Can Palantir’s annual meeting calm ethical concerns and valuation fears, or is the latest sell-off a warning investors should not ignore?

Why does the Palantir Annual Meeting matter?

Palantir Technologies Inc. heads into the Palantir Annual Meeting with two shareholder proposals that seek independent reviews of whether its software could contribute to human-rights abuses through government clients, including immigration enforcement, policing, and military use. The resolutions were backed by religious investors, with support also disclosed by Norges Bank and New York City pension funds. Even so, the votes are widely expected to fail because Palantir’s dual-class structure gives insiders led by Alex Karp, Stephen Cohen, and Peter Thiel nearly half of total voting power.

Palantir’s board urged shareholders to reject both proposals, arguing they are based on misunderstandings about how the company’s platforms are used. The company says customers own the data and Palantir provides software to integrate and analyze it. Still, the vote highlights a broader pressure point for a business deeply tied to US defense and public-sector work, at a moment when political and ethical scrutiny is becoming part of the investment case.

Can Palantir defend its premium?

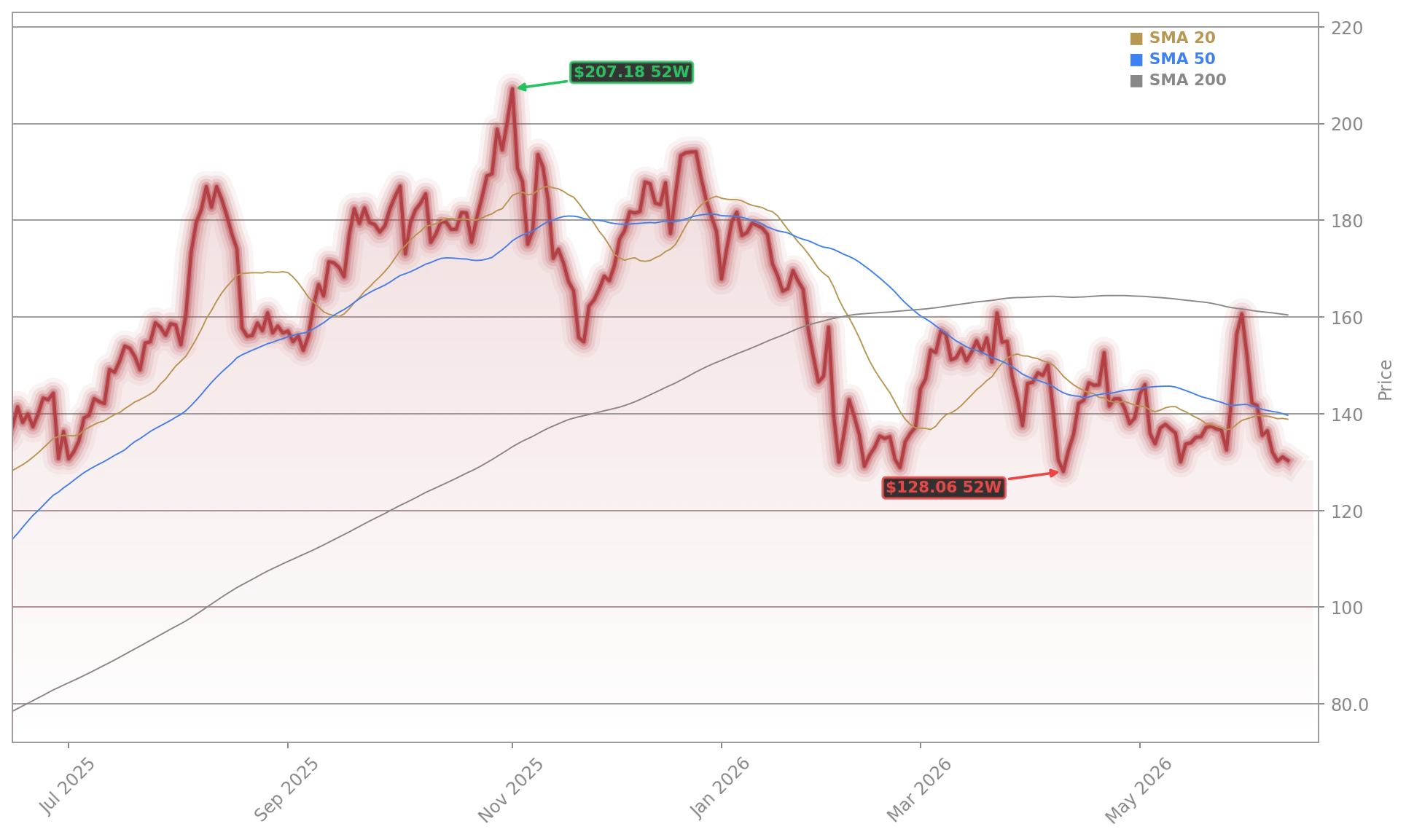

That is the second issue hanging over the Palantir Annual Meeting. The stock has pulled back hard from its 52-week high of $207.52, and today’s drop underscores how sensitive PLTR remains to any shift in sentiment. Bulls can point to exceptional Q1 2026 execution: revenue of $1.633 billion, 85% year-over-year growth, US commercial revenue up 133%, adjusted free cash flow of $925 million, and raised full-year guidance to roughly $7.656 billion.

But the bear case is just as visible. Multiple valuation frameworks still imply that Palantir is priced for near-perfect execution over years, with forward earnings multiples around 100-plus and a free cash flow yield below 1%. Seeking Alpha argued this week that Palantir’s market value would require unprecedented federal market share and commercial scale. TradingKey also pointed to insider selling, regulatory scrutiny, and technical weakness as factors behind today’s decline.

Recent insider activity has added to that debate. Investing.com reported that director Lauren Friedman sold more than $500,000 of stock under a Rule 10b5-1 plan, while separate filings showed other senior leaders also sold shares in May. For investors, planned sales do not automatically signal trouble, but they do matter more when a stock already trades at a premium.

How does Palantir compare with AI peers?

Palantir still occupies a distinct spot between enterprise AI software and defense technology, which helps explain why it often trades differently from NVIDIA, Microsoft, or ServiceNow. Unlike chipmakers, Palantir is selling data integration, operational decision tools, and AI deployment through Gotham, Foundry, and AIP. That positioning has also made it a beneficiary of investor interest in sovereign AI, defense modernization, and data-layer infrastructure.

On Wall Street, the rating picture remains mixed rather than uniformly bearish. Some firms have turned more constructive on software and AI infrastructure names broadly, while valuation-focused investors remain cautious on PLTR specifically. The analyst average price target cited in recent coverage sits near $183.73, but dispersion is wide, reflecting the market’s split between momentum believers and valuation skeptics. For comparison, richly valued AI leaders such as NVIDIA and Tesla also face premium debates, but Palantir’s government exposure adds an extra layer of policy risk.

Related Coverage: Investors tracking today’s selloff may also want to read this analysis of Palantir’s valuation warning and premium pressure. That piece focuses on whether explosive AI growth can keep supporting the stock’s elevated multiple. It also complements the Palantir Annual Meeting story by explaining why even strong execution may not fully shield shares from multiple compression.

We are interested in increased transparency and accountability and would like to see Palantir transparently acknowledge, mitigate, and otherwise address the human rights harms it is connected to.— Aaron Acosta

The Palantir Annual Meeting shows that PLTR remains a high-conviction but high-friction stock. For investors, the next key test is whether revenue growth, contract momentum, and AI adoption can overpower governance concerns and valuation fatigue. If Palantir keeps delivering at its recent pace, the debate stays alive, but today’s pullback is a reminder that even elite growth stories can still reset fast.