Can Palantir’s latest surge hold if Pentagon demand and commercial AI growth keep outrunning valuation fears?

Why is Palantir Forecast improving?

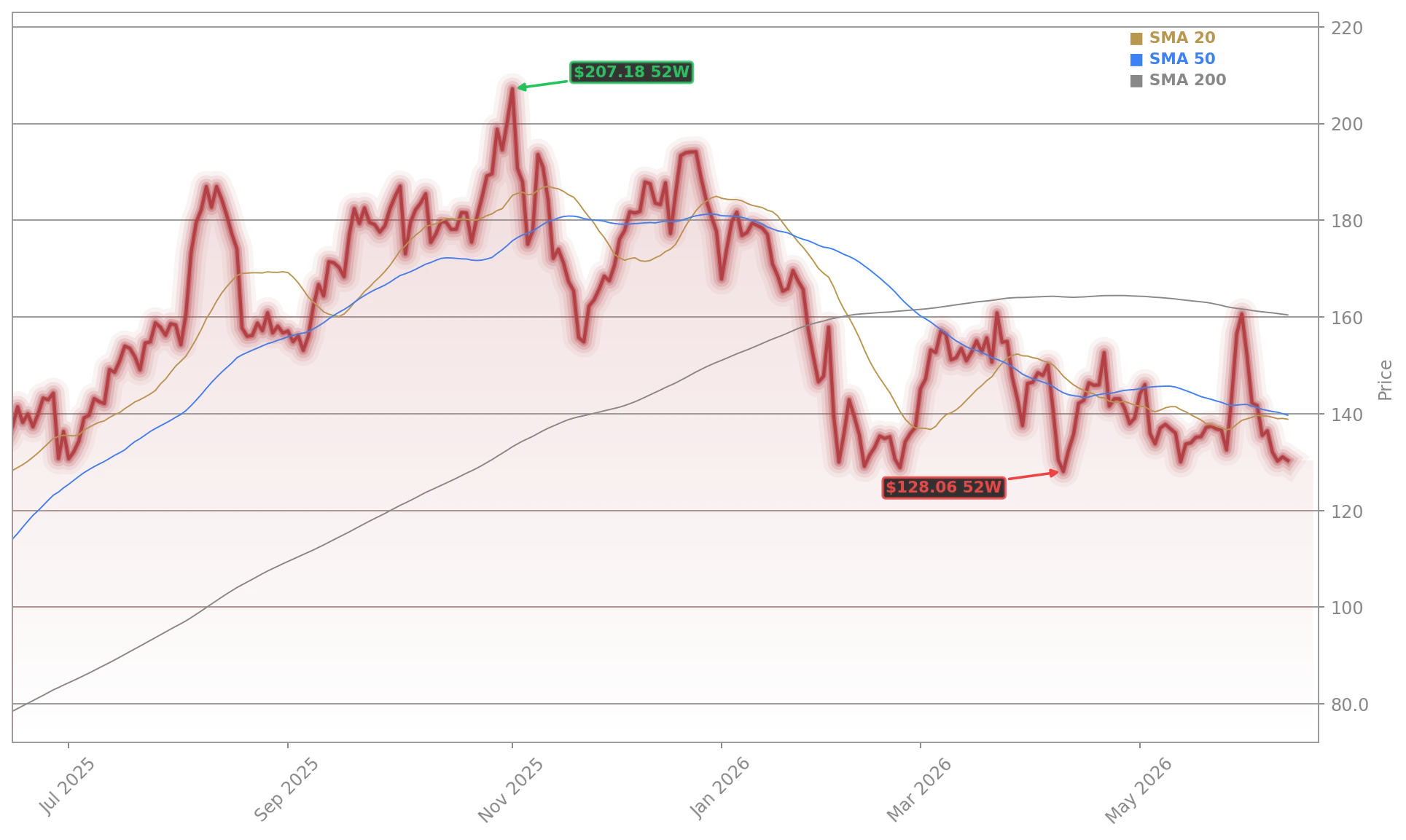

Palantir Technologies Inc. is regaining momentum after a strong bounce from the $126 to $127 area, a zone many traders now view as an emerging floor. The latest move follows renewed optimism around both government and commercial demand for the company’s AI-driven analytics platforms. That matters because the Palantir Forecast is increasingly tied to execution in two areas at once: federal contracts that provide long-duration revenue visibility and enterprise AI adoption that can accelerate top-line growth.

Management recently raised full-year revenue guidance to a range of $7.650 billion to $7.662 billion, up from a prior range of $7.182 billion to $7.198 billion. For the current quarter, revenue guidance stands at $1.797 billion to $1.801 billion. Those numbers reinforced the view that Palantir is still in a high-growth phase despite already commanding one of the richest valuations in large-cap software.

How important is Pentagon spending?

Government business remains central to the bull case. The Pentagon is requesting $2.3 billion to expand use of Palantir’s Maven Smart System, an AI-powered platform for battlefield analysis and AI-enabled targeting. Plans to classify Maven as an official program of record would make adoption across military branches easier and support a more durable funding stream.

That is only one part of the federal picture. Palantir software is also used across agencies including Immigration and Customs Enforcement, the State Department, Homeland Security, and the Internal Revenue Service. In Q1 2026, U.S. government revenue reached $687 million, up 84% from a year earlier. For investors, that scale helps explain why the Palantir Forecast remains closely tied to Washington budget trends.

Still, dependence on government work brings concentration risk. If defense priorities shift or procurement cycles slow, sentiment could change quickly, especially given how much growth is already priced into the shares.

Can commercial AI keep pace?

Palantir’s commercial business is now doing heavy lifting too. U.S. commercial revenue climbed to $595 million in the first quarter, up 133% year over year. The company also closed 206 deals worth more than $1 million, including 47 deals above $10 million. That deal flow suggests AI adoption is moving beyond experimentation and into larger production deployments.

This is where Palantir is increasingly compared with other premium software and AI names such as NVIDIA, Apple, and Tesla in investor discussions about market leadership and valuation discipline. Unlike chipmakers, however, Palantir sells decision software and workflow intelligence, which can create sticky recurring revenue if adoption broadens further.

The company is also extending its industrial footprint. Cleveland-Cliffs recently highlighted a new enterprise AI partnership with Palantir, underscoring how the platform is being positioned for operational efficiency use cases beyond defense and intelligence.

Is valuation still the main debate?

Yes. Even after the recent rebound, valuation remains the biggest point of tension in the Palantir Forecast. The stock is still discussed as expensive on conventional metrics, with a price-to-earnings ratio around 149. Yahoo Finance Singapore recently argued BILL offers the better value profile, while more bullish market commentary from Moomoo and The Globe and Mail emphasized momentum and thematic exposure instead.

At the same time, some bullish trading notes point to upside scenarios toward $190, implying roughly 32% potential from recent levels. Broader analyst sentiment also remains supportive, with 17 of 31 analysts reportedly rating the stock Strong Buy. No fresh price-target change from firms such as Citigroup or RBC Capital Markets was provided in the available material, but institutional investors are clearly watching whether raised guidance can support another rerating.

Related Coverage: Investors looking for a deeper valuation-focused angle can also read this analysis of whether Palantir’s AI growth can outrun its valuation test. That piece explores the same core tension now driving PLTR: exceptional revenue momentum versus increasingly demanding expectations from Wall Street.

The Palantir Forecast has turned stronger again as higher guidance, rapid commercial growth, and expanding Pentagon adoption support the bull case. For investors, the key question is no longer whether demand is real, but whether execution can keep outrunning a premium valuation. If Palantir continues landing large AI deals and converting government traction into long-term programs, the next leg higher could remain in play.