Can ServiceNow AI Strategy turn enterprise AI hype into durable growth, or is Wall Street getting ahead of itself again?

Is ServiceNow AI Strategy Reshaping the Enterprise Stack?

ServiceNow, Inc. is no longer positioning itself as a digital workflow vendor — it’s declaring itself the AI Control Tower for global enterprises. The ServiceNow AI Strategy now centers on unifying legacy systems, cloud applications, and multi-vendor AI agents under a single governance and action layer. This ‘Enterprise Control Plane’ vision gained momentum in June with expanded alliances with IBM and Aria Systems, and a strategic partnership with Inspira Enterprise to deliver integrated AI governance and cybersecurity solutions. Unlike pure-play AI infrastructure firms, ServiceNow leverages deep enterprise entrenchment: over 630 customers now hold contracts worth $5 million or more annually, and current remaining performance obligations stand at $12.64 billion — up 22.5% year-over-year. That stickiness provides a critical moat as AI-native competitors like Salesforce (CRM) and NVIDIA race to embed agents directly into CRM or infrastructure layers.

How Are AI Monetization Metrics Actually Performing?

Contrary to the narrative of AI-as-disruption, ServiceNow’s AI monetization is accelerating — not stalling. Now Assist net new annual contract value more than doubled year-over-year in Q4 2025, and by Q1 2026, AI-related ACV reached $750 million. Management has raised its 2026 target to $1.5 billion — a critical milestone investors will scrutinize. Crucially, deals bundling three or more Now Assist products grew nearly 70% YoY, and 36 contracts included five or more AI capabilities. This signals enterprise adoption is moving beyond pilots into production-scale deployments. The April 2026 pricing overhaul — replacing legacy editions with Foundation, Advanced, and Prime tiers, all embedding AI usage by default — confirms AI is no longer an add-on but the platform’s architectural core.

Why Are Analysts Raising Targets Amid Volatility?

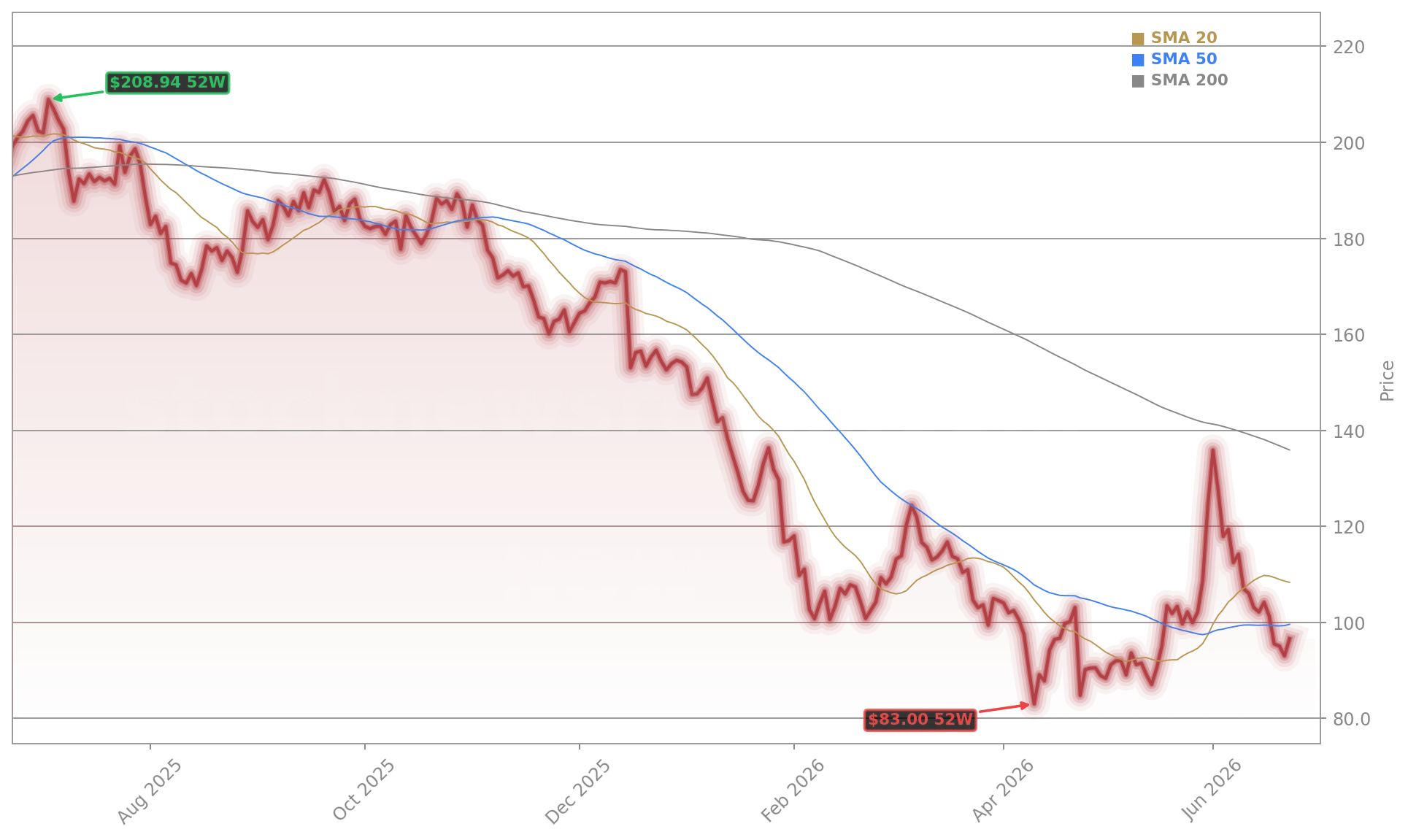

Despite a 51.6% one-year decline and 50-day/200-day moving average gaps, Wall Street remains bullish on ServiceNow, Inc. Benchmark reiterated its Buy rating and raised its price target to $130 from $125, citing confidence in long-term operating leverage and Agentic AI cybersecurity workflows. J.P. Morgan assigned an Overweight rating with a $145 target, while Citigroup maintains a Buy with a $132 price target. The consensus target stands at $141.98 — implying ~49% upside from current levels. Analysts emphasize the company’s fortress balance sheet ($4.58 billion FY25 free cash flow, up 34%), 32% non-GAAP operating margin guidance, and $5 billion buyback authorization. As Citigroup notes, ‘ServiceNow’s AI Control Tower narrative is gaining real-world validation in contract structure and cross-sell velocity.’

What’s Holding Back the Stock — Beyond AI?

The disconnect between fundamentals and valuation stems less from ServiceNow, Inc.’s execution and more from macro forces. Software stocks are among the most interest-rate-sensitive on Wall Street — and with the 10-year Treasury yield hovering near 4.8%, high-multiple growth names remain under pressure. A stronger-than-expected May jobs report (172,000 new positions) damped rate-cut expectations and triggered a 5% single-day drop. Technical indicators reflect the strain: the 30-day annualized volatility sits at 78.71%, and the RSI recently dipped to 40.4 — near oversold territory. Yet the June 23 rebound (+3.64% to $96.40) signals growing conviction that the selloff has overshot — especially as peers like Salesforce and Apple face similar macro headwinds. The next catalyst arrives July 24 with Q2 earnings, where investors will parse margin impact from the $2.85 billion Moveworks and $1.2 billion Armis acquisitions.

Can the Control Plane Vision Withstand Platform Fragmentation?

The biggest strategic risk isn’t competition — it’s interoperability. ServiceNow’s AI Control Tower requires seamless integration across AWS, Google Cloud, and Microsoft Agent 365. While open standards like OpenTelemetry enable visibility in public cloud environments, closed ecosystems like SAP’s Joule remain unconnected until late 2026. Until then, enterprises operate with ‘five control towers’ — one per major platform — undermining ServiceNow’s central governance thesis. That’s why the IBM partnership is pivotal: it targets precisely the ‘alt-system’ integration bottleneck. If joint solutions launch successfully in H2 2026 and demonstrate measurable cost reduction (e.g., 70% lower telecom billing ops via Aria), the ServiceNow AI Strategy shifts from promise to proof point — and valuation multiples may follow.

There’s a perfect correlation between enterprise AI from any source and ServiceNow’s expansion.— Bill McDermott, CEO of ServiceNow, Inc.

Related coverage: For deeper analysis on ServiceNow’s AI Control Tower momentum, see ServiceNow AI Strategy +1.7% as AI Control Story Gains. On the broader sector implications of AI spending pressure, read Oracle Job Cuts -5.3%: AI Spending Surge Sparks Warning.