Can Palantir AI Strategy justify its towering valuation as Anthropic looms and Wall Street still pushes price targets higher?

Why Is Palantir AI Strategy Under Fire Now?

Palantir Technologies Inc. faces intensifying scrutiny as its valuation disconnect widens. Trading at a trailing P/E of 150 and a price-to-sales ratio of 61, the stock carries a forward multiple near 90—far above peers like Adobe, which just posted a 4.7% earnings jump on AI-fueled revenue growth. Free cash flow yield sits at just 0.70%, less than half of Snowflake’s 1.35%. With a $299 billion market cap—nearly 3.6x Snowflake’s $83 billion—investors are questioning whether Palantir’s Palantir AI Strategy delivers proportional returns. The stock’s 22% drop from its $161.45 resistance zone underscores mounting pressure.

How Is Palantir Defending Its Edge Against Anthropic?

CEO Alex Karp isn’t flinching. In a recent CNBC interview, he dismissed concerns that Anthropic—or OpenAI—can replicate Palantir’s enterprise footprint. While Anthropic’s $965 billion post-money valuation reflects Wall Street’s AI enthusiasm, Karp argues the real challenge isn’t building models—it’s deploying AI where errors are unacceptable. “If you want to manufacture a car and you need a part or you want to send a rocket to the moon… that stuff doesn’t ship,” he said. Palantir’s Palantir AI Strategy centers on deterministic, auditable, real-world AI—distinct from probabilistic chatbot use cases. That distinction is gaining traction with defense, aerospace, and industrial clients, where Palantir’s contracts with Lockheed, RTX, and General Dynamics anchor its relevance.

What Are Wall Street’s Latest Price Targets?

Despite volatility, top-tier firms are doubling down. BofA Securities maintained its Buy rating and lifted its price target to $255—the highest on record. Citigroup raised its target to $225 from $210, citing accelerating government adoption and improved commercial pipeline visibility. Wedbush reaffirmed its Outperform rating and $230 target, while Rosenblatt and Loop Capital both raised targets to $225 and $220, respectively. These moves reflect confidence that Palantir’s Palantir AI Strategy is not just surviving but evolving—especially as AI governance and secure data orchestration become non-negotiable for federal agencies.

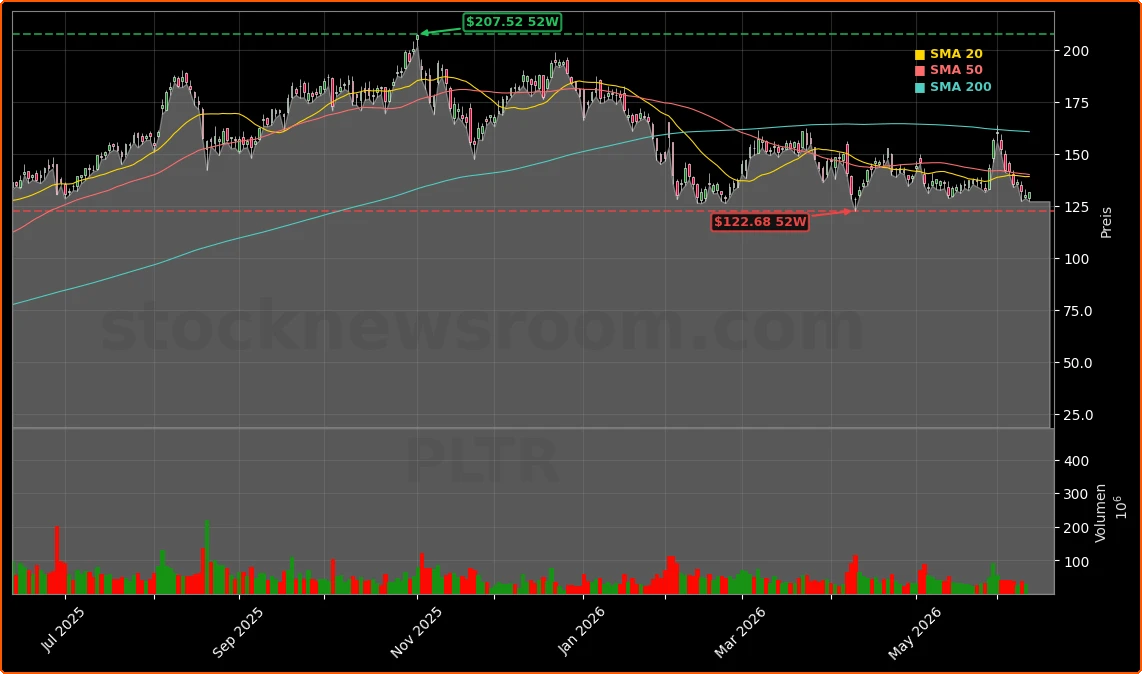

Is the Technical Picture Turning?

Technically, Palantir Technologies Inc. is testing critical support near $129.74—a zone that could trigger a reversal if held. Analysts note a developing inverted head-and-shoulders pattern, with the right shoulder forming slightly higher than the left—a bullish signal if the neckline at $138 breaks. A move above $160 would confirm trend reversal and open the path to $165 and beyond. Yet failure to hold support risks a slide toward the 500-day SMA and the psychologically important $100 level. That makes near-term price action a litmus test for investor conviction in Palantir’s long-term thesis—not just its AI narrative.

If you want to manufacture a car and you need a part or you want to send a rocket to the moon or you want to put a missile on your adversary’s head and bring home Americans safely, that stuff doesn’t ship.— Alex Karp, CEO of Palantir Technologies Inc.

Related Coverage: Palantir’s recent partnership slowdown—detailed in Palantir Partnerships Drop 3.3% as Valuation Fears Rise—adds pressure, but contrasts sharply with Adobe’s AI-fueled earnings beat, which proves enterprise AI monetization is possible when tied to clear workflows and recurring revenue. Meanwhile, investors watching the AI infrastructure layer should note that Snowflake—a quiet but essential enabler beneath Palantir and NVIDIA—delivered its strongest sequential growth quarter in company history even as Palantir’s stock cracked. That divergence underscores a broader market shift: from AI hype to AI utility.