Can Palantir’s explosive growth story stop this selloff, or is valuation finally catching up with the AI favorite?

What’s Driving the Palantir Plunge?

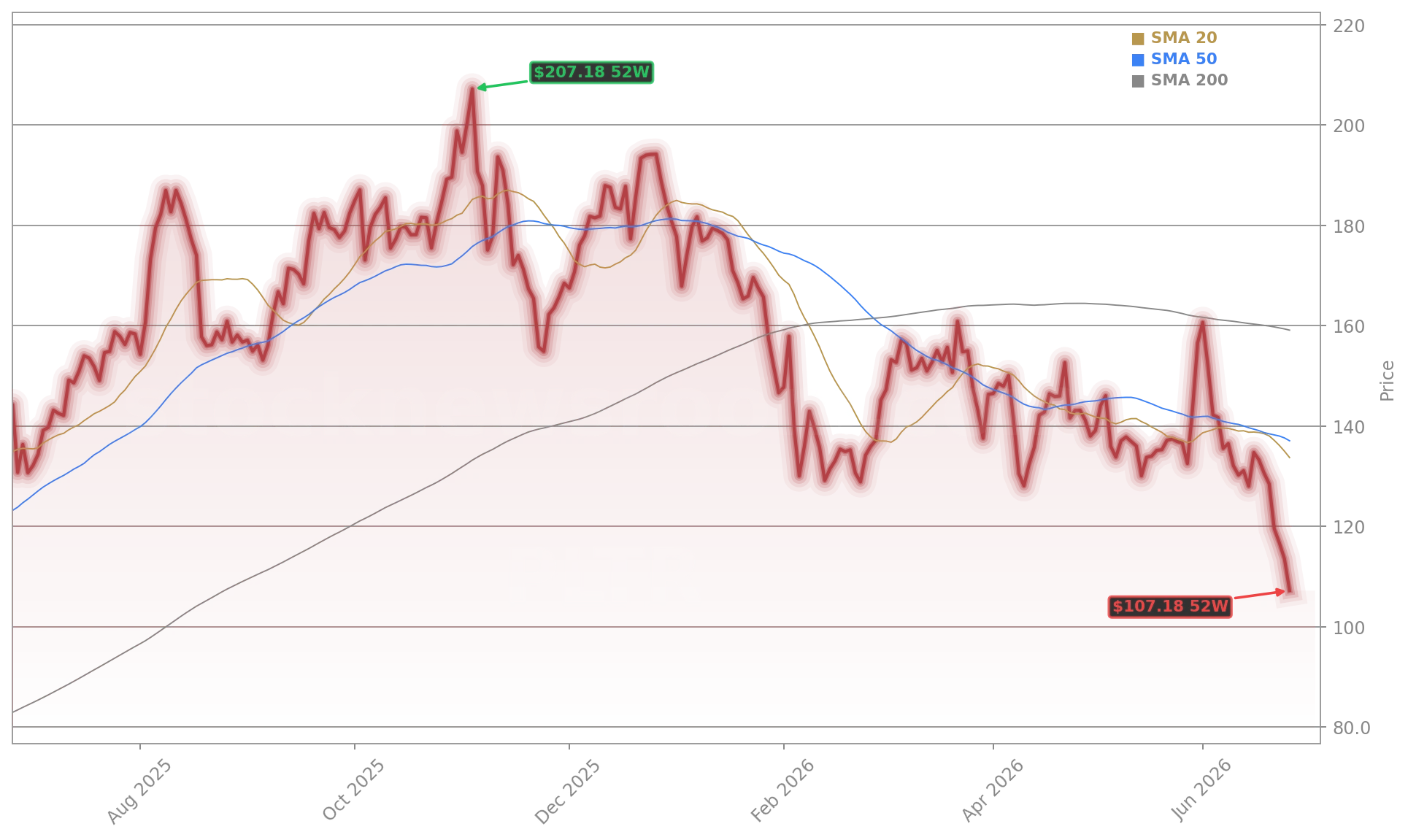

Palantir Technologies Inc. fell 4.49% to $107.66 on Thursday — its lowest close since April 2025 and a fresh 52-week low — extending a seven-day losing streak that has erased 19.48% of its value. The Palantir Plunge is not isolated: it’s part of a broader software selloff dubbed the ‘SaaSpocalypse’ by traders, triggered by rising interest-rate sensitivity, AI-driven competitive fears, and a sector-wide repricing of rich multiples. Palantir now trades at a trailing P/E near 144x and a free-cash-flow yield under 1%, leaving it exceptionally vulnerable to capital rotation away from high-multiple names. Unlike NVIDIA, which continues to benefit from AI infrastructure tailwinds, Palantir’s enterprise AI platform faces direct pressure from newer, API-first competitors like Anthropic — a dynamic highlighted by short-seller Michael Burry’s widely cited claim that ‘Anthropic is eating Palantir’s lunch.’

Why Are Fundamentals Not Supporting the Stock?

Q1 2026 results were unequivocally strong: revenue surged 84.7% year over year to $1.63 billion — the fastest growth in company history — with U.S. commercial revenue up 133% to $595 million and adjusted EPS of $0.33 beating consensus by 18%. Palantir raised full-year 2026 revenue guidance to $7.65–$7.66 billion and reported a staggering Rule of 40 score of 145%. Yet investors are ignoring fundamentals in favor of technical breakdowns and sentiment shifts. The stock has broken below key support levels — including $127, its February–June floor — and now trades 18.9% below its 20-day SMA and 31.8% below its 200-day SMA. Wolfe Research resumed coverage on June 16 with an upgraded ‘Peer Perform’ rating, affirming Palantir as ‘the most applied enterprise AI software company’ — but declined to assign a price target, citing valuation saturation.

How Are Competitors and Geopolitics Adding Pressure?

Palantir Technologies Inc. faces mounting headwinds beyond valuation: France’s domestic intelligence agency recently transitioned off Palantir’s tools to domestic provider ChapsVision, and the UK National Health Service contract — worth hundreds of millions — is under renewed scrutiny amid data sovereignty concerns and a 2027 break-up clause. Meanwhile, Anthropic’s usage-based, pay-as-you-go AI pricing model is reshaping enterprise procurement — offering faster deployment and lower upfront costs than Palantir’s ontology-driven, engineer-heavy platform. This competitive shift is echoed in market positioning: while Palantir’s Q1 commercial growth was robust, its shares are down 39% year-to-date, versus the Nasdaq Composite’s 9% gain and the S&P 500’s 7.8% rise. For U.S. investors holding tech-heavy portfolios, the Palantir Plunge underscores growing differentiation within the AI software space — where infrastructure leaders like Tesla and Apple face less direct disruption than application-layer platforms.

What Do Analysts Say About the $100 Threshold?

With Palantir Technologies Inc. now hovering just above $100 — a key psychological and technical level — Wall Street is divided on near-term direction. 24/7 Wall St. maintains a ‘BUY’ rating with a $150.02 price target (32% upside), while Citigroup recently reiterated its ‘Neutral’ stance citing ‘valuation risk outweighing execution strength.’ Morgan Stanley’s latest note warns that ‘the current multiple leaves no room for error’ despite strong cash flow generation. Meanwhile, RBC Capital Markets upgraded Palantir to ‘Outperform’ in early June, citing ‘unmatched government tailwinds and AIP scalability,’ but emphasized that ‘commercial monetization must accelerate meaningfully to sustain momentum.’ The consensus price target across 33 firms stands at $182.75 — implying 67% upside — yet the stock’s Accumulation/Distribution Rating remains ‘E,’ signaling heavy institutional selling. Technical indicators reinforce caution: RSI sits at 28.12 — deep in oversold territory — but momentum has yet to reverse.

What’s Next for Palantir Technologies Inc.?

The next major catalyst is Q2 2026 earnings, with management guiding to $1.797–$1.801 billion in revenue. Until then, Palantir Technologies Inc. will likely remain tethered to broader software sector sentiment and geopolitical headlines. Investors are watching whether the $100 level holds — or triggers a capitulation event that opens the door for strategic accumulation. Recent dip-buying by ARK Invest and improving U.S. commercial remaining deal value ($4.92 billion, up 112%) suggest underlying strength remains. Yet with shares down 40% in 2026 — Palantir’s worst year since its 2020 IPO — the Palantir Plunge has exposed a critical market question: can enterprise AI software sustain premium multiples without broader margin expansion and faster commercial scale?

Today, we see PLTR as the most applied enterprise AI software company, with the largest and fastest growth rates in the industry.— Alex Zukin, Wolfe Research

Related Coverage: Can the Palantir Zeta Partnership revive the AI growth story, or are investors too focused on valuation risk? Palantir Zeta Partnership -2.8% as Valuation Fears Grow. Meanwhile, Intel’s turnaround is impressive — but its valuation is pricing in massive foundry and AI execution success; Intel Goldman Sachs Coverage: $150 Target Meets Caution explores whether that optimism is justified.