Can blockbuster Palantir Earnings and an 85% revenue surge still justify a triple‑digit valuation after a sharp share price reset?

Do Palantir Earnings justify the current slide?

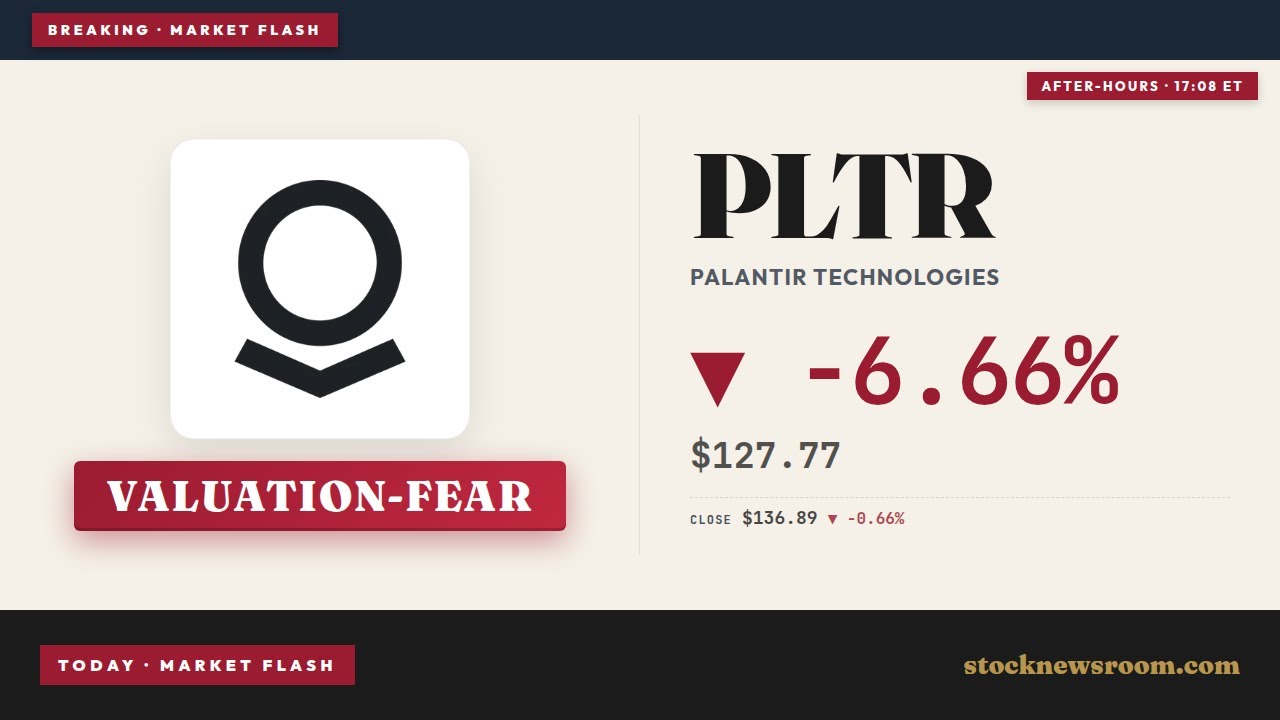

Despite an intraday dip of around 0.7% on Monday and additional weakness after the close, Palantir Technologies Inc. remains one of the strongest multi‑year winners on the NASDAQ, up more than 1,000% over three years even after a sharp correction from its 2024 highs above $200. Year to date, however, the stock is under pressure and now trades well below its peak, while bears argue that valuation rather than fundamentals is finally driving the price.

The latest Palantir Earnings for Q1 2026 showed revenue surging 85% year over year to $1.63 billion, beating Wall Street estimates of roughly $1.54 billion. Adjusted earnings climbed to $0.33 per share, up from $0.13 a year earlier and ahead of expectations around $0.28. Adjusted gross margin held at a robust 88%, while operating income rose about 60% and net income grew 53%, signaling that scale is translating into meaningful profitability rather than just top‑line growth.

Yet PLTR shares have dropped roughly 20%+ over the past six months even after this beat‑and‑raise quarter, a pattern that highlights how extended expectations had become following three consecutive years of triple‑digit gains. On Monday, the stock’s modest decline came as investors continued to digest cautious commentary from major outlets about rising competition in AI tools and the sustainability of Palantir’s growth premium.

How strong is Palantir Technologies’ AI and government engine?

Under the hood of the Q1 2026 Palantir Earnings, the operating story looks unusually strong for a software company still in hyper‑growth mode. Total customer count climbed 31% year over year to 1,007, while total contract value signed in the quarter rose 61% to $2.4 billion. Remaining deal value nearly doubled to $11.8 billion, providing multi‑year visibility that most younger AI peers can only envy.

Growth is increasingly U.S.‑centric. Revenue from the company’s home market more than doubled and now accounts for close to 80% of total sales, powered by both commercial AI rollouts and long‑dated federal work. Recent wins include a Pentagon contract expanded to about $1.3 billion and a $300 million agreement with the U.S. Department of Agriculture, alongside continuing projects in the U.K. and other allied markets. Palantir’s AI Platform (AIP) is also helping its commercial business catch up to its government segment, with enterprise clients using the software to operationalize large language models on sensitive, regulated data.

Notably, Palantir’s go‑to‑market model remains lean. Management reports a sales force of roughly 70 people, relying heavily on forward‑deployed engineers embedded at clients rather than the large quota‑carrier armies typical at traditional SaaS vendors. Sales and marketing spend grew 35% year over year to $319 million, far below the 85% revenue growth rate, which is helping drive operating leverage and margin expansion.

Is Palantir Earnings growth enough to offset valuation fears?

For 2026, management has raised its revenue outlook to about $7.66 billion, up from a prior guide of $7.19 billion, implying roughly 71% growth versus 2025. Profitability guidance also moved higher, with the company signaling that further margin gains are likely as its AI platform scales. Some Wall Street analysts remain constructive: several firms maintain Buy ratings with average price targets more than 30% above current levels, even as others warn about downside. Jefferies, for example, has flagged valuation risk with a $70 target that implies roughly 50% downside from current prices, effectively betting that Palantir’s lofty multiple must compress.

At around $136, Palantir trades at roughly 150 times trailing earnings and near 100 times forward earnings, with a sales multiple near 70. Those levels are rich even compared with high‑growth AI peers and megacaps like NVIDIA or Apple, and they help explain why the stock has struggled despite accelerating fundamentals. Short‑oriented investors, including well‑known bear Michael Burry, have reportedly expressed skepticism through put positions tied to PLTR and chip‑heavy ETFs, arguing that an AI‑driven tech correction could hit the stock particularly hard.

The broader backdrop on Wall Street also matters. Semiconductors and high‑beta AI names have rallied dramatically over the past few years, and any pullback in the NASDAQ or S&P 500 could pressure richly valued software winners like Palantir and even bellwethers such as Tesla. A recent technical view suggests PLTR is consolidating between support near $125 and resistance around $150–$170, with a long‑term uptrend still intact but vulnerable if sentiment deteriorates.

What are the competitive and regulatory risks for Palantir Technologies?

Competitive intensity around AI platforms is rising quickly. Enterprise customers can increasingly choose from offerings built on top of models from OpenAI, Anthropic and major cloud platforms such as Microsoft and others. Hyperscalers are pushing deeper into data integration and analytics, while specialized enterprise‑AI vendors pitch more focused solutions. That raises questions about how durable Palantir’s moat is, particularly as off‑the‑shelf AI tools become more capable and cheaper.

Palantir argues that its advantage lies in deeply embedded deployments, integrated data governance and its forward‑deployed engineering model, which is hard to copy at scale. Its large U.S. government and allied defense contracts also tend to be sticky, with multi‑year terms and high switching costs. Still, the company’s focus on sensitive security and defense applications brings its own risks, including heightened political scrutiny, civil‑liberties debates and potential regulatory shifts in AI oversight on both sides of the Atlantic.

For U.S. investors, the question is whether Palantir can grow fast enough, and for long enough, to grow into its premium multiple before any macro‑driven de‑rating of AI and software valuations. Bulls point to the AI software platforms market, projected to grow from roughly $79 billion in 2025 to nearly $296 billion by 2030 at a 35% CAGR, and argue that Palantir’s current trajectory could support double‑digit billions in revenue by the end of the decade. Bears counter that even small disappointments in growth or margins could trigger an outsized reaction given how sentiment‑driven the stock has been.

Related Coverage

Investors who want a deeper dive into how AI demand and new Pentagon work are feeding into the Palantir Earnings story can read our recent feature, “Palantir Earnings +85% Surge: Can the AI Boom Last?”. That analysis looks more closely at the U.S. Army’s AI initiatives, compares Palantir’s trajectory with other AI‑driven software names, and examines whether the current growth pace can realistically support today’s valuation over the next several years.

In the end, the latest Palantir Earnings confirm that the company is executing exceptionally well on both AI and government contracts, even as the share price lags. For American investors, the stock now represents a pure play on high‑growth, high‑multiple AI software where sentiment can overpower fundamentals in the short term. The next few quarters will show whether continued contract wins and guidance raises are enough to keep Palantir in Wall Street’s good graces despite the persistent valuation overhang.