Can ServiceNow AI Strategy turn enterprise AI hype into durable growth even as the stock drops 4.4%?

Why Is ServiceNow AI Strategy Gaining Traction Now?

ServiceNow AI Strategy is no longer about bolt-on chatbots — it’s about becoming the enterprise’s AI control tower. CEO Bill McDermott calls it the ‘AI control tower for business reinvention,’ and the architecture backs it up: seamless integration with any LLM, cloud, data silo, or legacy system. That interoperability explains why 85% of Fortune 500 companies rely on ServiceNow — and why Nvidia CEO Jensen Huang publicly anoints it the ‘enterprise operating system’ for AI. With over 8,800 subscription customers and $12.64 billion in current remaining performance obligations (up 22.5% YoY), ServiceNow’s revenue visibility is among the strongest in the S&P 500 software cohort. The platform’s agentic AI expansion — where autonomous workflows trigger cross-system actions — is directly lifting average contract value, especially among high-tier clients: Now Assist customers spending over $1 million ACV grew 130% YoY.

How Do Acquisitions Reinforce ServiceNow AI Strategy?

ServiceNow isn’t waiting for AI adoption to mature — it’s engineering the infrastructure for it. The $7.75 billion acquisition of Armis in April 2026 tripled its addressable market in AI-powered cybersecurity, while the earlier Veza purchase embedded real-time, AI-driven identity governance directly into the Now Platform. These moves signal a decisive pivot from pure IT workflow automation to full-stack AI infrastructure — one that sits between foundational AI providers like NVIDIA and enterprise adopters like Tesla and Apple. Unlike point-solution AI startups, ServiceNow’s embedded position across HR, IT, security, and customer service creates defensibility: replacing it would mean tearing down and rebuilding decades of integrated digital process logic. That’s why IBM partnered with ServiceNow in Q2 2026 — not to compete, but to co-develop AI-ready modernization layers for legacy mainframe and ERP environments, launching commercially in H2 2026.

What Do Q1 Numbers Say About Profitability and Scale?

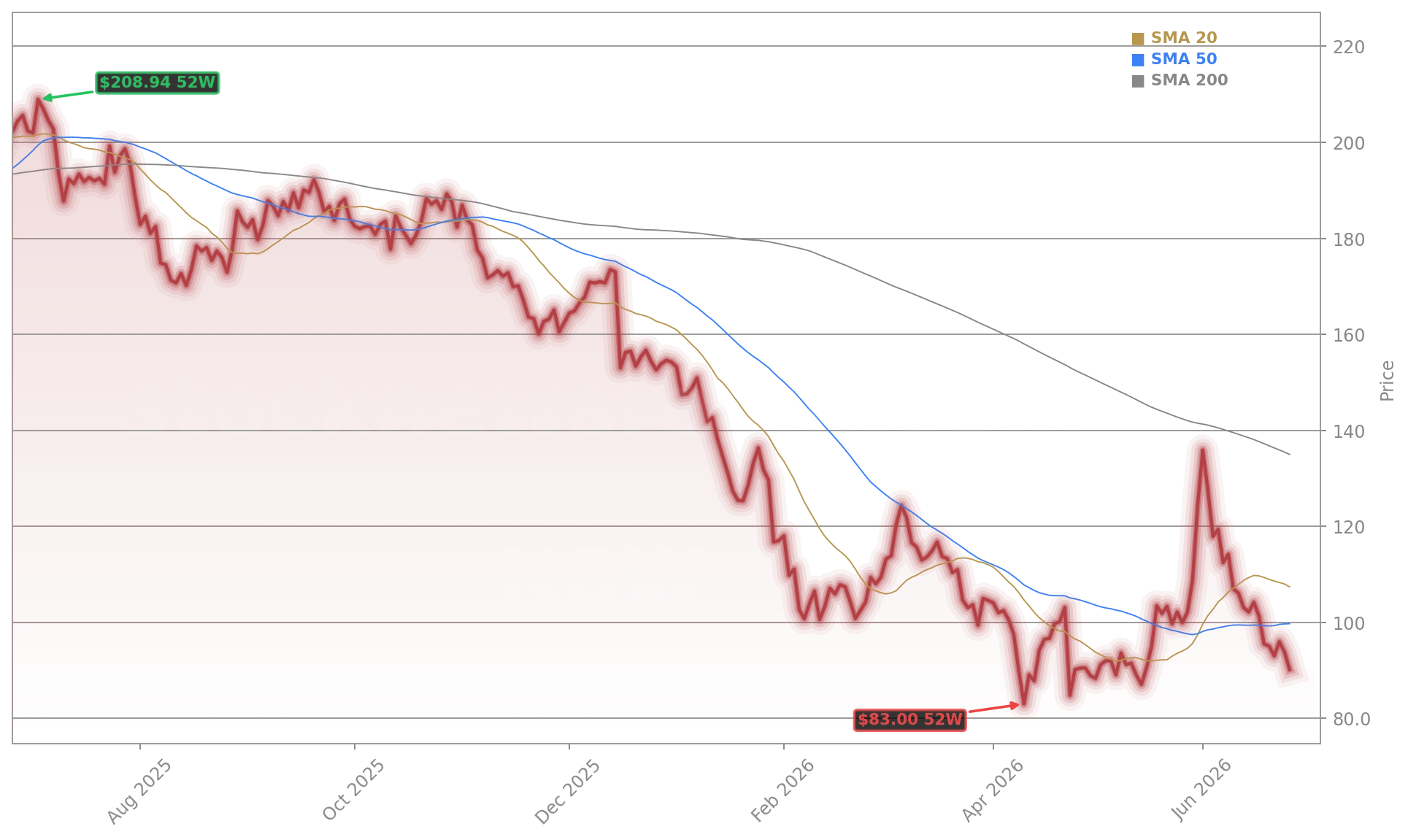

Q1 2026 delivered $3.77 billion in total revenue (up 22% YoY) and $3.67 billion in subscription revenue (up 19%). Gross margin held at 82%, and non-GAAP operating margin expanded to 31.2% — proof that scale and AI-driven efficiency are compounding. Crucially, total remaining performance obligations reached $27.7 billion, with $12.64 billion classified as ‘current’ — offering unmatched 12-month revenue visibility in a volatile macro environment. That backlog strength directly enabled management to raise its full-year subscription revenue guidance to $15.15–$15.20 billion, up from $15.05–$15.15 billion. The 97% customer renewal rate confirms sticky demand, even as the broader NASDAQ faces AI-valuation scrutiny. Notably, ServiceNow’s valuation disconnect — trading 57% below the $125.05 average analyst price target — reflects sentiment lag, not fundamentals.

How Are Analysts Reacting to ServiceNow AI Strategy?

Wall Street is shifting from skepticism to strategic conviction. Citigroup lifted its price target to $118 and reiterated a ‘Buy’ rating, citing ‘Now Assist monetization accelerating faster than expected.’ RBC Capital Markets upgraded ServiceNow, Inc. to ‘Outperform,’ highlighting the IBM co-innovation pipeline and Armis integration synergy as ‘material near-term catalysts.’ Goldman Sachs raised its 2027 EPS estimate by 8% and noted that ServiceNow AI Strategy ‘addresses the critical missing layer between AI models and enterprise execution — a moat few software firms possess.’ Morgan Stanley added ServiceNow, Inc. to its ‘Top Picks’ list, emphasizing that its workflow-first AI approach avoids the commoditization risks facing pure-play inference layer vendors. With a $85 billion market cap and 22% top-line growth, ServiceNow, Inc. trades at a significant discount to peers like Microsoft and Apple, despite superior growth consistency and margin expansion.

Where Does This Leave ServiceNow in the AI Stack?

ServiceNow, Inc. occupies a uniquely advantaged tier in the AI value chain: not a creator like NVIDIA, not a builder like Broadcom, but the dominant enterprise ‘adopter enabler.’ Its ServiceNow AI Strategy bridges the gap between theoretical AI promise and operational reality — turning fragmented models, data lakes, and legacy systems into governed, auditable, scalable workflows. While the S&P 500 rose 1.2% in June, ServiceNow, Inc. lagged — but that underperformance may now be the entry point. With H2 2026 set to deliver IBM co-solutions, Armis security AI rollouts, and expanded Now Assist enterprise deployments, the catalysts for re-rating are tangible and near-term. The market’s volatility — with 30-day annualized volatility above 78% — reflects uncertainty, not weakness. In fact, it signals a classic inflection: the moment when infrastructure becomes indispensable.

ServiceNow is the enterprise operating system for AI — it’s where AI gets work done.— Jensen Huang, CEO of NVIDIA

Related Coverage: For deeper analysis on how ServiceNow AI Strategy is reshaping enterprise AI adoption timelines, read ServiceNow AI Strategy Jumps 3.6% as AI Targets Rise. Meanwhile, investors weighing broader tech margin risks should consider Microsoft Xbox Price Hike: -2.9% Warning for Microsoft Stock, which highlights growing pricing pressure across hardware-adjacent software ecosystems.