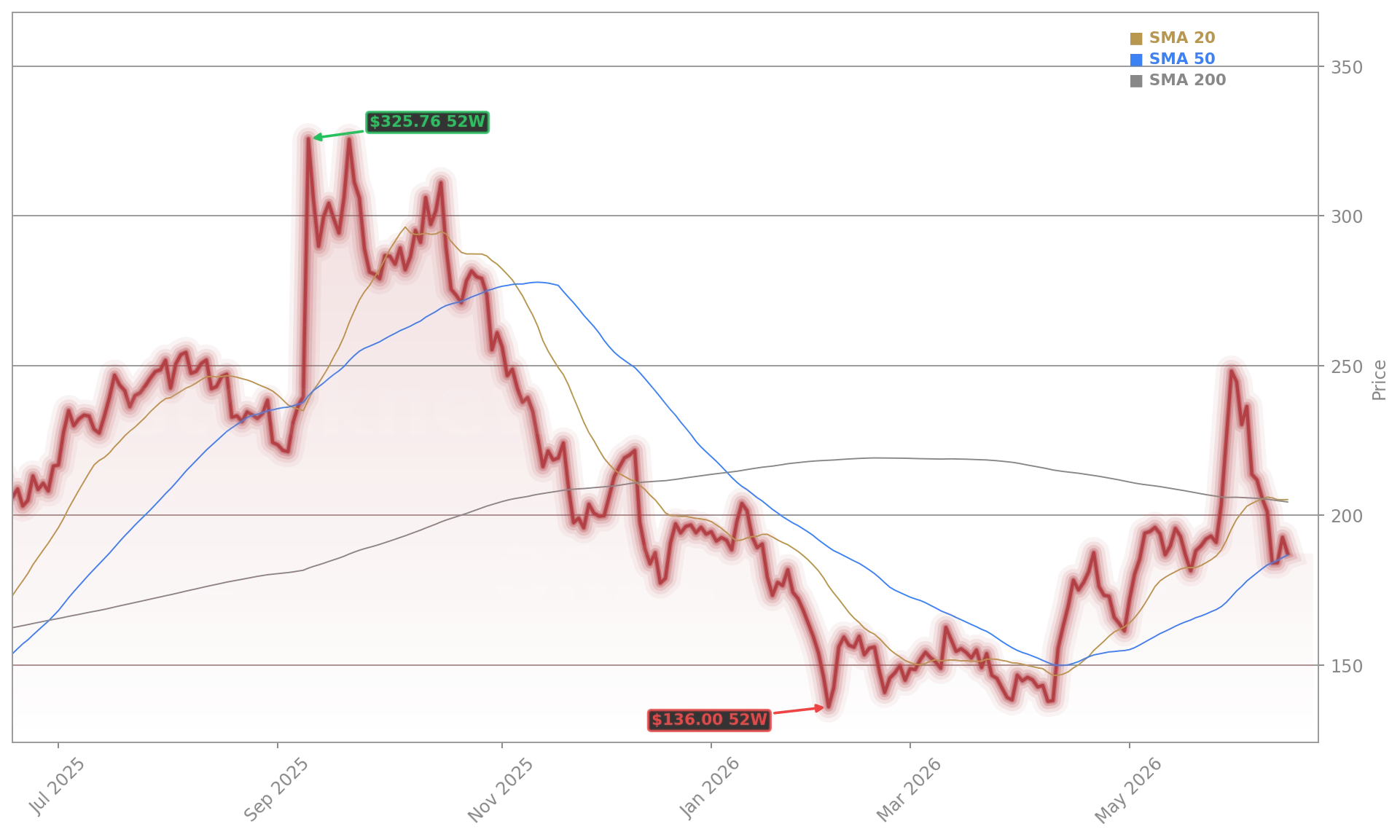

At $192.86, Oracle trades 5.8% below its 200-day SMA — a bearish technical signal — yet 14.1% above its 100-day SMA, suggesting short-term momentum is reasserting. Key resistance sits at $200.50, just below the 20-day/200-day SMA convergence zone. Downside support holds at $179.00, a prior buyer-defense level. With Q1 FY27 cloud revenue guided at 58%–64% growth and FY27 EPS raised to $8.05 (+18%), the disconnect between forward estimates and current valuation is widening. For investors, this isn’t a binary ‘buy or sell’ — it’s a test of whether AI infrastructure monetization justifies near-term cash burn.

Related Coverage: Oracle’s $638 billion AI backlog and debt financing strategy are under fresh scrutiny in Oracle Earnings Show $638B Backlog as Debt Fears Rise. Meanwhile, the broader AI valuation debate intensifies as Palantir’s 63x multiple faces pressure in Palantir Valuation at 63x Faces Warning After SpaceX IPO.

Capacity is all already contracted for at a very profitable rate.— Clay Magouyrk, co-CEO of Oracle Corporation

Oracle Earnings underscore a pivotal shift: AI growth is no longer about software margins alone — it’s about infrastructure scale, capital discipline, and balance sheet resilience. For U.S. portfolios, Oracle remains a high-conviction, high-stakes AI infrastructure proxy. The next quarterly earnings will reveal whether execution matches the ambition — and whether Wall Street’s patience holds.