Can Palantir Valuation still justify its premium now that SpaceX has seized the market’s mega-tech multiple spotlight?

Why Did Palantir Valuation Drop From #1?

SpaceX’s June 12 Nasdaq debut reset the valuation ceiling for private-to-public tech transitions. Priced at $135 and surging to $178 by Monday’s close, SpaceX now trades at a staggering 110x trailing price-to-sales — nearly double Palantir’s 63x multiple. For context, the S&P 500 trades at 3.5x, and even NVIDIA — the AI infrastructure leader — trades at just 20x. This shift isn’t academic: it forces portfolio managers to justify holding PLTR at a premium when a rival with comparable growth narratives, deeper government ties, and higher near-term revenue visibility commands a steeper multiple. Palantir’s valuation no longer stands alone as the outlier — it’s now the benchmark SpaceX has surpassed.

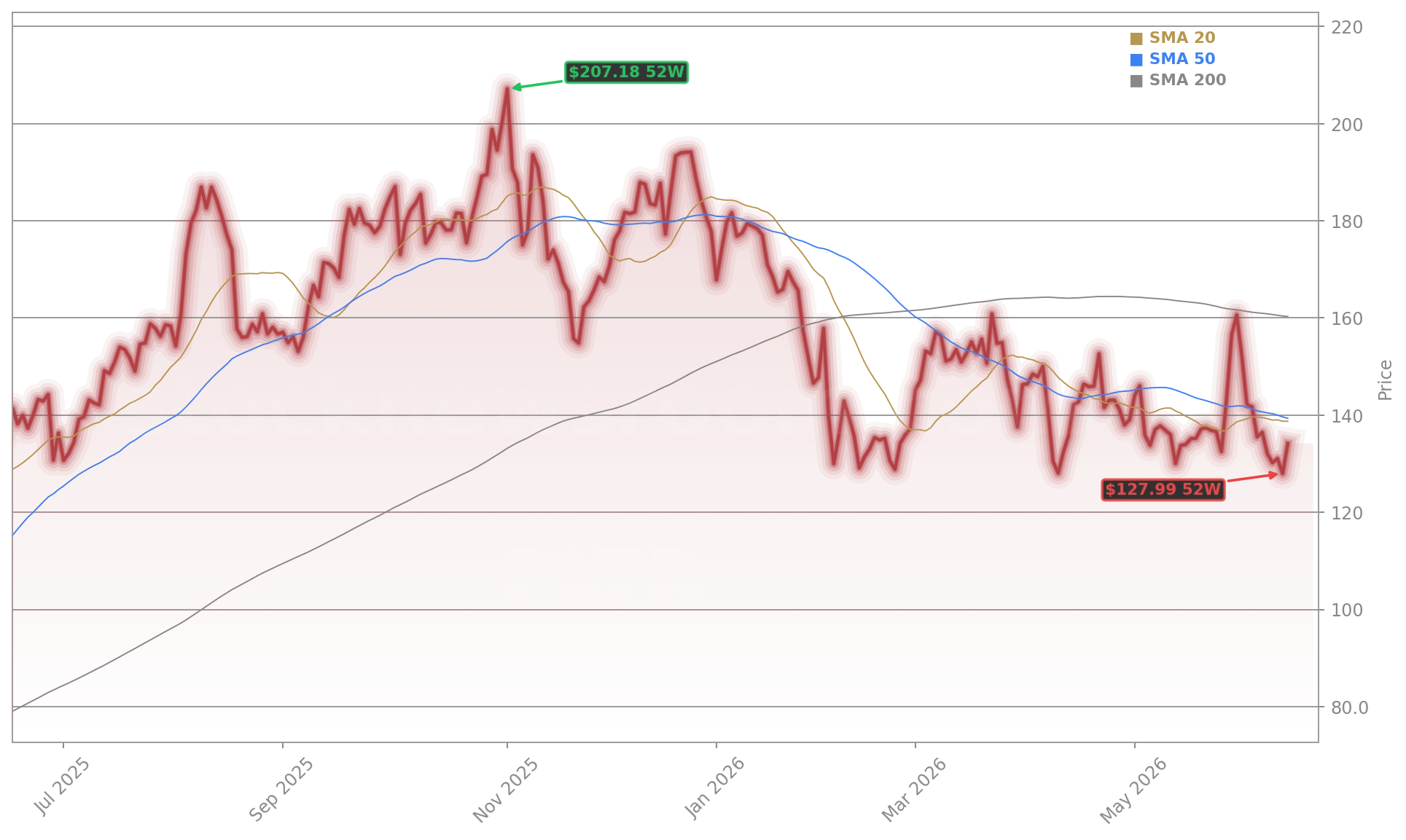

How Is Palantir Valuation Holding Up in Q2?

Despite the relative valuation compression, Palantir Technologies Inc. delivered resilient Q2 2026 results: revenue rose 28% year-over-year to $712 million, beating consensus by $17 million, while GAAP net income hit $119 million — its third consecutive profitable quarter. Gross margin expanded to 81%, and government revenue grew 34%, underscoring stickiness in its core defense and intelligence verticals. Still, the market’s muted reaction — PLTR dipped 0.62% in regular trading before rebounding after hours — signals that growth alone no longer commands automatic multiple expansion. Citigroup maintained its ‘Neutral’ rating but lowered its 12-month price target to $130, citing ‘valuation saturation relative to near-term execution risk.’ Meanwhile, RBC Capital Markets upgraded Palantir Technologies Inc. to ‘Outperform,’ highlighting its AI platform’s accelerating adoption at Fortune 500 firms and federal agencies.

What Do Competitors Reveal About Palantir Valuation?

Comparisons reinforce the pressure. Tesla trades at 6.7x sales, Apple at 3.2x, and Salesforce — fresh off its $3.6 billion AI-focused acquisition — trades at 7.1x. Even AI-native firms like C3.ai (AI) hover near 12x. Palantir’s 63x multiple is an order of magnitude higher — and it’s now being challenged not just by fundamentals, but by narrative velocity. SpaceX’s Starlink revenue is already $5.2 billion annualized, with government contracts expanding rapidly, while Palantir’s commercial AI monetization remains in early innings. As one Morgan Stanley analyst noted in a June 14 note, ‘The market is no longer paying for potential alone — it’s pricing for near-term revenue scalability, and SpaceX just demonstrated it at scale.’

Is Palantir Valuation Sustainable Amid Political Headwinds?

Yes — but only if execution remains flawless. A recent Swiss investigative report by Republik raised concerns over data governance in Palantir’s European contracts — though no material financial impact has been reported. More materially, U.S. Senate hearings on AI procurement oversight could delay or reshape future defense contracts. Yet Palantir Technologies Inc. continues to win major renewals: the U.S. Army’s $2.1 billion Palantir Gotham extension and a new $480 million deal with the Department of Veterans Affairs signal strong institutional trust. Still, valuation sustainability hinges on translating that trust into consistent commercial AI revenue — not just government wins. Goldman Sachs recently emphasized that ‘Palantir Valuation hinges on the next 12 months of commercial AI monetization — not the last three years of government growth.’

Where Is Palantir Valuation Heading Next?

Short-term, technical support remains firm near $120 — a level analysts at J.P. Morgan cite as ‘a high-probability accumulation zone’ given strong insider buying and options flow. Longer term, the valuation path depends on Q3 commercial AI revenue acceleration and clarity around the U.S. AI Executive Order implementation timeline. With SpaceX now setting the bar at 110x, Palantir Technologies Inc. must prove its AI platform delivers measurable ROI across healthcare, finance, and logistics — not just defense. As RBC Capital Markets stated, ‘This isn’t about defending the multiple — it’s about earning the next one.’

Related coverage: For deeper insight into how political scrutiny is testing Palantir’s AI growth engine, read Palantir AI Strategy -2.2%: Growth Meets Political Risk. Meanwhile, Salesforce Acquisition $3.6B Deal Tests Its AI Strategy offers a parallel lens on how enterprise software peers are monetizing AI amid similar valuation pressures.

This isn’t about defending the multiple — it’s about earning the next one.— RBC Capital Markets

Palantir Valuation remains a critical litmus test for AI monetization credibility on Wall Street. For investors, the takeaway is clear: strong fundamentals alone won’t sustain premium multiples — consistent, scalable commercial AI revenue will. The next quarterly earnings will show whether Palantir Technologies Inc. is delivering that inflection. For aggressive growth portfolios, the current dip presents a tactical entry — provided the AI execution narrative remains intact.