Can Palantir’s AI momentum overpower valuation fears, or is this rebound already running into Wall Street’s favorite buzzkill?

What’s Driving the Palantir Rebound?

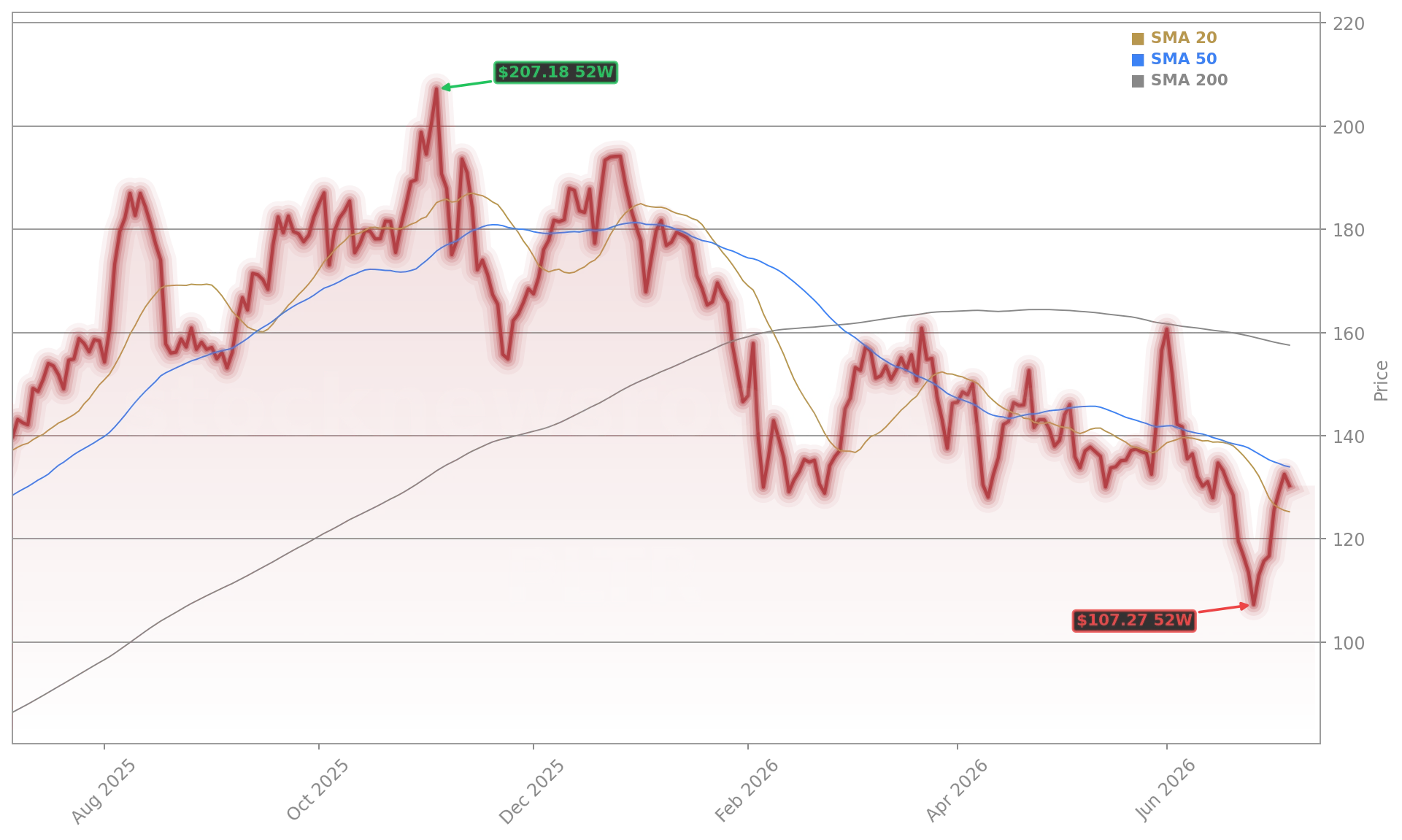

The Palantir Rebound isn’t just technical — it’s fundamentally anchored. On July 7, Palantir Technologies Inc. jumped 3.52%, fueled by two concrete catalysts: an expanded AI partnership with Mexican insurer GNP Seguros and the integration of NVIDIA’s Nemotron AI models into its AIP platform. These developments reinforce Palantir’s unique positioning — not as a model developer like OpenAI, but as the trusted enterprise layer that bridges frontier AI with sensitive government and commercial data. With 85% year-over-year revenue growth in its most recent quarter and a 53% net income margin, Palantir Technologies Inc. is proving profitability isn’t optional in AI software. That’s a stark contrast to many unprofitable AI pure-plays now facing Wall Street scrutiny.

How Does Palantir Stack Up Against AI Peers?

Compared to giants like Meta and Apple, Palantir Technologies Inc. operates in a far narrower — but higher-margin — niche: mission-critical AI orchestration for defense and regulated industries. While NVIDIA powers the chips and Microsoft embeds AI via Copilot, Palantir builds the secure, auditable workflows that federal agencies and Fortune 500 firms require. That differentiation matters. DA Davidson recently upgraded Palantir Technologies Inc. to ‘Buy’ and raised its price target to $175 — citing attractive valuation relative to growth. Yet Citigroup analysts caution that Palantir’s forward P/E of nearly 90 remains dramatically elevated versus the S&P 500 tech sector median of 28. For context, even high-flying software peers like Salesforce trade closer to 35x forward earnings.

Is the Valuation Debate Holding Back the Rally?

Yes — and it’s the central tension behind today’s price action. Palantir Technologies Inc. trades at nearly 90 times forward earnings, meaning the market expects explosive, sustained growth to justify the premium. Wall Street forecasts 45% revenue growth for 2027 — strong, but not enough to rapidly compress that multiple. Meanwhile, insider activity adds nuance: CTO Sankar Shyam sold $24.05 million in Class A shares on July 2 under a pre-arranged plan — a routine transaction, but one that reminds investors Palantir remains early-stage in its earnings scaling. The valuation debate isn’t academic: it directly impacts portfolio allocation decisions for U.S. investors seeking AI exposure without overpaying for hype.

Where Does the Palantir Rebound Go From Here?

The near-term path hinges on two catalysts: Q3 2026 earnings clarity and sovereign contract renewals. Palantir Technologies Inc. has over 832 customers — a tiny fraction of the global enterprise and defense market — suggesting massive runway. Yet execution risk remains. Competitors like BigBear.ai and newer defense-AI entrants are gaining traction, and Microsoft’s new 6,000-person AI deployment team signals intensifying competition in enterprise AI integration. Still, Palantir’s Rule of 40 score — combining growth and profitability — remains among the strongest in software. RBC Capital Markets notes Palantir’s defense tech leadership provides structural resilience absent in consumer-AI plays. For investors, the Palantir Rebound is less about timing the top and more about assessing whether its unique moat justifies patience through valuation normalization.

Related Coverage: For deeper analysis of Palantir’s cash flow surge and valuation case, see Palantir Upgrade: Buy Call After 57% Cash Flow Surge. Investors also increasingly compare Palantir’s government-AI model to defense contractors like Lockheed Martin — a dynamic explored in our recent feature on Lockheed Martin’s AI integration roadmap. And for context on how Palantir’s commercial expansion compares to enterprise software peers, read our analysis of Salesforce’s AI strategy and Q2 execution.

Palantir is the trusted layer that lets enterprises and governments deploy AI without compromising data sovereignty or security.— Alex Karp, CEO of Palantir Technologies Inc.

Palantir Technologies Inc. remains a defining AI infrastructure stock — not because it builds models, but because it secures them. The Palantir Rebound confirms demand, but the real test is whether earnings growth can meet Wall Street’s lofty expectations. For U.S. portfolios, this isn’t just a stock pick — it’s a bet on the architecture of trusted AI. The next quarterly earnings will show whether the trend continues.