Did Oracle just hit a costly wall in its AI expansion after a $3 billion cloud deal reportedly fell apart?

Why did the Oracle Cloud Deal fail?

According to people familiar with the matter reported by Business Insider, Microsoft explored leasing capacity on Oracle Cloud Infrastructure (OCI) to offload select Azure workloads — a move aimed at easing pressure on its own AI compute pipeline. The deal, valued at over $3 billion, would have marked one of the largest inter-cloud capacity-sharing agreements in history. But negotiations stalled when Oracle declined to pursue FedRAMP authorization for its public cloud platform, citing the engineering burden and timeline. While Oracle’s government cloud already meets FedRAMP standards, extending it to OCI would require significant architectural rework — a hurdle the company was unwilling to clear for this deal. Oracle issued a terse denial, calling the report’s details ‘inaccurate’ while reaffirming its ‘tremendously collaborative’ partnership with Microsoft.

What does this mean for Oracle’s AI infrastructure push?

Oracle Corporation is building at breakneck speed: capex surged to $48 billion in fiscal 2026 and is projected to hit $70 billion in 2027 — with $20–25 billion expected from customer prepayments. Its $638 billion RPO reflects massive underlying demand, particularly from AI-native firms and hyperscalers. Yet the Oracle Cloud Deal collapse exposes a strategic vulnerability: OCI’s enterprise and government adoption remains constrained by compliance gaps. Piper Sandler analysts reaffirmed their ‘Overweight’ rating on Oracle Corporation, calling it ‘the top second-half idea’ despite debt concerns — but emphasized that ‘execution on FedRAMP and broader certification timelines will be a key catalyst watch.’ Meanwhile, Goldman Sachs analysts note that ‘agentic AI token consumption could rise 24x by 2028,’ intensifying pressure on all cloud providers to secure certified, scalable capacity — not just raw watts.

How is Wall Street reacting to the Oracle Cloud Deal fallout?

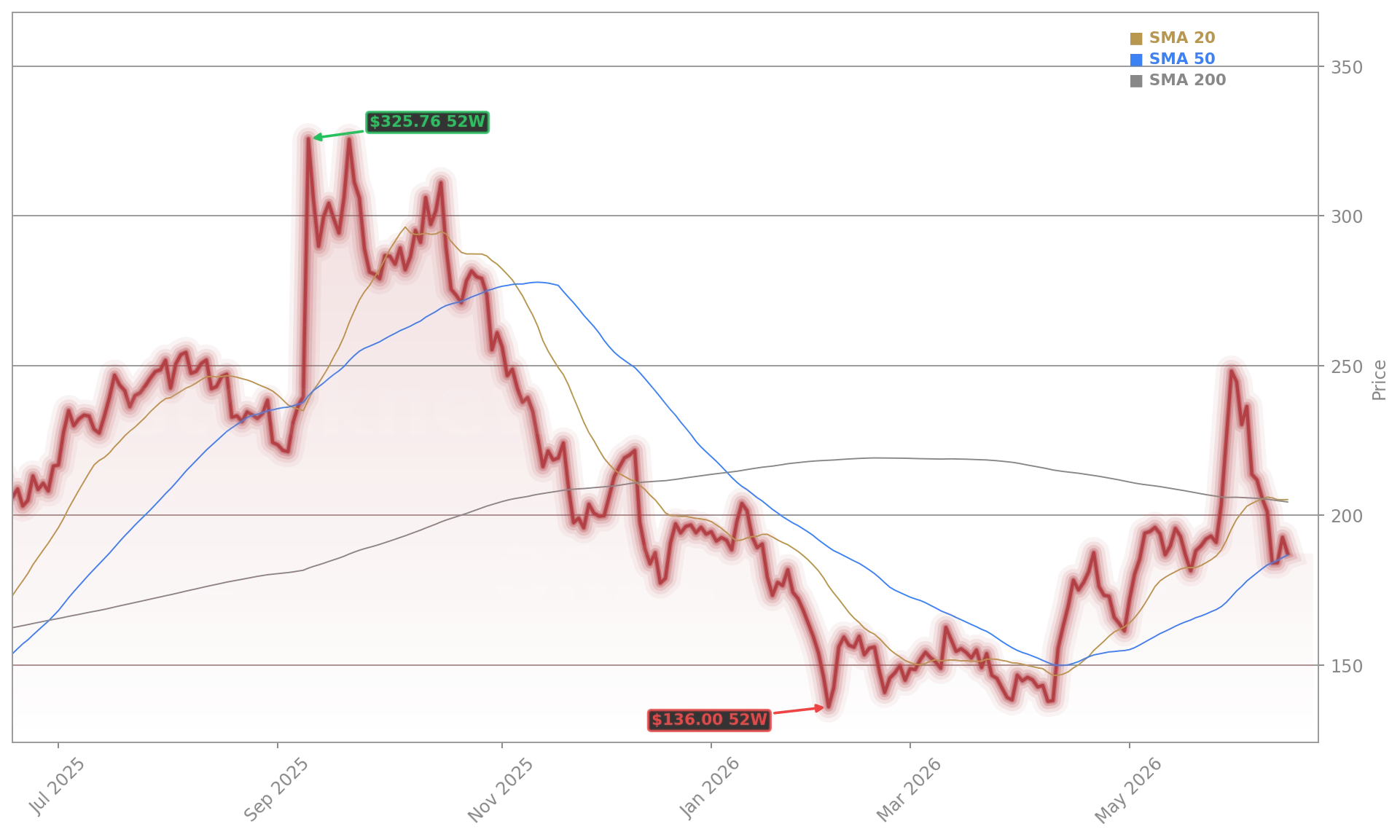

Oracle’s shares have dropped 8.59% over the past 52 weeks — underperforming the Nasdaq Composite’s 37% gain — and fell sharply again after the news. The Columbia Global Technology Growth Fund noted in its Q1 2026 letter that Oracle’s stock declined ~25% during the quarter as investors ‘digested the scale and financial intensity’ of its AI infrastructure ambitions. The fund cited ‘increasingly complex financing relationships and customer concentration’ — particularly OpenAI’s outsized role in Oracle’s forward commitments — as key concerns. Still, RBC Capital Markets maintains its ‘Outperform’ rating, citing Oracle’s ‘unmatched database-to-AI stack integration’ and ‘first-mover advantage in sovereign cloud deployments.’ With $120 billion in debt already on its balance sheet, Oracle’s next $40 billion financing round — split between debt and equity — will be closely watched by credit analysts and equity investors alike.

Where does Oracle stand versus cloud rivals?

Unlike Microsoft, which controls Azure’s full stack and compliance roadmap, or Amazon (via AWS), which holds broad FedRAMP High authorization, Oracle’s public cloud lags in federal and regulated-sector trust signals. NVIDIA and Tesla are not cloud players, but their AI hardware and edge infrastructure investments underscore the broader ecosystem race for certified, secure AI compute — a race where compliance is now a feature, not a footnote. Microsoft’s ‘shopping for capacity everywhere’ strategy reflects a new reality: cloud providers are no longer just competing for end users — they’re bidding for each other’s capacity. That dynamic benefits infrastructure enablers like Broadcom and ASML, but pressures pure-play cloud builders without regulatory agility. Oracle’s $90 billion capex plan may deliver scale — but without FedRAMP, its OCI growth ceiling remains lower than peers.

What’s next for Oracle’s cloud ambitions?

We are shopping for capacity everywhere.— Microsoft source, Business Insider

Oracle Corporation has signaled it will prioritize sovereign cloud and industry-specific certifications — including HIPAA, GDPR, and PCI — over broad FedRAMP expansion for now. Yet with U.S. federal AI procurement accelerating, that calculus may shift. The company expects to convert $77 billion of its RPO into revenue within the next 12 months, but revenue acceleration hinges on infrastructure monetization — not just buildout. Analysts at Citigroup recently raised Oracle’s price target to $210, citing ‘improving visibility into RPO conversion’ and ‘strong traction in financial services and healthcare verticals.’ Still, the Oracle Cloud Deal impasse serves as a stark reminder: in the AI infrastructure arms race, capital and compute matter — but compliance is the gatekeeper.