Are Alphabet Earnings entering a new AI-fueled boom phase, or will massive capex and rising competition cap the upside?

How strong is the current Alphabet Earnings momentum?

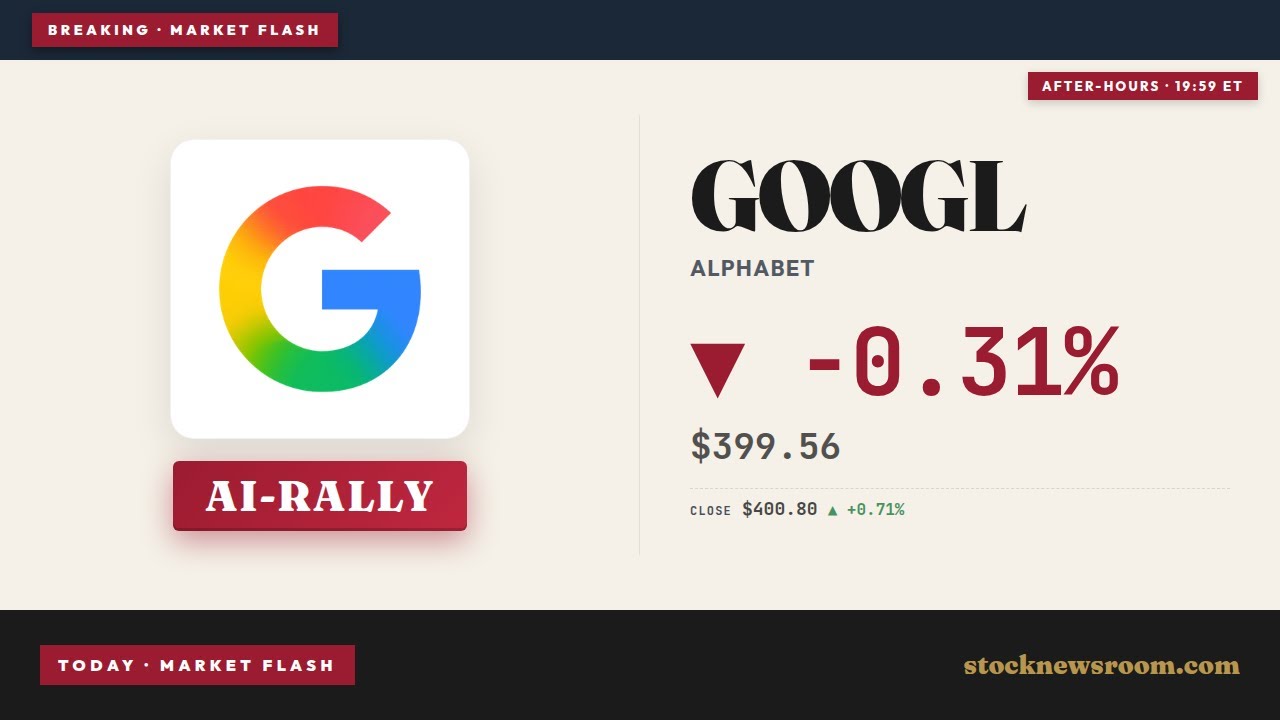

Alphabet Inc. (Google) has delivered a string of upside surprises, with the latest Q1 2026 Alphabet Earnings topping expectations on both revenue and profit. Class A shares have hovered near the $400 mark after that beat, closing Friday at $400.80, up 0.71% on the day, before easing to $399.56 in the late session. Class C shares finished at $397.05 and dipped to $395.80 after the bell, suggesting some short-term consolidation after a powerful multi-month advance.

The Q1 report highlighted just how central AI has become to Alphabet Earnings. AI-enhanced advertising lifted monetization in Google Search and YouTube, while Google Cloud turned in another quarter of robust top-line growth and expanding profitability. Analysts on Wall Street responded by lifting price targets and projecting mid- to high-teens earnings growth over the next few years, even as they acknowledged that AI infrastructure will keep capital expenditures elevated.

According to recent 13F filings, some institutional investors used the post-earnings rally to trim positions. Ruffer LLP cut its Alphabet stake by more than 80%, and Davidson Kahn Capital Management and Oakworth Capital also modestly reduced holdings. At the same time, most large banks maintain bullish views, and TipRanks’ AI-based analyst tool still labels the stock “Outperform,” with an average target around the low $400s, slightly above Friday’s close.

What is driving AI and Google Cloud growth at Alphabet?

The core of the bullish thesis behind the latest Alphabet Earnings is the company’s accelerating AI monetization. Alphabet’s Gemini model is now tightly integrated into Google Search, making it one of the most widely used consumer-facing AI systems worldwide. That integration supports more personalized, higher-value ad formats, directly feeding into the company’s largest profit engine.

On the enterprise side, Google Cloud continues to reshape the growth profile of the business. In Q1, the segment generated around $20 billion in revenue, up roughly 63% year over year, and $6.6 billion in operating income. That means Google Cloud already contributes more than 16% of Alphabet’s operating profit, and market research suggests cloud spending could grow above 20% annually through the next decade. The big three cloud providers — Alphabet, Amazon Web Services and Microsoft Azure — remain locked in a race to capture that demand, particularly for AI workloads.

Alphabet is also selling its custom Tensor Processing Unit (TPU) chips to external customers, turning Google Cloud into both a cloud platform and an AI silicon provider. That move puts it in more direct competition with NVIDIA and other chip players, but it also deepens Alphabet’s vertical integration and helps secure long-term AI compute contracts. Recent deals around large-scale data centers and cloud commitments, including massive AI-related capacity purchases by partners such as Anthropic, illustrate how central Alphabet’s infrastructure has become to the broader AI ecosystem.

How do rising AI investments and agents shape Alphabet Earnings?

Investors watching upcoming Alphabet Earnings are increasingly focused on the capex line. Wall Street expects the company, alongside Microsoft, Amazon, Meta Platforms and Oracle, to pour ever larger sums into data centers, networking and advanced chips. Rising long-term interest rates make that spending more visible: as Treasury yields climb, market valuations rely less on distant profits and more on near-term free cash flow, putting pressure on richly valued AI leaders to show discipline.

At the same time, Alphabet is leveraging its own AI to improve productivity. Management recently disclosed that roughly 50% of the company’s code is now written by AI agents and checked by human engineers. CEO Sundar Pichai highlighted the firm’s new Antigravity platform, which enables “truly agentic workflows” and “fully autonomous digital task forces” that help teams build products faster. If those tools reduce internal development costs and speed, they could offset some of the heavy AI capex and support future Alphabet Earnings.

Beyond software, Alphabet’s strategic investments offer potential upside optionality. The company holds an estimated 6% stake in SpaceX, giving shareholders indirect exposure ahead of a highly anticipated IPO. If SpaceX were to go public near a $1.75 trillion valuation and Alphabet monetized part of its stake, the resulting windfall could be redeployed into AI infrastructure or shareholder returns, adding another layer to the long-term narrative.

How does Alphabet stack up against other tech giants?

With a market cap approaching $5 trillion and a year-to-date gain above 25%, Alphabet is firmly entrenched among the mega-cap tech leaders that dominate the NASDAQ and S&P 500. Its advertising engine competes directly with Meta’s social platforms, while Google Cloud challenges Amazon and Microsoft in cloud and AI infrastructure. Alphabet’s recent move to initiate and then raise a quarterly dividend to $0.22 underscores its transition from high-growth disrupter to mature cash machine, though its payout ratio remains low compared with peers like Apple.

For U.S. investors, the key relative question is whether Alphabet’s AI exposure is more attractive than opportunities in other leaders, from NVIDIA’s chips to Tesla’s autonomous driving ambitions. Alphabet’s AI presence spans consumer search, cloud infrastructure, TPUs, Waymo robotaxis and even early quantum computing efforts available through the cloud. That breadth, combined with a strong balance sheet and still-reasonable valuation versus some AI peers, keeps the stock near the top of many long-term growth portfolios, even as some institutions tactically reduce positions after the recent run-up.

Related Coverage

Investors looking for more context on how big AI contracts can reshape the story should revisit our earlier piece on the Anthropic deal. In Alphabet Anthropic Deal $200B Surge Puts $GOOGL Near Record High, we explored how a massive multi-year cloud commitment helped push the stock toward record territory and reinforced Alphabet’s position as a long-term AI infrastructure leader. Together with the latest Alphabet Earnings trends, that analysis highlights why the company remains central to the next phase of the AI cycle on Wall Street.

With Antigravity, we are shifting to truly agentic workflows. Our engineers are now orchestrating fully autonomous digital task forces and building at a faster velocity.— Sundar Pichai, CEO of Alphabet

In summary, Alphabet Earnings remain firmly powered by AI-enhanced advertising and a rapidly scaling Google Cloud business, even as heavy infrastructure spending and higher rates introduce new trade-offs. For U.S. investors, the stock offers diversified exposure across consumer, cloud and next-generation AI platforms, backed by a strengthening dividend and substantial optionality in areas like SpaceX and Waymo. The next Alphabet Earnings report will show whether management can balance aggressive AI investment with disciplined cash returns, a combination that could keep the shares near the core of long-term growth portfolios.