Can the Palantir Zeta Partnership revive the AI growth story, or are investors too focused on valuation risk?

What Does the Palantir Zeta Partnership Mean for AI Marketing?

The Palantir Zeta Partnership, unveiled Tuesday at Cannes Lions, represents a structural shift in how enterprise marketing infrastructure is built. Zeta Global will rearchitect its Data Cloud on Palantir’s Foundry platform, integrating its AI intelligence layer ‘Athena’ with Palantir’s ontology, governance, and operational infrastructure. This deep technical integration allows real-time, governed decision-making at scale — a critical differentiator for Fortune 500 marketers wary of AI hallucinations and compliance gaps. Co-Founder and CEO Alex Karp called it ‘a next generation marketing environment’ that delivers AI advantages while mitigating known risks. Zeta CEO David Steinberg projected the partnership could drive over $100 million in annual revenue for Zeta in coming years — a direct monetization path for Palantir’s commercial AI expansion.

Why Is Palantir Technologies Inc. Underperforming Its Peers?

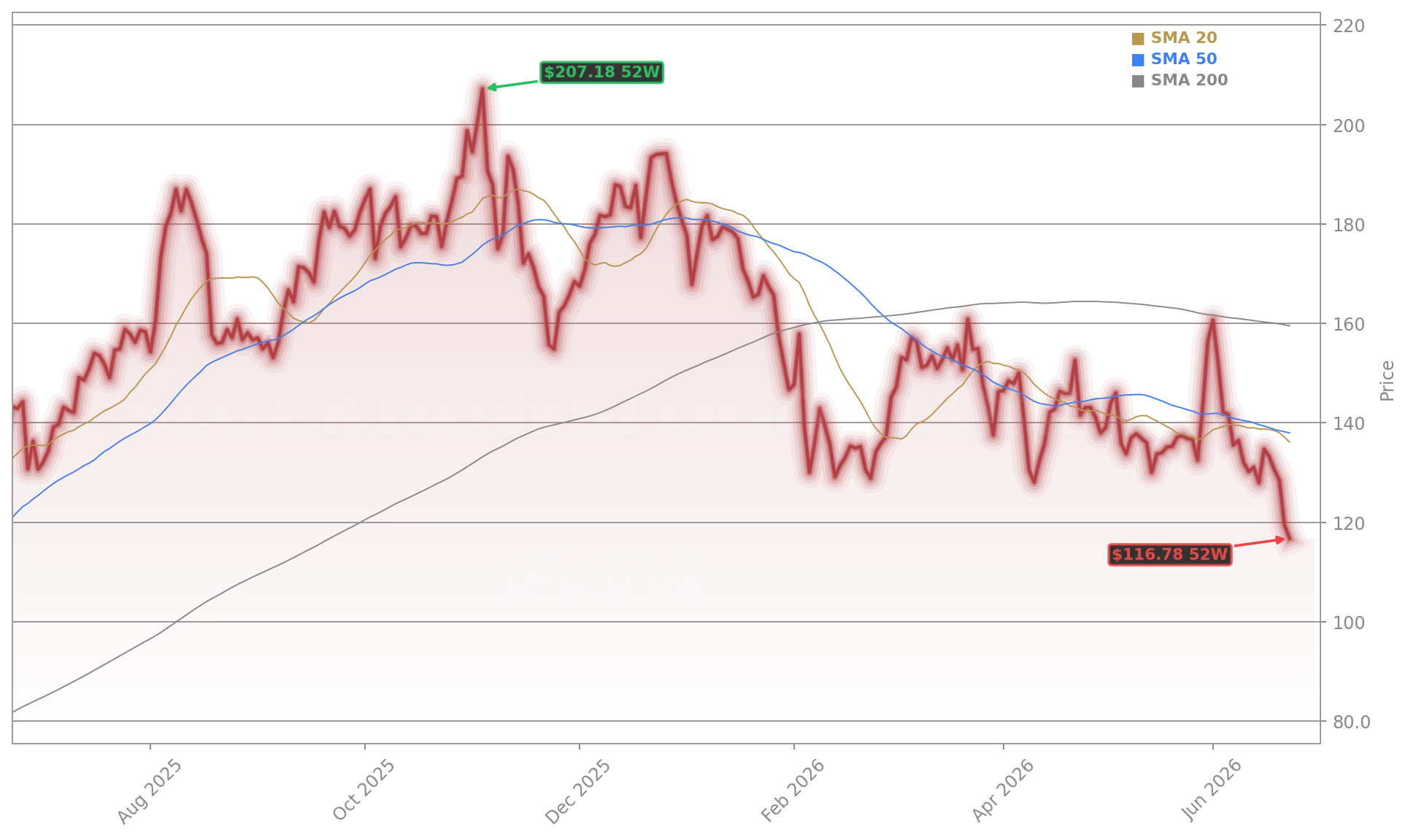

While NVIDIA and Tesla trade near 52-week highs and the S&P 500 is up 7.5% year-to-date, Palantir Technologies Inc. has plunged 34% YTD and hit $118.00 — its lowest close since June 2025. The sell-off isn’t sector-wide: software peers like Salesforce and Palo Alto are flat or modestly down. Instead, it’s company-specific — driven by valuation fatigue (trading at 89x forward P/E vs. S&P 500’s 20.9x), rising short interest, and geopolitical contract uncertainty. France’s DGSI is phasing out Palantir in favor of ChapsVision, and the UK NHS contract faces a 2027 break clause review. Meanwhile, UBS reiterated its Buy rating with a $200 price target on June 16, citing Palantir’s Ontology layer as ‘a tough nut to crack’ for rivals like Anthropic and OpenAI.

How Does the U.S. Army NGC2 Win Fit Into the Picture?

Palantir Technologies Inc. secured a foundational role in the Army’s $20 billion NGC2 common data layer — a strategic win affirming its government dominance. Yet the announcement, released after Monday’s close, failed to spark a relief rally. That disconnect highlights a key market dynamic: Palantir’s government franchise is solid, but investors now demand commercial scalability and margin sustainability. The Army win validates Palantir’s technical depth, but the Palantir Zeta Partnership targets the higher-margin, faster-growing U.S. commercial segment — where revenue jumped 133% YoY in Q1. Wolfe Research upgraded Palantir to Peer Perform from Underperform, citing ‘robust position in enterprise AI software market,’ though it declined to issue a price target due to valuation concerns.

Is the Valuation Really That Extreme?

Palantir and Zeta are using Ontology to create a next generation marketing environment, giving Zeta all the advantages of AI while protecting against many of the known dangers.— Alex Karp, Co-Founder and CEO of Palantir Technologies

Yes — and it’s the central tension. Palantir trades at 144x trailing P/E and 89x forward P/E, dwarfing peers like Apple (30x) and even AI hardware leader NVIDIA (23x forward P/E). Its Rule of 40 score of 145% and 60% adjusted operating margin are elite, yet the market appears to have priced in three years of flawless execution. With Q1 revenue at $1.63 billion (85% YoY growth) and full-year guidance raised to 71% growth, the math is clear: earnings must triple from 2027 levels to justify today’s multiple. Citigroup analysts note that ‘valuation remains the single largest overhang,’ while RBC Capital Markets maintains a ‘Sector Perform’ rating, warning that ‘any deceleration in U.S. commercial growth would materially compress the compounding equation.’