Could Palantir’s latest AI alliance turn government demand into the next major growth engine for the stock?

What Does the Palantir AI Partnership Mean for U.S. Defense Tech?

Palantir Technologies Inc. and NVIDIA have jointly launched a sovereign AI operating system built to run Nvidia’s Nemotron open models inside secure, air-gapped government networks. Unlike cloud-based AI services, this architecture gives federal agencies full data ownership, real-time model customization, and audit-ready governance — critical for defense, intelligence, and civilian agencies managing 2 million employees across energy, transportation, and healthcare. The Palantir AI Partnership leverages Palantir’s Foundry for data integration and Apollo for model orchestration, while Nvidia supplies the hardware stack and open model foundation. This isn’t theoretical: early deployments with the Department of Defense and Department of Energy are already underway, targeting multi-year contracts that could scale beyond $500 million annually.

Why Did DA Davidson Upgrade Palantir Technologies Inc.?

DA Davidson upgraded Palantir Technologies Inc. from Neutral to Buy and raised its price target from $165 to $175 — citing accelerating cash flow, expanding commercial adoption, and strategic differentiation in the AI platform race. The firm notes Palantir’s adjusted free cash flow doubled year-over-year in Q1 2026, reaching $420 million, while recurring revenue grew 63% — ahead of CEO Alex Karp’s 50%–70% three-year guidance. Crucially, DA Davidson highlights Palantir’s unique professional services model: embedded engineers and ‘AI bootcamps’ drive faster workflow deployment than traditional SaaS sales, increasing customer lifetime value and contract expansion rates. At 50x cash flow — comparable to Snowflake and Datadog — but growing twice as fast, the firm calls Palantir ‘the best software company in the U.S. today.’

How Does Palantir Compare to Nvidia and Other AI Leaders?

While NVIDIA reported $81.6 billion in Q1 2026 revenue — up 85% year-over-year — Palantir Technologies Inc. posted $1.6 billion on the same basis, also up 85%. But the growth vectors differ sharply: Nvidia’s momentum remains hardware-led and infrastructure-scale, while Palantir’s is software-led and workflow-embedded. That distinction matters for portfolios. Nvidia trades at a forward P/E of 22; Palantir Technologies Inc. trades at 88 — reflecting higher growth expectations but also greater execution risk. Competitors like Tesla and Apple are building internal AI stacks, yet none offer Palantir’s sovereign, model-agnostic platform for regulated enterprises. In fact, Palantir’s ability to swap between Llama, Claude, and Nemotron — without vendor lock-in — is now a decisive advantage amid tightening U.S. export controls on AI models.

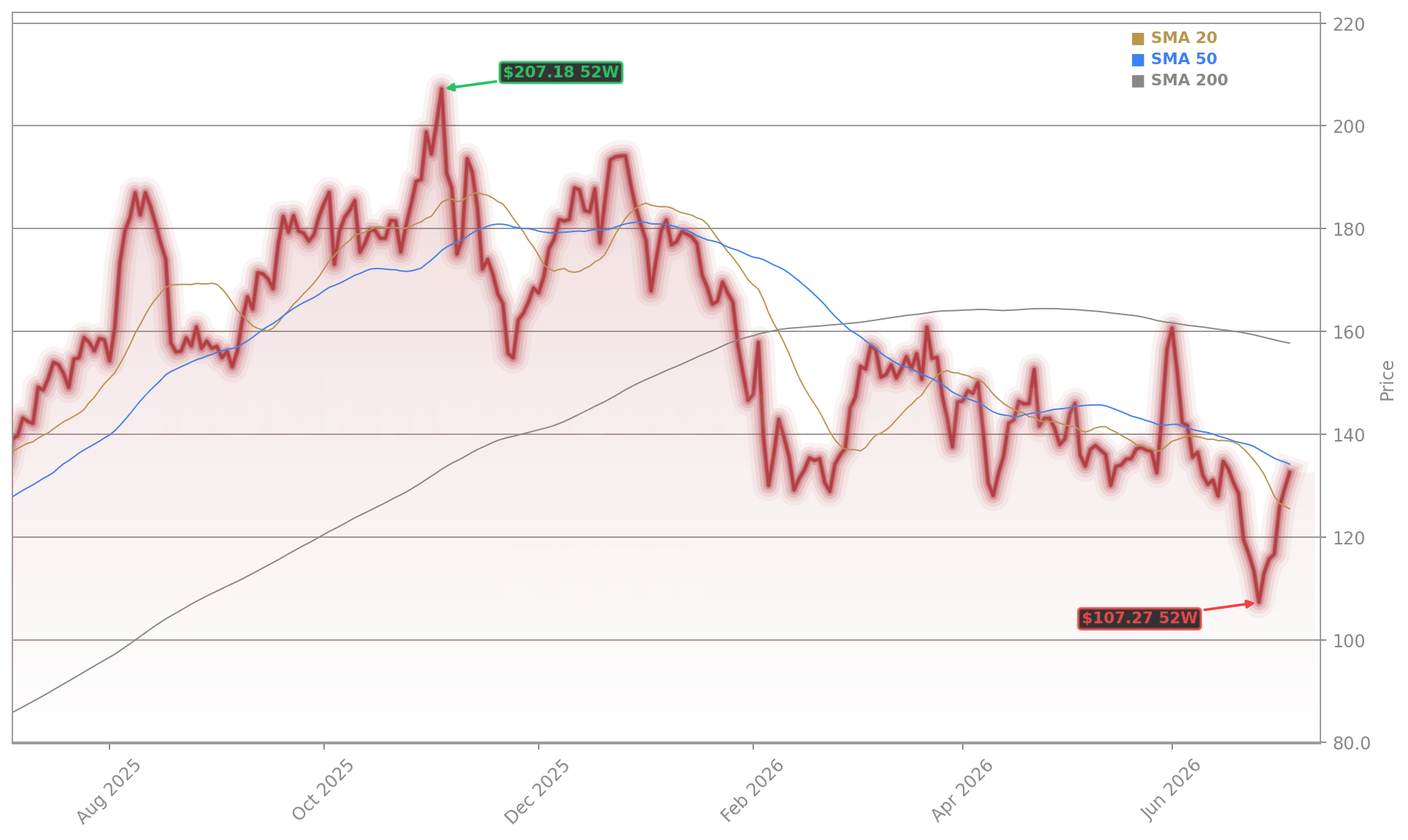

Is Palantir Technologies Inc. Still Overvalued?

At $132.54, Palantir Technologies Inc. trades at a forward P/S ratio of 64 — down from 92 in late 2025 but still steep. Yet DA Davidson argues the multiple is justified: if 85% revenue growth holds, the P/S ratio could compress to 36 in 12 months. More compelling is the cash flow trajectory: with $1.2 billion in cash and $320 million in quarterly operating cash flow, Palantir is now profitable on a GAAP basis — a milestone few hypergrowth software firms achieve before $2 billion in revenue. Investors should note that valuation pressure isn’t due to weakening fundamentals, but rather a market-wide recalibration of AI expectations — one that’s creating asymmetric upside for stocks with proven deployment velocity, like Palantir Technologies Inc.

What’s Next for Palantir Technologies Inc. on Wall Street?

With the Palantir AI Partnership now operational across federal agencies and commercial pilots expanding at Fortune 100 energy and financial firms, the next catalyst is Q2 2026 earnings — due August 5, 2026. Analysts expect continued revenue acceleration and margin expansion as AIP adoption deepens. RBC Capital Markets recently reiterated its Outperform rating, citing ‘unmatched workflow integration velocity,’ while Morgan Stanley added Palantir to its ‘Top AI Picks’ list for 2026. For U.S. investors, this isn’t just about one stock: it’s about positioning for the next phase of AI — where platform sovereignty, not just raw compute, defines competitive advantage. The Palantir AI Partnership is the first major proof point that this thesis is monetizing — and scaling.

Palantir may be the best software company, with cash flow doubling this year while the stock has fallen by about a third.— DA Davidson analyst

Related coverage: For deeper analysis on Palantir’s cash flow surge and DA Davidson’s upgrade rationale, see Palantir Upgrade: Buy Call After 57% Cash Flow Surge. That article breaks down how Palantir’s shift from services-led to platform-led growth is reshaping its margin profile — and why Wall Street may be underestimating its 2026 operating leverage.