Is the latest NVIDIA Record rally a sustainable AI super-cycle or the moment when expectations finally outrun reality?

Is NVIDIA Record momentum still driving the market?

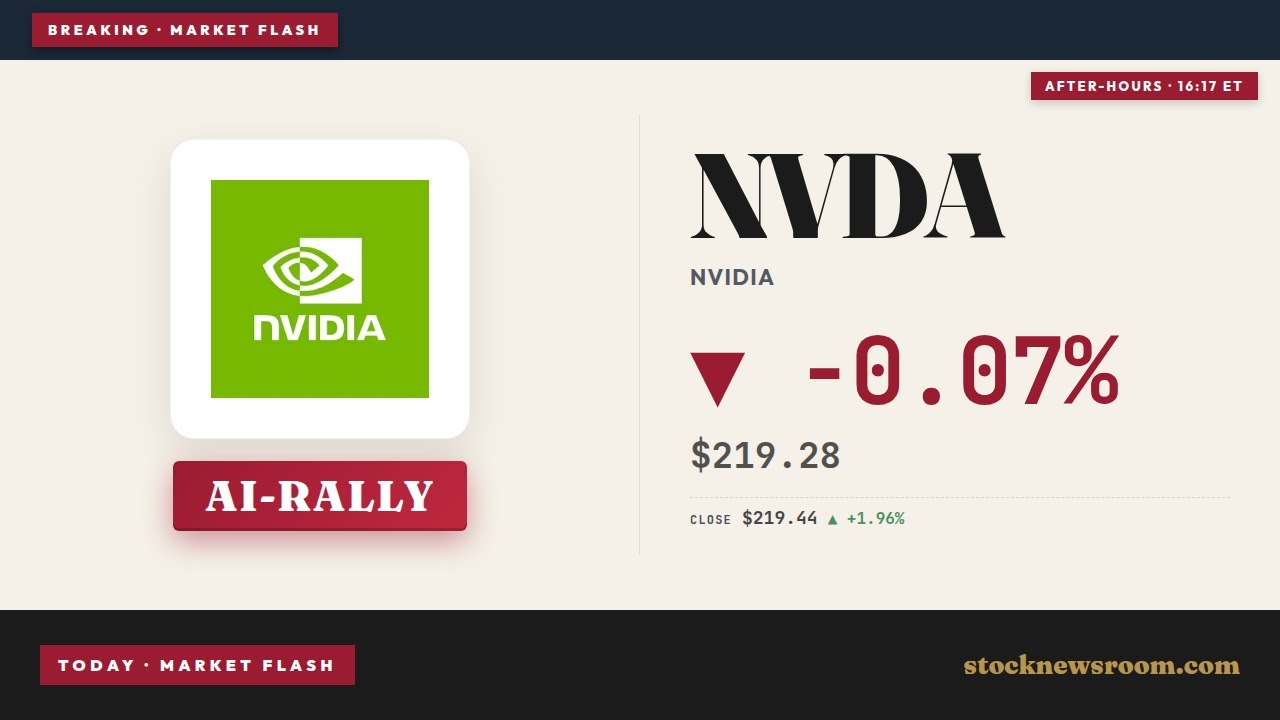

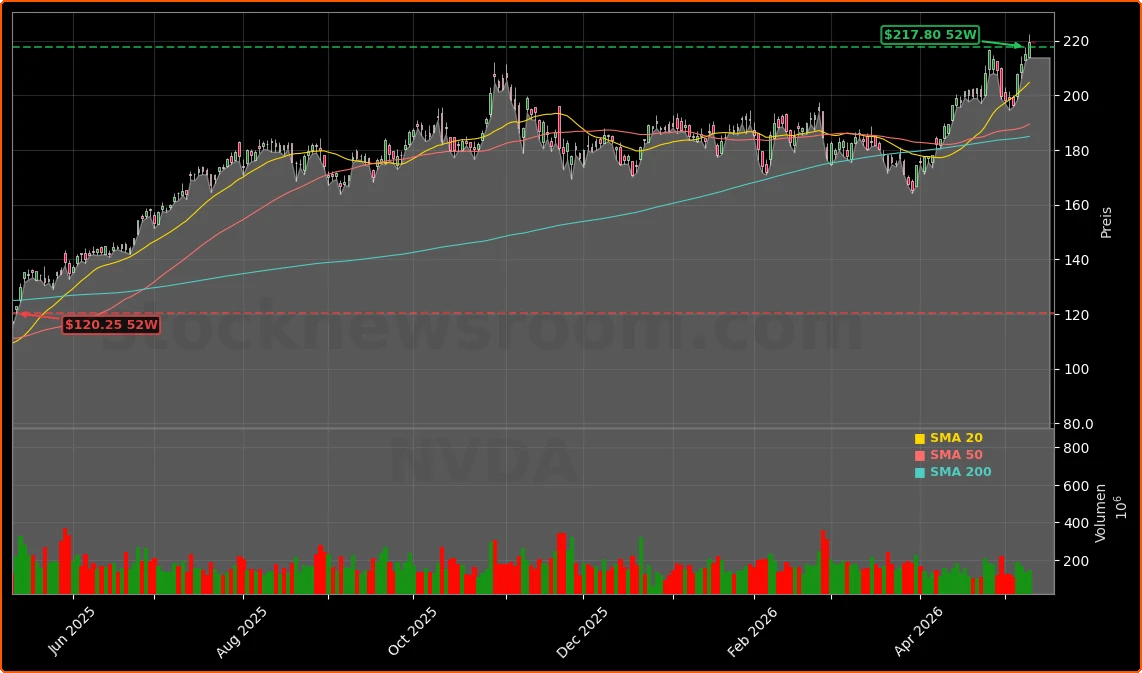

On Monday, NVIDIA (NVDA) finished the US session at $219.44, just below its recent peak around $217–$218 that marked a new NVIDIA Record high for the stock. The shares are up nearly 14% year-to-date and about 150% over the past year, making NVIDIA Corporation the single-largest weight in major benchmarks like the S&P 500 via SPDR S&P 500 ETF Trust and broad US funds from Schwab and Vanguard, where it now represents roughly 6%–8% of assets. Even a modest 2% daily move in NVIDIA can meaningfully sway the NASDAQ and S&P 500.

Behind the price action is an AI capex cycle that many on Wall Street compare to the telecom fiber buildout of the late 1990s, but with stronger current earnings. Hyperscalers are pouring well over $200 billion into accelerated computing, and NVIDIA is estimated to command roughly 80% market share in AI GPUs for training and inference. The Philadelphia Semiconductor Index has surged in recent weeks, with NVIDIA often described as the anchor of what some strategists now call a “semiconductor melt‑up.”

At the same time, institutional flows show early signs of profit‑taking. MarketBeat data highlights that Warm Springs Advisors trimmed its NVIDIA position by 4.8% in Q4 while still keeping it as its largest holding. Insiders including John Dabiri and Ajay K. Puri also executed sizeable stock sales, a reminder that even long‑term believers are locking in part of the NVIDIA Record rally.

How solid are NVIDIA and Alphabet at the top?

The market narrative is increasingly framed as a duel between NVIDIA and Alphabet for the top spot in global equity markets. NVIDIA’s market cap sits around $5.2–$5.3 trillion, while Alphabet is closing in near $4.8–$4.7 trillion. Alphabet’s stock is up about 26% this year versus roughly 16% for NVIDIA, helped by diversified cash engines in search, YouTube, cloud, and its Gemini AI platform.

Some investors argue that Alphabet’s broader base makes it a more balanced AI play, while NVIDIA is still heavily tied to one leg—AI data center infrastructure. Skeptics point to a gap between hyperscaler capex forecasts, often modeled near 10% growth, and the roughly 40% trajectory suggested by CEO Jensen Huang’s AI factory vision. If data center demand normalizes, that gap must close somewhere, and it is unclear whether the adjustment will fall on earnings expectations, capex budgets, or valuations across the AI complex.

Yet, for now, earnings are still backing the NVIDIA Record story. Wall Street expects around $78.6 billion in revenue for the upcoming report on May 20, implying roughly 78% year‑over‑year growth. Data center revenue alone recently topped $60 billion annually, with analysts projecting that NVIDIA could approach $370 billion in total revenue by fiscal 2027 if AI infrastructure spending remains on its current trajectory.

NVIDIA Record run powered by new partnerships?

Beyond pure chip sales, NVIDIA is aggressively locking in its position in the AI supply chain via large strategic partnerships. Earlier this month, the company signed a landmark deal with data-center operator Iren to support up to 5 gigawatts of NVIDIA DSX‑aligned AI infrastructure, centered on a 2‑gigawatt flagship campus in Sweetwater, Texas. The agreement includes a $3.4 billion AI cloud contract and a five‑year option for NVIDIA to purchase up to 30 million Iren shares at $70, representing a potential $2.1 billion equity stake. JPMorgan has warned that the economics look partly “circular,” as NVIDIA both funds and supplies the buildout, but the deal still underscores NVIDIA’s intent to anchor the next wave of AI‑native clouds.

NVIDIA is also investing directly in critical components for AI factories. A $500 million commitment to Corning, with potential to grow to $3.2 billion, will massively expand US-based fiber optic and connectivity capacity for future AI data centers. Corning plans to boost domestic optical manufacturing ten‑fold and add three new plants in the US, a move that both secures NVIDIA’s supply chain and strengthens American infrastructure. Separately, NVIDIA’s open-source NVIDIA Ising quantum AI models and CUDA‑Q platform aim to position the company early in hybrid quantum‑classical computing, expanding its reach beyond today’s GPU‑centric workloads.

On the software and ecosystem side, NVIDIA continues to embed itself in next‑generation robotics and industrial automation. Teradyne has partnered with NVIDIA to integrate its AI chips into collaborative robots (“cobots”), a bet that automation on factory floors will be the “next phase” of AI adoption. For investors, this broad ecosystem makes the NVIDIA Record rally less dependent on any single cloud contract or hardware cycle.

Can rivals dent the NVIDIA Record valuation?

Competition, however, is accelerating. AMD, Broadcom and in‑house chips from cloud majors like Apple, Microsoft, Amazon and Meta are all targeting slices of NVIDIA’s margin-rich GPU business. Seeking Alpha notes that ARM-based CPU offerings from NVIDIA itself, Amazon, and Google are set to reshape the server market, while a parallel “server CPU super cycle” benefits AMD, Intel and Qualcomm.

The newest headline rival is Cerebras Systems, which is preparing a high‑profile IPO under the ticker CBRS. The company’s wafer‑scale engine architecture, designed as an alternative to GPU clusters, has attracted a reported $10+ billion cloud deal with OpenAI and overwhelming IPO demand, with orders said to be more than 20x the available shares. While Cerebras remains far smaller than NVIDIA, its offering is another signal that customers are actively exploring alternatives to the incumbent, particularly for ultra‑large AI training jobs.

Investors must also consider geographic and regulatory constraints. NVIDIA is barred from selling its most powerful chips to China, the world’s second‑largest AI market by development activity. Local players such as Huawei’s Ascend line and domestic cloud providers are racing to fill that gap, while US data center projects face mounting pushback over power and water usage. Those frictions could slow the most aggressive AI buildout scenarios that underpin some of the loftiest NVIDIA Record valuation targets.

Related Coverage

For a deeper dive into how large infrastructure bets are shaping NVIDIA’s future, including the Iren deal and Corning partnership, see NVIDIA Infrastructure Boom: $3.4B IREN Deal Sparks NVDA Rally. That analysis explores whether the company is building an unbeatable AI empire or laying the foundation for a future bubble, and how those dynamics feed back into the broader semiconductor sector.

The NVIDIA Record story today combines near‑record share prices, dominant AI positioning and an escalating race with Alphabet for global market leadership. For US investors, the stock remains a core driver of index performance and a high‑beta expression of belief in long‑term AI infrastructure demand. The next few quarters of earnings, capex guidance and competitive responses will determine whether this NVIDIA Record era marks a sustainable new baseline or the peak of an extraordinary cycle.