Is the ServiceNow AI Re-rating the start of a durable comeback, or just a sharp bounce in a still-volatile software trade?

Why is the ServiceNow AI Re-rating gaining traction?

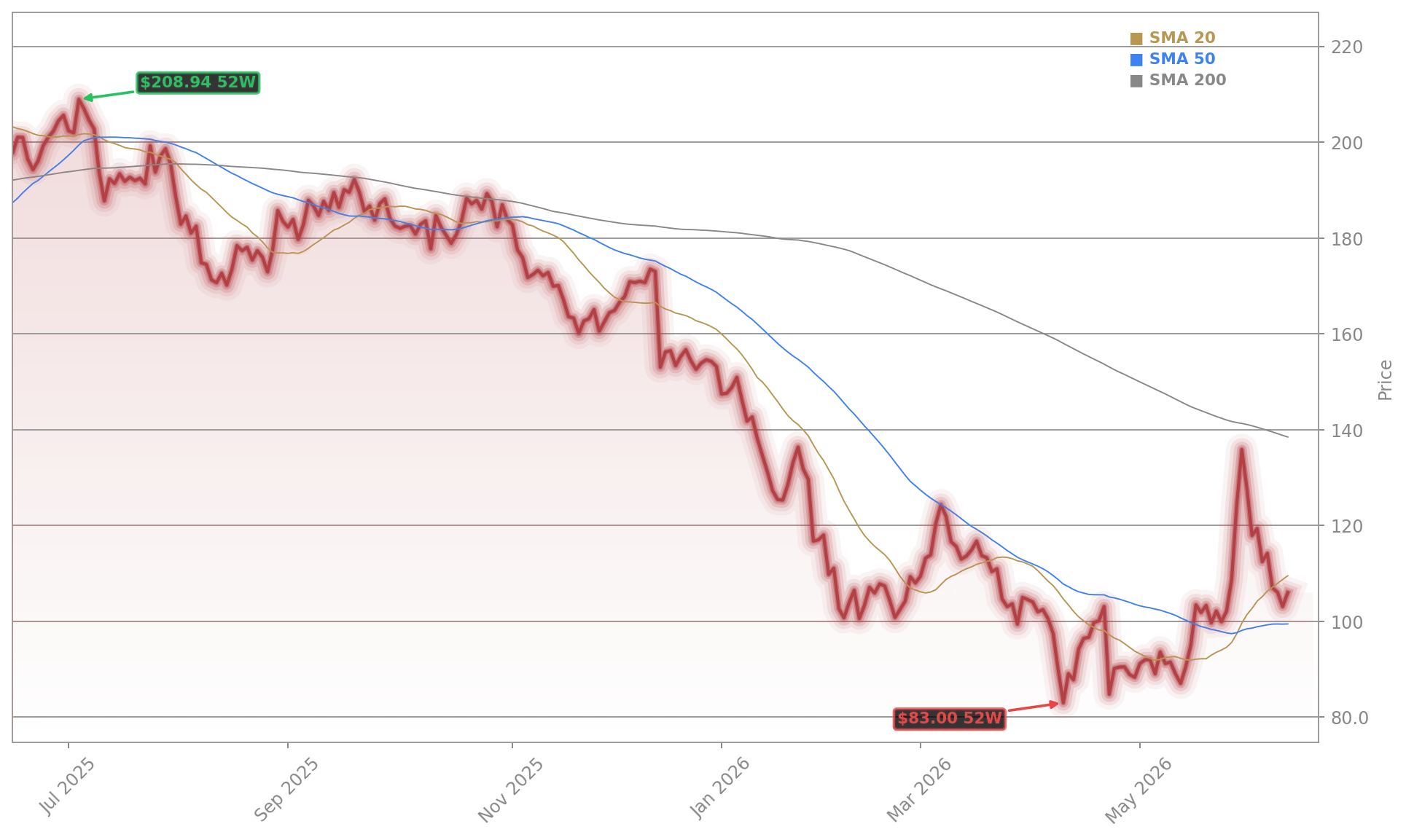

The latest rally in ServiceNow, Inc. was part of a broader software rebound that also lifted NVIDIA, Salesforce, Adobe, and other enterprise names. Investors responded to comments from Nvidia CEO Jensen Huang that AI agents will require more software tools, easing a key fear that generative AI could cannibalize legacy software spending. That narrative shift has been especially powerful for ServiceNow because the stock had previously fallen sharply from its 52-week high of $211.28. Even after Monday’s jump, shares remain well below that high, which means this is not a breakout to new highs but a meaningful repricing from depressed levels.

The ServiceNow AI Re-rating is also being supported by technical momentum. The stock has approached the $140 area, a level traders have watched as an important resistance zone. Holding above the low-$130s has strengthened the short-term setup, although volatility may remain elevated after such a steep rebound.

Can ServiceNow fundamentals support the move?

Fundamentals have clearly helped fuel the turnaround. In Q1 2026, revenue rose 22.1% year over year to $3.77 billion, while remaining performance obligations increased 22.5% to $12.64 billion. Those figures reinforced the view that enterprise demand remains healthy despite concerns about hiring pressure and tighter IT budgets.

Management’s AI strategy also matters. ServiceNow has said 50% of new deals are now usage-based rather than seat-based, an important distinction as investors debate how AI agents will change software monetization. The company’s Now Assist product is targeted to reach $1.5 billion in annual contract value by the end of 2026, suggesting AI is becoming a revenue driver rather than just a product feature.

There are also signs of unusual customer stickiness. Retention has been running around 97% to 98%, and ServiceNow already serves roughly 80% of the S&P 500. That installed base gives the company a strong position if enterprises expand AI-enabled automation across IT, security, HR, finance, and customer workflows.

What are analysts and funds seeing in ServiceNow?

Wall Street firms have become more constructive. Bank of America reinstated coverage with a Buy rating and a $130 price target, arguing that ServiceNow should benefit from AI adoption rather than be displaced by it. Oppenheimer reiterated an Outperform rating and a $130 target after customer checks pointed to healthy software demand and stronger conviction for the second half of 2026. MarketBeat data also showed a broader analyst consensus near $141.85, indicating room for debate but generally supportive sentiment.

Institutional investors have also been adding exposure. Hedge fund ownership reached 108 funds in Q1 2026 with an aggregate value of $5.45 billion. Separate filings highlighted fresh buying from retirement and capital management firms, while other large investors sharply increased stakes earlier this year. For portfolio managers, that combination of improving sentiment and renewed sponsorship often matters as much as the headline move itself.

How does ServiceNow compare with peers?

The ServiceNow AI Re-rating is unfolding within a wider rotation back into software. Apple ecosystem demand, Tesla automation debates, and the hardware-led AI boom have dominated markets for months, but software names are now reclaiming attention. ServiceNow stands out because it sits closer to the system-of-record layer that AI agents may need to operate inside enterprises. That distinguishes it from more discretionary software spending and puts it in the same strategic conversation as Salesforce, SAP, and Oracle.

Related Coverage: Investors tracking this rebound may also want to read this analysis of whether Bank of America’s AI-driven upgrade can support a longer ServiceNow rally. That piece examines the earlier turn in sentiment and helps frame whether the current move is a squeeze, a durable re-rating, or the start of a broader software leadership shift.

The ServiceNow AI Re-rating now looks like more than a one-day momentum spike, because it is being backed by solid Q1 growth, stronger AI monetization, and renewed analyst confidence. For investors, the next test is whether shares can consolidate gains near $140 while the company keeps proving that AI expands software demand instead of replacing it.