Can Palantir’s explosive AI growth keep supporting a sky-high premium, or is the market finally pushing back on valuation?

Why is Palantir Valuation under pressure?

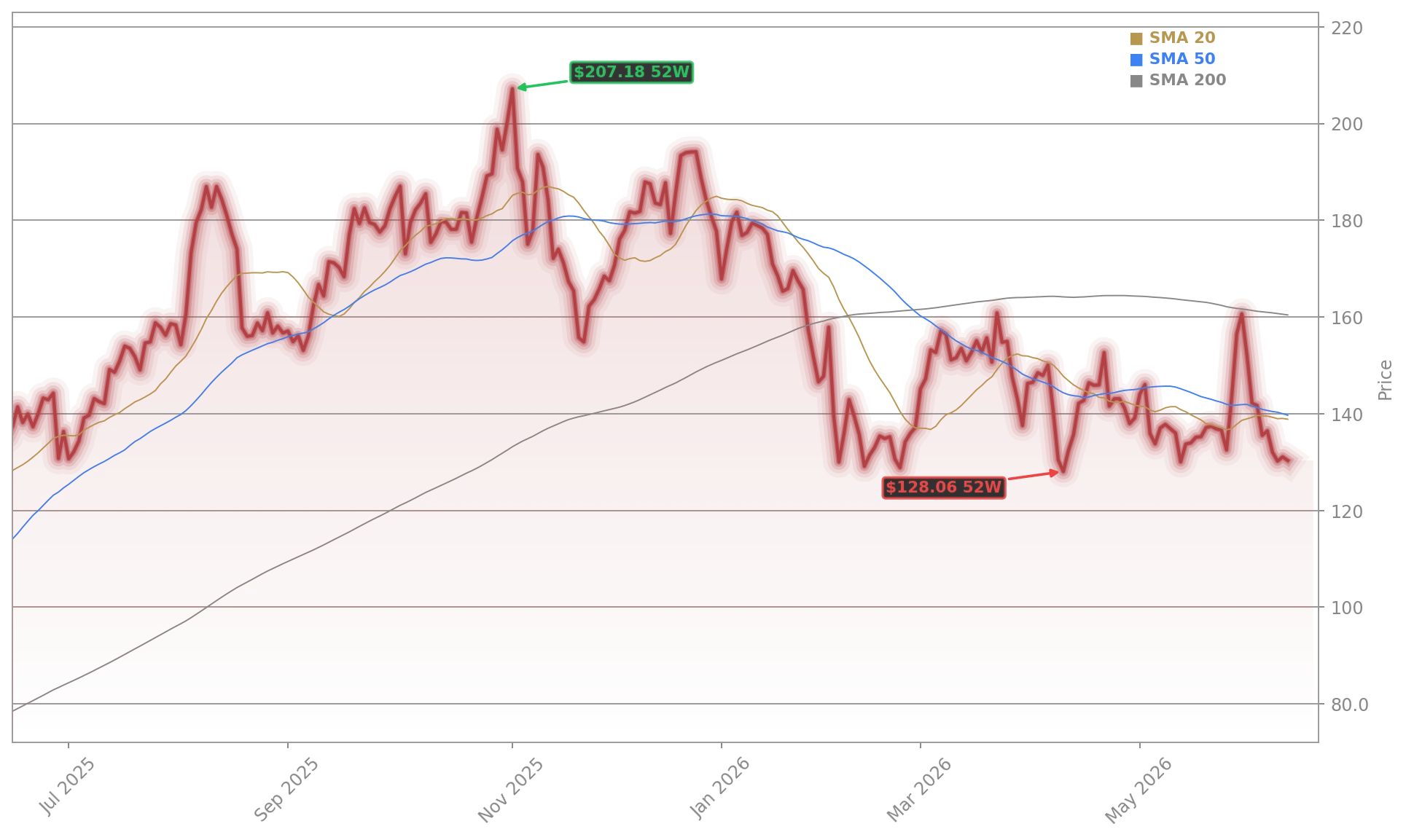

Palantir Technologies Inc. is still one of the market’s most polarizing AI names. In intraday trading Tuesday, the stock gave back part of its recent rally as investors reassessed whether the company’s premium can stretch further. TradingKey pointed to elevated valuation, sensitivity to broader tech sentiment, and heavier AI competition as key reasons behind the move. That logic fits the current setup: when a stock trades at extreme sales and earnings multiples, even small shifts in risk appetite can hit hard.

That is why Palantir Valuation matters more than almost any single quarterly metric. Even bullish commentary around enterprise AI infrastructure has not erased concerns that PLTR already discounts years of upside. Recent coverage tied Monday’s strength to a broader software rebound after upbeat results from other technology names, but Tuesday’s reversal shows how fragile momentum can be when expectations are this high.

Can Palantir keep justifying the premium?

The bull case is not hard to find. Palantir has positioned itself as a critical data and decision layer for government and commercial AI deployments. Its platforms have deep links to defense programs, and recent contract wins have kept enthusiasm elevated. Investors also continue to focus on explosive commercial expansion, especially in the U.S. market, where Artificial Intelligence Platform adoption has become a major growth engine.

Recent company figures cited across market coverage showed revenue of $1.41 billion, up 70% year over year, with U.S. commercial revenue jumping 137% to $507 million. GAAP operating income reached $575.4 million, implying a 41% margin. Those are eye-catching numbers and help explain why some investors compare Palantir’s strategic position to infrastructure leaders rather than traditional software vendors. Still, the same reports also highlighted a P/E ratio above 200 and a valuation near 72 times sales, a level that stands out even against AI favorites such as NVIDIA.

That leaves Palantir Valuation in a difficult place. Strong execution clearly supports a premium, but the market is asking whether the premium has become detached from a reasonable forward return profile.

How does Palantir compare with peers?

On Wall Street, PLTR increasingly trades as a hybrid of defense software and AI platform infrastructure. That gives it a different narrative than Salesforce, ServiceNow, or Tesla, but not immunity from comparison. Investor’s Business Daily highlighted a software rally that lifted Palantir alongside Snowflake and Dell, while Benzinga noted Wedbush analyst Dan Ives sees the data layer as the next major AI monetization theme. Even with that favorable backdrop, valuation remains the dividing line between believers and skeptics.

Some institutional investors have also shown more caution. Yahoo Finance reported that Renaissance Technologies continued trimming its stake in Q1 2026, even as Palantir’s business trends remained strong. That does not invalidate the long-term thesis, but it does suggest sophisticated investors are balancing opportunity against crowding and multiple risk. Meanwhile, partnership mentions tied to enterprise AI infrastructure, including Rackspace’s work with Palantir, support the idea that the company is becoming more embedded in regulated AI deployments.

What should investors watch next?

The next question is whether PLTR can hold the roughly $150 area after this pullback. Recent market commentary suggested investors were looking for stabilization in the $150 to $160 range before any renewed push higher. If the stock does base there, bulls will argue the market is digesting gains rather than breaking trend. If it slips further, Palantir Valuation will likely dominate the conversation again.

Related Coverage: Investors following the recent surge should also read this analysis of Palantir Forecast and Pentagon-driven AI demand. It explores whether commercial momentum and defense spending can continue to outweigh valuation concerns, a question that fits perfectly with today’s retreat in PLTR.

Palantir’s Rule of 40 score is now an incredible 127%… We are an n of 1.— Alex Karp

Palantir Valuation remains the key investment debate: the business is executing at a remarkable level, but the stock still trades as if exceptional growth and margin expansion will continue for years. For investors, that means every contract win, commercial update, and earnings report matters more than usual. If management keeps delivering, PLTR can stay a market leader; if growth normalizes, Palantir Valuation could become a bigger headwind than today’s intraday drop suggests.