Can Palantir’s explosive AI growth keep pushing the stock higher, or is valuation finally becoming the market’s biggest obstacle?

Why is Palantir moving now?

Palantir Technologies Inc. is trading near its session highs on Thursday, extending renewed momentum in one of Wall Street’s most closely watched AI names. The latest Palantir Forecast has turned more constructive as investors revisit the company’s Q4 2025 performance, where revenue reached $1.406 billion, up 70% year over year, while U.S. commercial revenue surged 137%. The company’s Rule of 40 score of 127% also stands out even among elite software peers.

That operating strength is helping offset a debate that has followed PLTR for months: whether growth can stay strong enough to justify a very rich earnings multiple. With the stock now rebounding from prior compression, traders appear increasingly willing to pay for execution again, especially as AI leaders like NVIDIA and Meta continue to shape risk appetite across the sector.

Palantir Forecast: what supports the bull case?

The bull case centers on continued commercial adoption and the spread of Palantir’s enterprise AI platform into industrial and government workflows. This week, Cleveland-Cliffs highlighted a new three-year strategic partnership with Palantir focused on an enterprise AI platform, reinforcing the company’s position beyond defense and intelligence. Another recent industry update tied Innodata’s evolving AI engineering role to work with Palantir and the U.S. Missile Defense Agency, suggesting the broader ecosystem around Palantir remains active.

That matters because the Palantir Forecast depends less on one quarter and more on whether management can sustain triple-digit growth in key segments. Some market chatter has also circulated around aggressive upside targets, including speculative references to much higher numbers. Still, the more grounded benchmark remains the Wall Street consensus target near $183.73. The analyst mix behind that view includes 1 Strong Buy, 18 Buy, 10 Hold, 1 Sell, and 1 Strong Sell, showing support, but not blind unanimity.

How big is the valuation challenge?

This is where the story gets harder. Even after today’s move, valuation remains the central hurdle in any Palantir Forecast. Some estimates place PLTR at roughly 123 times forward earnings, while more optimistic scenarios toward $225 in 2027 would imply a multiple above 200 times based on forward EPS assumptions near $1.11. That leaves little room for execution missteps or slower demand.

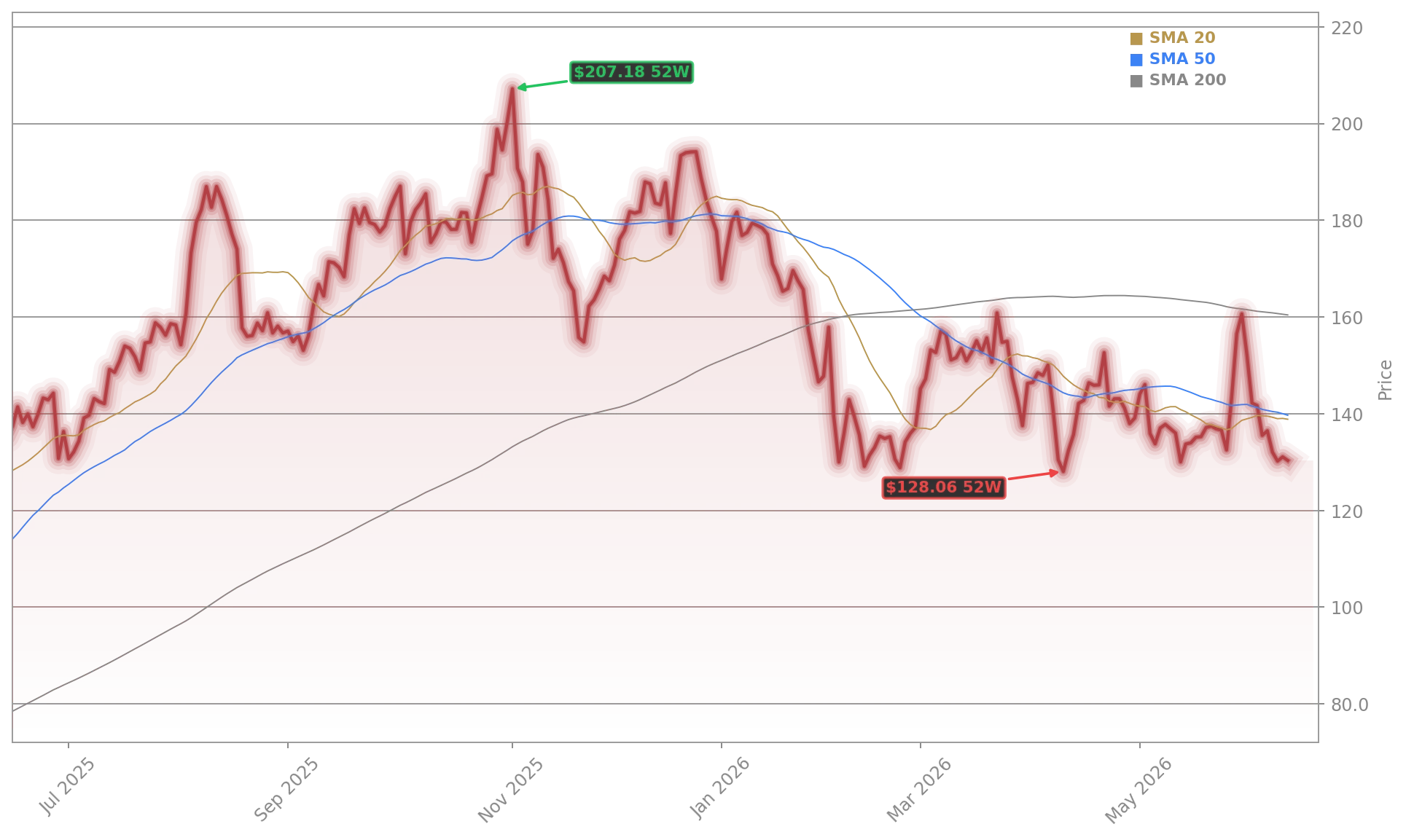

Volatility also cuts both ways. Palantir’s beta above 1.5 means multiple compression can hit harder than it does for steadier software names. A recent internal modeling framework cited a base case around $152.01, with a bull case of $198.75 and a bear case of $138.52. With the stock at $139.80 intraday, that range shows upside exists, but it is no longer obvious or cheap. Compared with mature mega-cap platforms such as Apple and Tesla, Palantir still trades more like a high-expectation growth vehicle than a conventional large-cap software stock.

What should investors watch next?

For American investors, the next test is whether fundamentals keep outrunning the valuation debate. Continued strength in U.S. commercial bookings, free cash flow execution, and new enterprise partnerships would all support a stronger Palantir Forecast into the second half of 2026. Industry screens have also kept Palantir in broader cybersecurity and AI stock baskets, which can help maintain visibility as long as sector sentiment stays constructive.

Related Coverage: Investors looking for a deeper look at the growth-versus-valuation debate can also read Palantir AI Strategy: 85% Growth Boom vs. Rich Valuation. That analysis explores whether the company’s AI platform momentum can keep driving a rerating, while also framing the risks of owning a stock that already prices in major future success.

The bottom line for the Palantir Forecast is clear: the business is still executing at a level few software companies can match, but the stock’s next leg higher depends on proving that growth can stay extraordinary for longer. If commercial AI adoption keeps broadening and sentiment around premium AI names remains firm, PLTR could still work higher from here. For investors, the next earnings and contract updates may decide whether today’s intraday surge becomes a durable breakout.