Can the Sunrun Tesla Deal turn home batteries into a serious AI power business before Wall Street’s excitement outruns the revenue?

What Does the Sunrun Tesla Deal Mean for Wall Street?

Sunrun’s 26% intraday rally — its largest since August 2025 — reflects investor recognition that the Sunrun Tesla Deal redefines the company’s revenue model. No longer just a residential solar installer, Sunrun is now positioned as a distributed grid operator. The 16-GW VPP leverages Sunrun’s ~300,000 home battery systems, Tesla’s Powerwall fleet, and Renew Home’s network of 8 million smart thermostats and connected devices. Crucially, the infrastructure is already deployed — meaning monetization can begin immediately. For U.S. utilities and hyperscalers facing 12-month interconnection delays and skyrocketing power costs, this is infrastructure that arrives in months, not years. The deal’s timing aligns with Goldman Sachs Commodities Research projections that U.S. data center demand will hit 41 GW in 2026 and 66 GW in 2027 — a $200+ billion annual power market Sunrun now aims to serve.

How Does This Compare to NVIDIA and Apple’s Energy Strategies?

While NVIDIA’s chips drive AI power demand, and Apple pursues 100% renewable data center power via long-term PPAs, Sunrun’s model is fundamentally different: it’s dispatchable, distributed, and revenue-generating per kilowatt-hour delivered. Unlike utility-scale solar or nuclear — which require years of permitting and billions in capex — the Sunrun Tesla Deal turns existing residential assets into a real-time grid resource. That agility matters. In Virginia’s Data Center Alley, the coalition already has 300 MW available for immediate deployment, with 500 MW targeted by 2030. PJM Interconnection’s proposed Reliability Backstop Process could unlock over 1 GW of committed capacity — a near-term catalyst for recurring revenue. Analysts at RBC Capital Markets note the model’s scalability could make Sunrun a ‘grid-as-a-service’ provider — a concept gaining traction amid S&P 500 utility sector volatility.

Is This Deal Backed by Real Revenue or Just Hype?

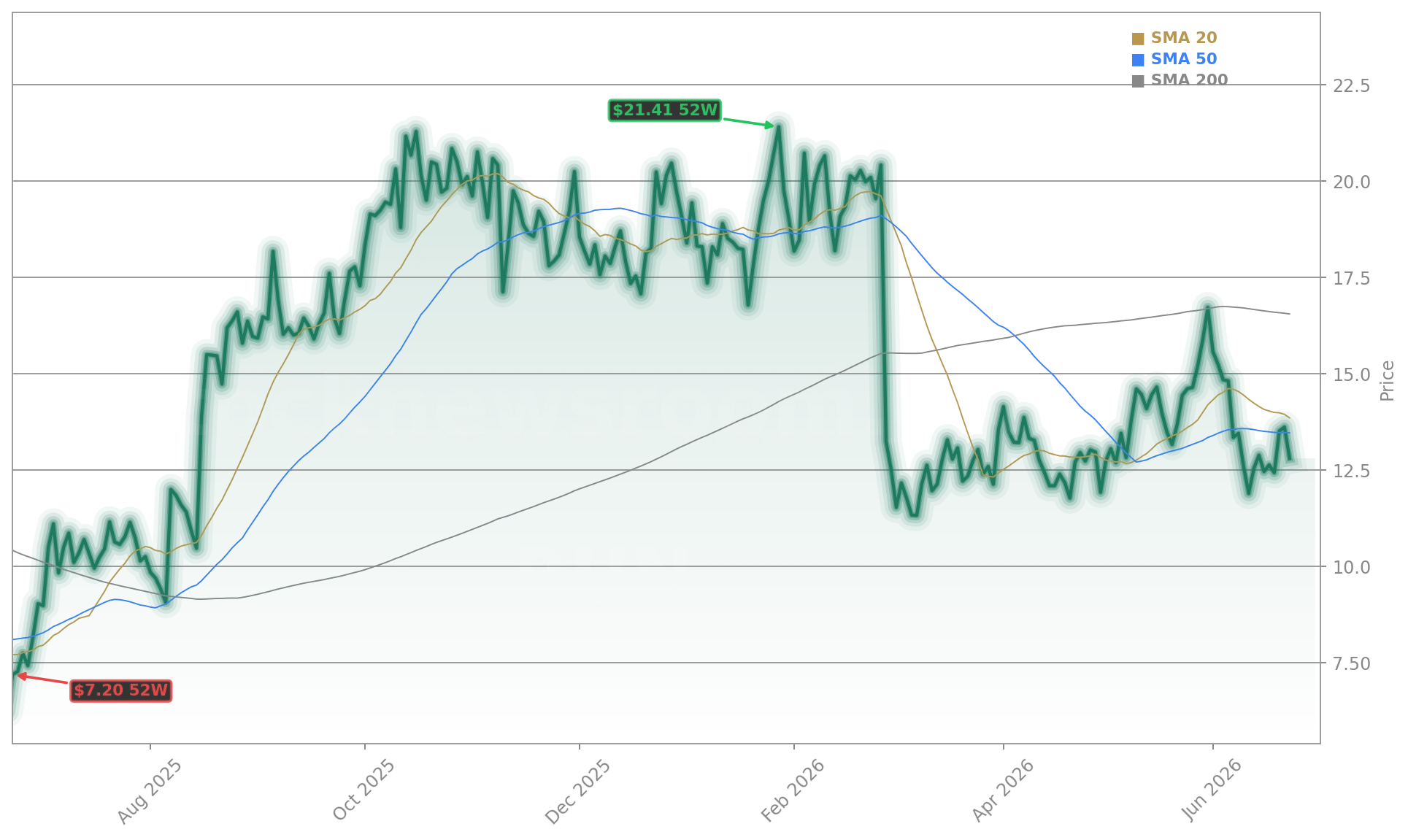

The Sunrun Tesla Deal is a capacity-as-a-solution framework — not yet backed by signed, multi-year hyperscaler contracts. That distinction matters. Sunrun’s Q1 2026 results showed strong fundamentals: $722 million in revenue (+43% YoY) and a record 73% storage attachment rate — validating its hardware and customer base. But bear-case concerns remain, including regulatory approvals, utility program adoption, and enrollment rates. The current consensus price target for Sunrun stands at $19.11, supported by 3 Strong Buy and 9 Buy ratings versus 10 Holds, according to Bloomberg data. Citigroup recently raised its price target to $21.50, citing ‘accelerated VPP monetization potential.’ Still, Sunrun remains down 11% year-to-date — underscoring investor caution until revenue visibility improves.

What’s Next for Sunrun Investors?

The grid of the 1800s cannot power the innovation of 2026.— Mary Powell, CEO of Sunrun

Three near-term catalysts will determine whether the Sunrun Tesla Deal transitions from headline to earnings driver. First, confirmation of hyperscaler offtake agreements — especially from firms with massive, AI-driven load profiles. Second, formal allocation under PJM’s Reliability Backstop Process, expected this quarter. Third, expansion beyond Virginia into Texas (ERCOT) and the Midwest (MISO), where grid constraints are acute. Management has signaled that initial revenue from the VPP could begin in Q3 2026. For investors, this represents a high-conviction, high-volatility bet on grid modernization — one that sits at the intersection of AI infrastructure, energy transition, and residential tech. With Tesla and Renew Home as co-architects, execution risk is lower than typical startups — but contract conversion remains the gatekeeper to sustained upside.