Can Palantir’s latest upgrade and surging cash flow finally convince investors its premium AI valuation is more than hype?

What Does the Palantir Upgrade Mean for Wall Street?

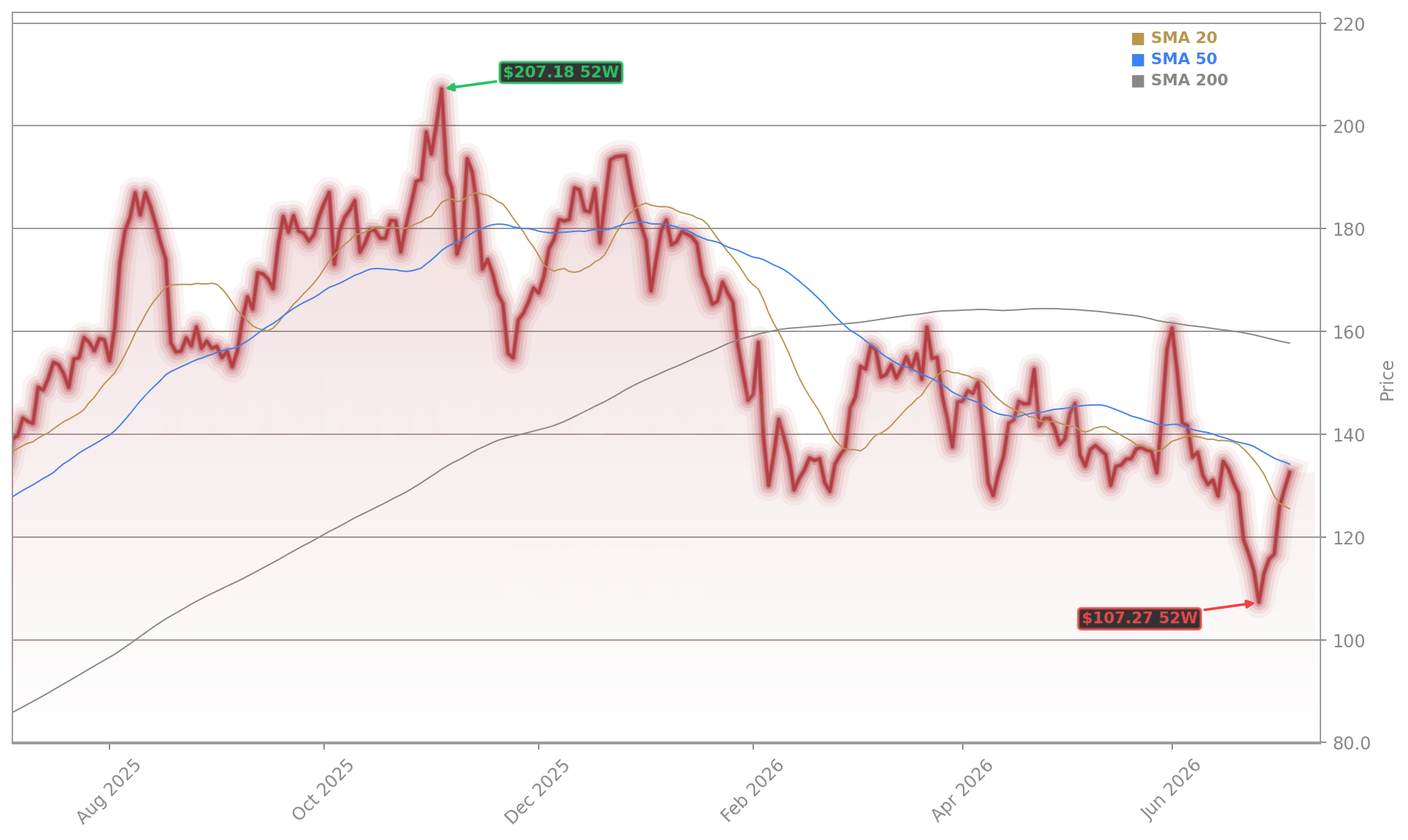

DA Davidson’s Palantir Upgrade marks a pivotal shift in institutional sentiment—especially amid a 27% year-to-date decline and a 38% drop from its October 2025 all-time high. The firm upgraded Palantir Technologies Inc. from Neutral to Buy, citing accelerating cash flow (up 57% YoY in Q1 2026), robust inbound demand for its Artificial Intelligence Platform (AIP), and a newly announced ‘sovereign AI’ partnership with NVIDIA. Unlike pure-play AI infrastructure stocks, Palantir’s value proposition centers on workflow orchestration—enabling enterprises to swap AI models, unify siloed data, and embed custom agents into operational systems. That differentiation, DA Davidson argues, justifies a 50x forward cash flow multiple—comparable to Snowflake, Datadog, and CrowdStrike, yet with twice their growth rate.

How Does Palantir Compare to NVIDIA and Other AI Leaders?

While NVIDIA posted $81.6 billion in Q1 2026 revenue—up 85% YoY—Palantir Technologies Inc. generated $1.6 billion on the same basis, also up 85%. The contrast reveals divergent paths: NVIDIA’s growth remains hardware-led and infrastructure-scale, while Palantir’s is software-led and workflow-deep. Crucially, Palantir’s adjusted free cash flow rose 57% YoY, and EPS quadrupled—despite its $4.48 billion annual revenue base. Its forward P/E of 88 remains steep versus NVIDIA’s 22, but DA Davidson notes Palantir’s recurring revenue growth guidance of 50%–70% over the next three years could compress that multiple sharply. Meanwhile, Apple and Tesla continue to lag in AI platform integration, underscoring Palantir’s niche as a neutral, platform-agnostic enabler.

Why Are Institutions Buying Palantir Now?

Institutional positioning confirms momentum: Palantir Technologies Inc. ranks as the third-largest holding (7.26%) in the First Trust Indxx Aerospace & Defense ETF—behind only GE Aerospace and The Boeing Company. That exposure reflects growing defense and federal AI adoption, accelerated by the new sovereign AI initiative with NVIDIA targeting federal agencies. Additionally, Palantir’s ‘bootcamp’ deployment model—where engineers co-build workflows with client teams—drives high retention and expansion: 89% of commercial customers increased spend in Q1. Its AIP is now embedded in critical operations at Surf Air Mobility (SRFM), powering its SurfOS aviation platform, and at major defense contractors—evidence of sticky, ROI-driven adoption, not token-based AI spending.

Is Palantir’s Valuation Justified—or a Risk?

Palantir may be the best software company—cash flow is doubling this year while the stock has fallen by about a third. It now trades at 50x cash flow, similar to Snowflake, Datadog, CrowdStrike, and Shopify, but growing twice as fast.— DA Davidson analyst

Yes—and no. With a price-to-sales ratio of 64 and a P/E of 146, Palantir Technologies Inc. remains expensive by traditional metrics. But DA Davidson argues its valuation reflects structural advantages: proprietary professional services, deployed engineering teams, and AI model flexibility in a world of tightening export controls on Anthropic and others. The analyst’s bull case envisions 2–3x cash flow growth over three years—if the multiple holds, shares could rally significantly. Still, volatility is baked in: AI data point releases and geopolitical shifts will likely drive near-term swings. For S&P 500 and NASDAQ investors, Palantir’s role as an AI ‘integrator’ rather than a ‘vendor’ offers diversification against pure hardware or model risks.