Can Palantir’s France contract uncertainty justify a sharp sell-off, or is the market finally pushing back on a premium valuation?

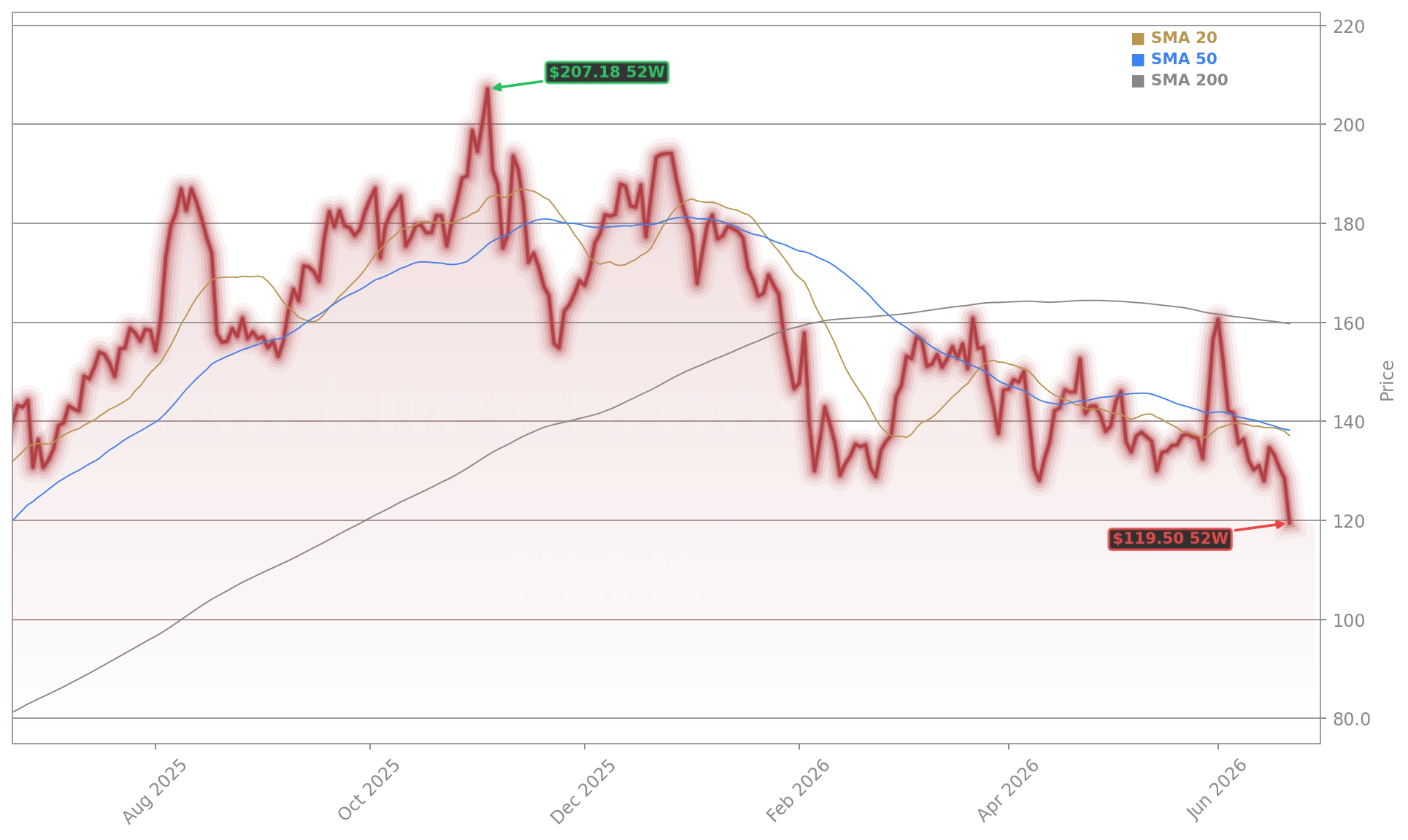

What’s Driving Palantir’s 52-Week Low?

PALANTIR TECHNOLOGIES INC. fell 6.87% to $119.65 on Monday, marking its lowest close since June 2025 and its weakest intraday level since $119.76 — a level not seen in over a year. The slide comes amid broad software-sector weakness, but Palantir’s underperformance stands out: it ranked as the third-worst performer in both the S&P 500 and Nasdaq 100 on the session. Unlike peers such as NVIDIA and Tesla, whose AI narratives remain tightly coupled to hardware and autonomous systems, Palantir’s valuation hinges almost entirely on recurring government and enterprise software monetization — making contract visibility critical. With the Palantir France Contract now under public scrutiny and subject to multi-year replacement, investors are reassessing exposure to European sovereign risk and geopolitical headwinds.

How Does the Palantir France Contract Impact Valuation?

The Palantir France Contract — renewed at the end of 2025 for several additional years — remains legally in force, according to company statements. Yet Prime Minister Sebastien Lecornu confirmed ChapsVision has been formally retained to substitute Palantir’s tools, with integration expected to span “several years” to avoid capability gaps. That ambiguity is toxic for a stock trading at 88x forward earnings — a multiple far above peers like Apple (28x) and even high-growth AI enablers such as Micron Technology (12x). Wolfe Research recently upgraded Palantir to “Peer Perform” from “Underperform” but declined to issue a price target, explicitly citing valuation concerns. Meanwhile, UBS maintains its “Buy” rating with a $200 price target — a 67% upside — but acknowledges near-term sentiment is tethered to contract stability and commercial execution.

Is Palantir’s Growth Still Compelling?

Yes — but the math is tightening. In Q1 2026, Palantir Technologies Inc. delivered $1.63 billion in revenue, up 84.7% year over year and beating consensus by $90 million. U.S. commercial revenue surged 133%, while government revenue grew 62%. Net income margin hit 53%, and the company raised full-year revenue guidance to 71% growth — up from 61% — implying $7.65 billion in annual revenue. Yet that elite growth is priced in: at $1.40 forward EPS, the 92x forward P/E demands flawless execution through 2027 and beyond. For context, NVIDIA trades at 23x forward earnings despite similar AI-driven growth — underscoring the market’s skepticism around Palantir’s scalability outside classified government work.

What Are the Broader Market Risks?

Three structural headwinds are converging: rising U.S. interest rates (Bank of America forecasts three Fed hikes in 2026), intensifying AI competition from Anthropic and OpenAI in government procurement, and weakening technical structure — with PLTR now trading well below its 50-day ($138.43) and 200-day ($160) moving averages. The stock’s IBD Composite Rating of 46 — well below the 90+ threshold for leading growth stocks — reflects heavy institutional selling. Insider activity added fuel: a Palantir director sold $2.1 million in shares on June 15 under a pre-set 10b5-1 plan, just days before the Palantir France Contract news broke. With beta at 1.515, PLTR magnifies every macro wobble — and Wall Street is clearly exhaling after three straight years of triple-digit gains.

Where Do Analysts Stand Now?

We don’t work with ICE, either through Palantir or anyone else. We don’t work with CBP. I don’t believe we work in Gaza.— Dario Amodei, CEO of Anthropic

Consensus remains cautiously bullish — but fractured. Of 33 firms tracked by FactSet, 17 rate Palantir Technologies Inc. as “Buy,” 11 as “Hold,” and 2 as “Sell.” The average price target stands at $182.75 — 52% above current levels — with Citigroup recently reiterating its $195 target and Morgan Stanley maintaining an “Overweight” rating. Yet RBC Capital Markets issued a neutral “Sector Perform” call last week, warning that “valuation compression is inevitable if Q2 commercial growth decelerates below 100%.” That’s the pivot: Palantir’s U.S. commercial momentum must sustain — or accelerate — to justify its multiple. Without it, the Palantir France Contract becomes less a one-off and more a precedent.