Is Palantir’s latest upgrade the start of a deeper AI rerating, or just another sharp bounce in a volatile momentum trade?

Why Did DA Davidson Issue a Palantir Upgrade?

DA Davidson upgraded Palantir Technologies Inc. to Buy from Neutral on July 2, 2026, raising its price target to $175 — a 34% upside from Thursday’s premarket price of $130.33. The firm cited Palantir’s accelerating revenue growth (85% YoY in Q1), expanding 46% operating margin, and $4.3 billion free cash flow guidance for 2026. Crucially, DA Davidson emphasized Palantir’s unique ontology-driven architecture — which maps AI directly to physical operations and legacy systems — as unreplicable by large language model (LLM) pure-plays like OpenAI or Anthropic. This Palantir Upgrade joins recent bullish calls from Bank of America Securities ($181 target) and UBS, which called Palantir’s systems ‘uniquely complex’ and noted customers say ‘no LLM can replace Palantir for data workloads.’

What’s Driving the Technical Rebound?

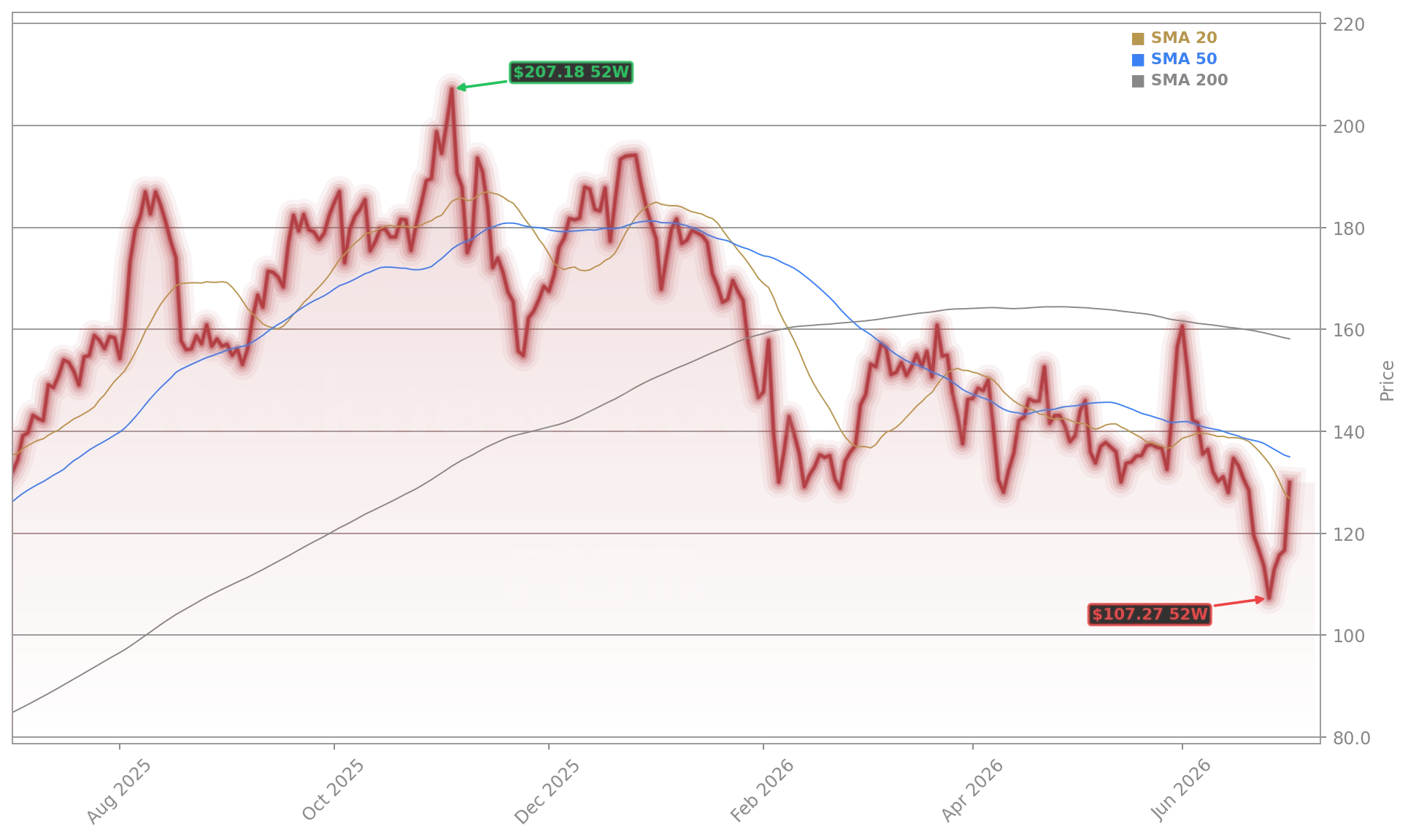

After falling over 30% year-to-date — underperforming the NASDAQ and S&P 500 — Palantir shares staged a sharp 20% five-day bounce, breaking above a key downtrend line near $106.37. Technical analysis shows heavy volume clustering between $130 and $140, suggesting strong institutional accumulation. While resistance at $126 remains critical, a close above $125.60 — the 21-day exponential moving average — confirms bullish momentum. The RSI sits near 50, neutral but poised for acceleration if the $135 and $162 levels yield. This rebound isn’t just momentum: it’s a rotation into high-conviction, cash-generative AI infrastructure — a category where Palantir Technologies Inc. stands apart from speculative LLM vendors.

How Is Palantir Redefining Enterprise AI Trust?

Palantir CEO Alex Karp’s July 1 CNBC appearance ignited Wall Street’s AI valuation debate. Calling token-based pricing ‘completely wrong,’ Karp argued enterprises fear losing intellectual property and competitive ‘alpha’ to frontier labs. His critique — echoed by Futurum Equities’ Shay Boloor and Moor Insights’ Patrick Moorhead — reframes Palantir not as an AI model vendor, but as the secure, sovereign infrastructure layer. That narrative gained traction with the July 1 announcement of Palantir’s partnership with NVIDIA to deploy secure, air-gapped AI models for U.S. government agencies — directly addressing Karp’s trust concerns. Meanwhile, Amazon Web Services’ $1 billion investment in Forward Deployed Engineering mirrors Palantir’s decade-old client-integrated model — validating its strategic blueprint.

How Does Palantir Compare to AI Peers on Valuation?

At $130.33, Palantir trades at a P/E of 131 — starkly above the S&P 500’s 32. But that metric misleads: Palantir’s PEG ratio is just 0.46, well below the 1.0 threshold signaling undervaluation. Contrast that with peers: Tesla’s AI efforts remain unmonetized at scale, while Apple’s AI rollout remains in early integration phases. Palantir’s $7.66 billion full-year revenue guidance — up 131% YoY — and $2.25 billion operating income target dwarf most pure-play AI software firms. Its 46x 2027 free cash flow multiple, per UBS, looks justified next to peers trading at 60x+ on slower growth. That valuation gap is closing — and the Palantir Upgrade signals Wall Street is catching up.

What’s Next for Palantir’s Growth Trajectory?

The basic view among enterprises in this country is ‘I’m going to chillax and waste my time with tokens, I’m going to get no value, and they’re going to get my IP.’— Alex Karp, CEO of Palantir Technologies Inc.

With Q2 2026 earnings due in early August, investors will scrutinize three vectors: federal contract wins (especially in defense AI), commercial enterprise adoption beyond financial services, and progress on the NVIDIA-powered secure AI stack. The $1 billion AWS FDE investment and Surf Air Mobility’s AI-driven SurfOS integration — detailed in Palantir Partnership: 85% Revenue Surge Tests Skeptics — suggest vertical AI monetization is accelerating. Meanwhile, Oracle AI Infrastructure -2.3% as $95B CapEx Sparks Debate highlights how capital intensity separates infrastructure builders from model vendors — a dynamic favoring Palantir’s capital-light, high-margin model. The next catalyst? Confirmation that Palantir’s ontology approach is becoming the de facto standard for AI governance in regulated sectors.