Can Meta’s aggressive AI spending spree supercharge long-term growth, or is it a costly gamble that will hit the stock?

How is Meta AI Strategy moving the stock?

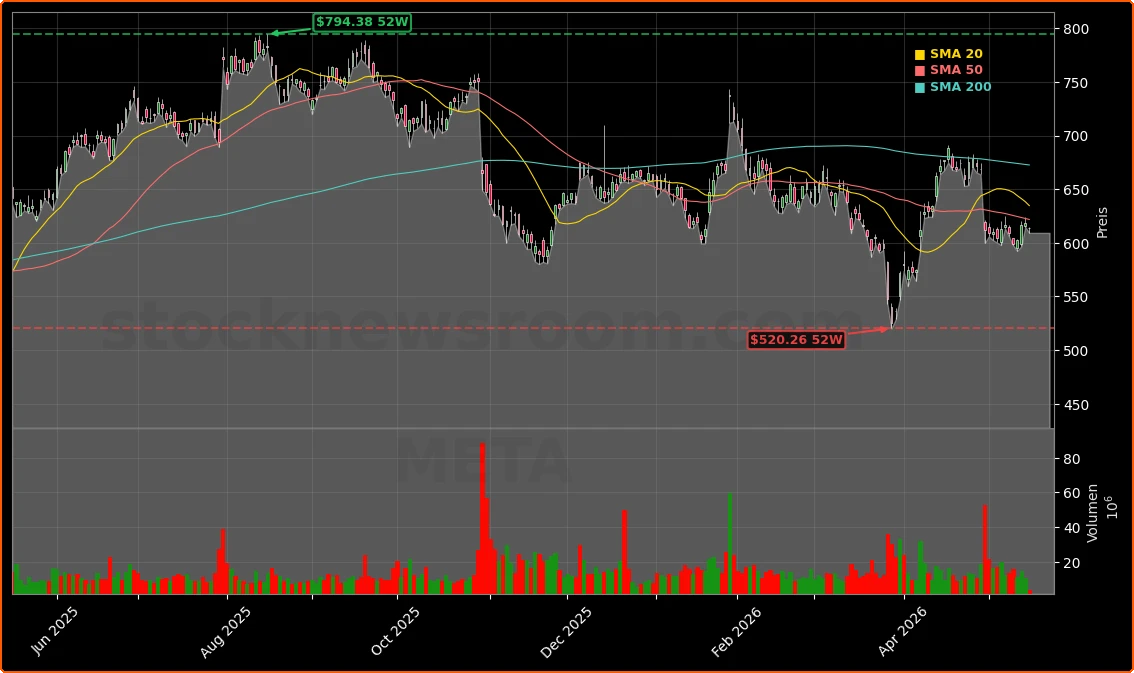

Meta Platforms, Inc. (NASDAQ:META) trades roughly 24% below its 52-week high after management doubled down on AI-related Capex, guiding up to $145 billion for the year versus about $72 billion last year. Friday’s intraday move of -0.72% to $613.96 reflects lingering anxiety that this spending wave could pressure free cash flow and crowd out buybacks, which dropped to zero in Q1 2026 after $12.8 billion of repurchases a year earlier. Yet the core business remains powerful: Q1 2026 revenue jumped 33% year over year to $56.3 billion, with operating margin at a hefty 41% and GAAP EPS up 62% to $10.44, keeping Meta firmly in the top tier of S&P 500 profit generators.

Despite the volatility, institutional investors continue to see long-term value in the Meta AI Strategy. Principal Financial Group recently lifted its position to about 3.81 million shares, worth roughly $2.5 billion, while Truist Financial also increased its stake toward 1 million shares. Overall, nearly 80% of Meta’s float is in institutional hands, a sign that big money is willing to ride out short-term Capex fears for potential AI upside.

What are analysts saying about Meta?

Analysts on Wall Street remain broadly constructive. MarketBeat data show a consensus “Moderate Buy” rating with an average price target near $840, implying substantial upside from current levels. Large houses such as Goldman Sachs, Morgan Stanley, and Citigroup have repeatedly highlighted Meta’s ad platform strength and improving AI monetization as key reasons to stay overweight mega-cap tech, even as interest rates remain elevated. One widely watched median target of about $817.50 suggests roughly mid‑30% appreciation potential versus the $600–$620 trading band seen in recent sessions.

Crucially, analysts are focusing less on near-term EPS dilution and more on whether the Meta AI Strategy can extend Meta’s lead in social and performance advertising. Meta’s Advantage+ and other AI-driven campaign tools are now central to agency and brand playbooks, alongside Google’s PMax. Performance marketers increasingly report that autonomous or “agentic” AI on Meta improves clickthrough rates and lowers acquisition costs, reinforcing the company’s pricing power in digital ads and justifying premium valuation multiples relative to much smaller rivals.

How is Meta’s AI spending changing the business?

Meta has pivoted from its costly metaverse bet toward a more grounded AI supercomputing build‑out. Management is deploying billions into new data centers, optical networking, and next‑generation GPUs, working with partners ranging from power producer Vistra to specialized equipment makers that enable light‑based data transmission. As a hyperscaler, Meta is competing head‑on with NVIDIA’s biggest customers—Apple, Alphabet, Microsoft, and Amazon—to secure enough compute to power large language models, recommendation systems, and next‑gen agentic AI.

On the product side, the Meta AI Strategy is visible across the family of apps. Models like Muse Spark, LLaMA, and Meta AI assist with content creation, feed ranking, and a new shopping mode that searches Facebook Marketplace and the wider web. In hardware, Meta’s AI-infused sunglasses and VR headsets are turning into important testbeds for on‑device assistants, with usage of AI smart glasses reportedly tripling year over year. These initiatives underpin Q1 metrics: ad impressions rose 19% and price per ad gained 12%, signaling both higher engagement and healthier demand from advertisers.

How does Meta compare with other mega-cap tech?

Within the NASDAQ mega-cap cohort, Meta’s spending arc mirrors that of Alphabet and Microsoft, but its revenue mix is more concentrated in advertising. Alphabet’s AI Capex is projected at $180–$190 billion this year, while Meta’s $125–$145 billion range puts it firmly in the hyperscaler elite. Both companies paused buybacks in early 2026 to fund data center expansion, raising questions about the durability of a key S&P 500 tailwind. Yet, unlike cloud‑heavy peers, Meta already converts ad dollars into exceptional net income margins near 48%, giving it more internal cash to redeploy.

On the competitive front, Meta’s ad scale and AI capabilities leave smaller platforms like Snap struggling to keep pace, while retail media players such as Instacart are choosing to integrate with Meta’s ecosystem rather than compete directly. For U.S. investors accustomed to viewing AI through the lens of chipmakers like NVIDIA or EV disrupters like Tesla, Meta offers a different angle: an ad‑driven, cash‑rich platform attempting to reinvent itself as an AI infrastructure and agentic‑marketing powerhouse inside the S&P 500.

What risks and signals should investors watch?

Key risks around the Meta AI Strategy center on execution and regulatory pressure. A Capex plan that pushes hyperscaler investment toward $700 billion industry‑wide could become a margin trap if AI monetization lags or if demand for training and inference compute normalizes. In that case, Meta’s stock could remain under pressure, especially with buybacks sidelined and some institutions, such as Bank of Montreal, trimming exposure.

Investors should track three datapoints: future Capex guidance each quarter, ad revenue growth relative to peers, and progress in AI‑enabled products like Meta AI assistants, Advantage+ automation, and smart glasses. Insider activity—such as a modest 10b5‑1 share sale by COO Javier Olivan—has been limited and programmatic so far, not yet signaling a broad management exit. With President Li Qiang recently hosting Meta leadership alongside CEOs from Apple and other U.S. tech giants, the company is also working to keep critical international markets, especially China, open for data center suppliers and ad clients.

Related Coverage

For a deeper dive into the infrastructure side of the story, readers can explore how Meta’s spending plans have evolved in “Meta AI Infrastructure $72B Surge Shakes Big Tech”, which examines whether escalating AI Capex will cement Meta as a supercomputing leader or compress margins over the next cycle.