Is the Palantir Rebound just an oversold bounce, or the first sign that institutional money is rotating back into AI software?

What Triggered the Palantir Rebound?

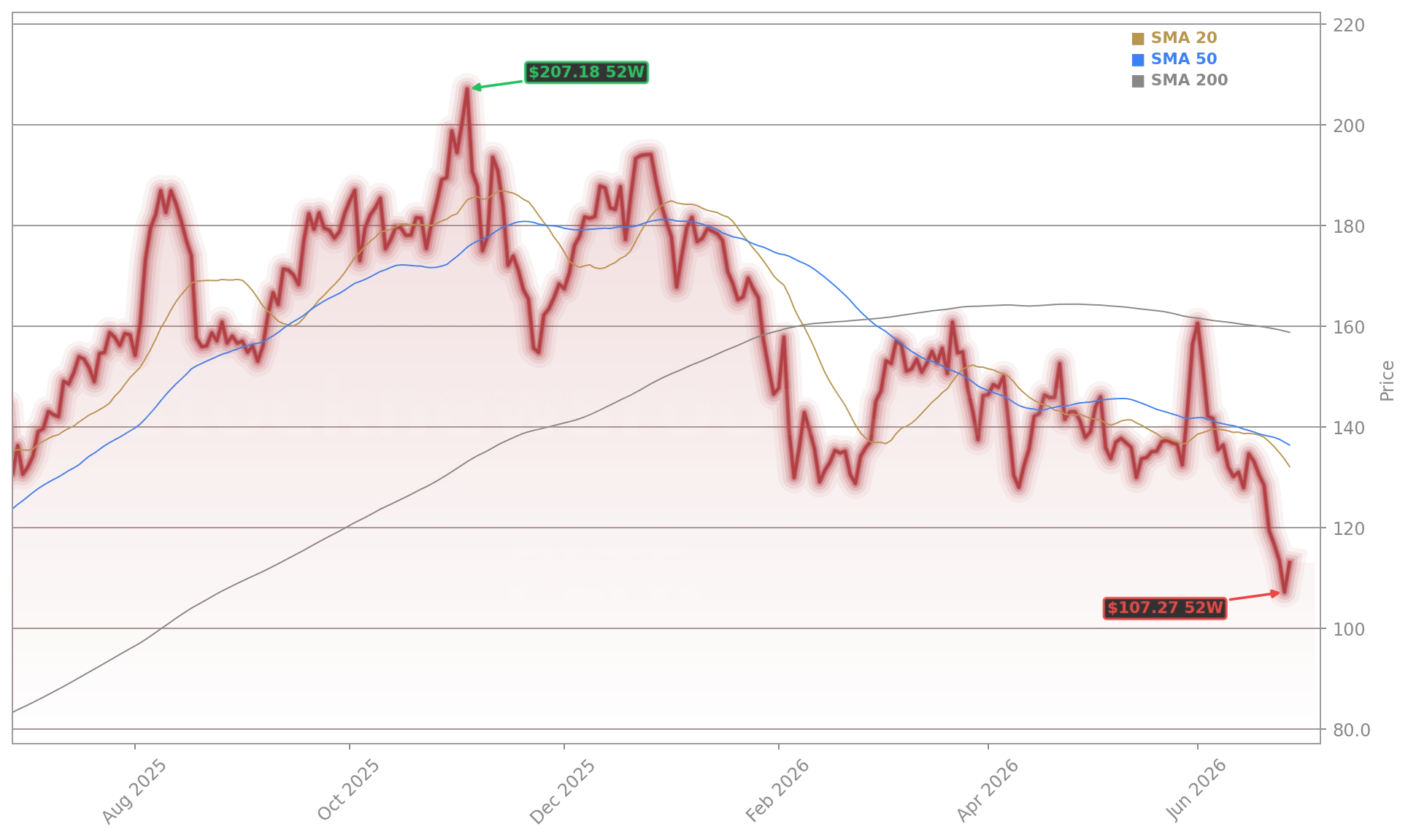

Friday’s 4.76% surge — lifting Palantir Technologies Inc. to $112.64 — was catalyzed by three converging forces: technical exhaustion, institutional conviction, and sector rotation. The stock’s 14-day RSI plunged to 27.37 on Thursday — deep in oversold territory — prompting algorithmic and discretionary dip-buying. Simultaneously, ARK Invest disclosed purchases across three ETFs (ARKK, ARKW, ARKF), adding 30,528 shares at an average price near $107.27. Crucially, the rebound occurred while the Nasdaq Composite fell 0.2% and the S&P 500 edged flat — underscoring Palantir’s divergence from broader tech weakness. This wasn’t a market-wide lift; it was a targeted vote of confidence in AI software execution amid a broader rotation away from AI chip names like NVIDIA and toward applied AI platforms.

How Does Palantir Compare to Peers?

While Palantir Technologies Inc. fell 36% in 2026, the S&P 500 rose 7.5% and the Nasdaq Composite gained 9%. That underperformance starkly contrasts with peers: Meta is down 31%, ServiceNow 55%, and Salesforce 44% — yet Palantir’s revenue growth remains unmatched. First-quarter 2026 revenue spiked 85% year-over-year to $1.63 billion, the strongest quarterly growth since its 2020 IPO. Earnings more than quadrupled, and management raised full-year guidance to $7.65–$7.66 billion — a 63% increase over 2025. By comparison, Microsoft and Oracle reported mid-teens revenue growth. Palantir’s valuation has compressed sharply: its P/E ratio fell from over 121x to 74x forward earnings, narrowing the gap with software peers despite accelerating growth — a dynamic Citigroup highlighted in its recent $175 price target and ‘Buy’ rating.

Is the Technical Structure Supporting Recovery?

Technically, Palantir Technologies Inc. remains in a bearish longer-term posture — trading 10% below its $127 support level, 16% under its 20-day SMA ($132.06), and 30% beneath its 200-day SMA ($158.83). A Death Cross (50-day below 200-day SMA) remains intact since February. However, Friday’s rebound cleared critical near-term resistance at $110.50 and brought volume above 20-day average — a bullish confirmation signal. Key upside targets now loom at $132.06 (20-day SMA) and $142 (50% Fibonacci retracement of the May–June decline). Downside remains anchored at $106.37 — the June 25 intraday 52-week low. With IBD’s Composite Rating at 36/99 and Accumulation/Distribution Rating at ‘E’, institutional selling pressure persists — yet ARK’s move suggests a pivot may be underway.

What Do Analysts Say About the Outlook?

Wall Street remains overwhelmingly constructive. According to FactSet, Palantir Technologies Inc. carries an average Overweight rating and a $189.87 consensus price target — implying 67% upside from current levels. Of 33 firms tracked, 17 issue ‘Buy’ ratings, including Morgan Stanley, which reaffirmed its ‘Overweight’ stance citing ‘commercial AI monetization accelerating faster than expected.’ RBC Capital Markets maintains a $168 target and ‘Outperform’ rating, emphasizing government contract durability and commercial pipeline expansion in healthcare and financial services. Notably, Goldman Sachs recently raised its 2026 revenue estimate by $120 million, citing stronger-than-expected adoption of AIP (Artificial Intelligence Platform) in Fortune 500 enterprises. The $189.87 target is supported by 2027 EPS growth of 112% and a forward P/E of 48x — still premium, but justified by 70%+ revenue CAGR.

Why Is This Rebound Significant for U.S. Portfolios?

This Palantir Rebound matters because Palantir Technologies Inc. is a pure-play proxy for AI’s enterprise adoption — distinct from infrastructure plays like Tesla or hardware enablers like Apple. Its Q1 2026 results confirmed U.S. government revenue grew 42% and commercial revenue rose 102%, validating the dual-track strategy. As investors rotate from AI chips to AI software — evidenced by gains in Workday and Microsoft on Friday — Palantir stands out for its revenue scalability, 92% gross margins, and zero debt. For S&P 500 and NASDAQ investors, this Palantir Rebound signals potential stabilization in the most volatile segment of the tech rally — and may presage broader strength in high-growth software names. The Palantir Rebound also tests whether Wall Street’s ‘AI disruption’ narrative applies to enablers — or only to disruptors.

Palantir is a winner in AI, delivering actual KPIs and proving ability to be top of funnel for new clients.— Anonymous institutional investor, cited in Benzinga Pro analysis

Related Coverage: A day earlier, Palantir Plunge -4.5% as AI Valuation Fears Deepen examined how valuation concerns accelerated the selloff despite accelerating fundamentals. Meanwhile, Marvell Technology Analysis -4.3%: AI Hype Meets Valuation Risk highlighted similar pressures in semiconductor peers — reinforcing that Palantir’s rebound reflects a broader sector realignment, not isolated strength.