Can Meta’s massive AI infrastructure splurge turn today’s profit machine into tomorrow’s dominant supercomputing platform—or a margin trap?

How does Meta AI Infrastructure reshape the AI arms race?

Meta Platforms, Inc. is emerging as one of the most aggressive buyers of high‑end AI compute. A long‑term agreement with Nebius commits Meta to as much as $27 billion of cloud‑based computing capacity over five years, effectively pre‑booking external data center power to complement its own build‑out. Together with in‑house investments, Meta has lifted its AI budget to as much as $72 billion for 2026, putting it in the same league as hyperscaler peers like Alphabet, Amazon, and Microsoft in absolute spend.

This Meta AI Infrastructure push is centered on training and serving large‑scale models such as Llama and the new Spark family, while improving the recommendation engines that drive engagement and ad performance on Facebook, Instagram, Threads, and WhatsApp. Meta is securing advanced servers built around NVIDIA GPUs and ARM‑based chips, while also experimenting with custom accelerators to reduce its long‑term dependency on third‑party silicon. For portfolio managers, that means Meta is no longer just an ad platform; it is quickly becoming a foundational AI infrastructure buyer whose capex decisions ripple across the entire semiconductor and cloud supply chain.

What is the financial impact for Meta?

Despite the soaring spend, Meta’s core business remains highly profitable. Recent quarterly results showed revenue growth of roughly 24% year over year at one point and 33% in the latest reported quarter, with operating margins north of 40%. That level of profitability gives management room to fund Meta AI Infrastructure without resorting to excessive leverage or sacrificing near‑term earnings entirely.

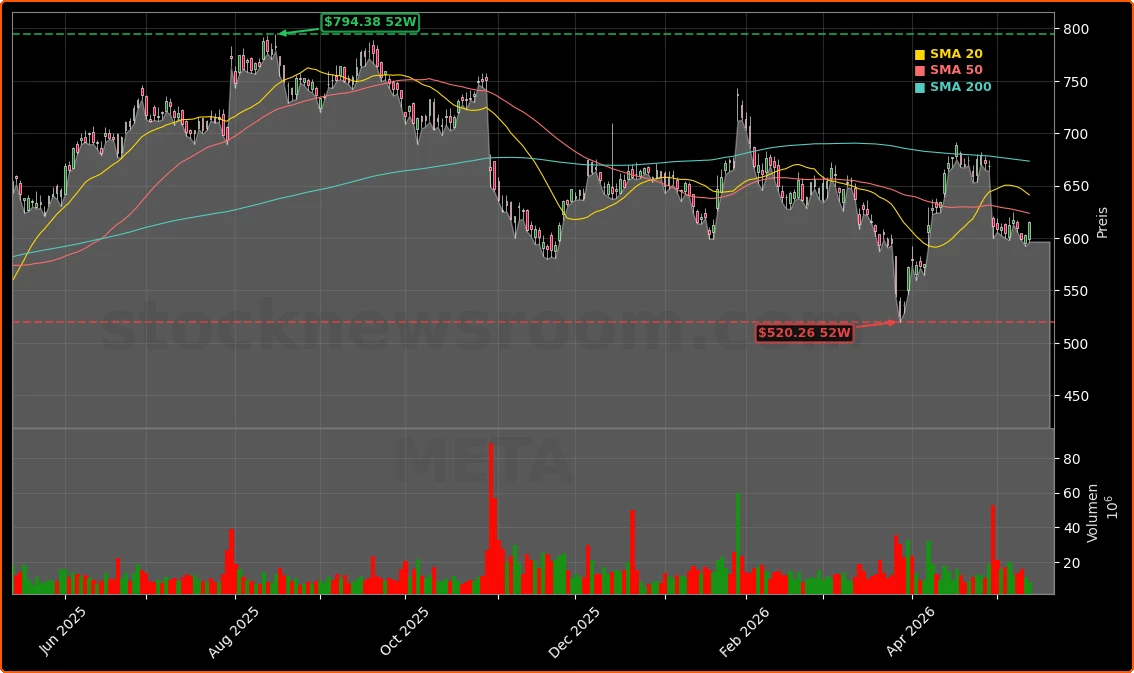

However, guidance for full‑year 2026 operating expenses implied an increase of about 40% versus the prior year, which triggered a sharp sell‑off after the last earnings release as investors recalibrated margin expectations. The shares briefly dipped below $600 before recovering toward the current $615 area. Some institutional holders, such as Baron Capital’s Durable Advantage Fund, highlighted that while the stock dropped roughly 13% in Q1 and about 8–9% over 12 months, the fundamental story remains intact: AI‑driven enhancements are boosting content recommendations, time spent, and ad conversion rates, partially offsetting the hit from higher depreciation and operating costs tied to new infrastructure.

On valuation, Meta still trades at around 19x expected forward earnings, cheaper than the S&P 500 despite faster top‑line growth than Alphabet and most mega‑cap tech peers. That discount reflects lingering market skepticism that Meta’s AI bets, including the Metaverse and Reality Labs efforts, will ultimately pay off.

How competitive is Meta against other AI leaders?

While Alphabet’s cloud and search businesses remain formidable, Meta has recently outgrown its rival on the top line, posting 33% revenue growth versus Google’s 22% in the last reported quarter. Meta’s advertising engine is clearly benefiting from improved AI‑based targeting and ranking, leading to higher return on ad spend for marketers and supporting higher pricing power across its platforms.

Beyond ads, Meta is pushing into hardware and new user experiences, including smart glasses and mixed‑reality devices, though these remain loss‑making. The company’s AI vision extends from social feeds into the Metaverse, where agentic AI could power realistic NPCs and personalized digital assistants. In parallel, Meta’s open‑source Llama ecosystem competes with closed models from OpenAI and Anthropic, creating an alternative for enterprises and developers who want more control and lower costs.

The talent strategy behind Meta AI Infrastructure has also been unusually aggressive. The company spent roughly $14 billion to acquire nearly half of Scale AI and recruit its co‑founder Alexandr Wang to lead a new Superintelligence Lab, reportedly offering some researchers compensation packages approaching $100 million. High compute per researcher and a promise of bold, well‑funded research agendas have lured top names from rivals like OpenAI and Apple. That raises execution risk—culture and focus must be maintained—but it also underscores how serious Meta is about competing at the frontier of AI.

What new revenue streams could AI unlock for Meta?

One near‑term experiment is WhatsApp Plus, a paid add‑on subscription at EUR 2.49 per month that layers premium features onto the company’s largest messaging app. While early and small in absolute terms, such moves illustrate how Meta can leverage AI to power advanced tools—such as smarter chatbots, business messaging, and commerce features—and then bundle them into subscription products. If even a fraction of WhatsApp’s user base converts, the incremental high‑margin revenue could help amortize Meta AI Infrastructure costs over a broader base.

Longer term, Meta envisions AI‑enhanced smart glasses and other wearables that bring its assistants into the physical world. These projects currently sit in the red within Reality Labs, but a breakout hit could materially alter Meta’s growth profile. In the meantime, the company is already using AI internally to automate workflows, analyze employee behavior data, and improve productivity—controversial steps that also highlight how deeply AI is embedded in Meta’s operating model.

Related Coverage

For a deeper dive into how Meta’s escalating capex plans could reshape its financial profile, readers can explore Meta AI Infrastructure Boom: Billions In New Compute Spend, which examines whether today’s investments lay the groundwork for a dominant AI platform or risk overshooting demand.

People joined because there was high compute per researcher, so they could make more progress than maybe they would be able to make wherever they were before.— Alexandr Wang, Head of Meta Superintelligence Lab

Meta AI Infrastructure is becoming a defining factor for the stock’s risk‑reward profile. The combination of a $27 billion Nebius compute deal, a potential $72 billion annual AI budget, and accelerating ad‑driven cash flows positions Meta as both a high‑capex infrastructure heavyweight and a cash‑generating consumer internet leader. The next few quarters will show whether this aggressive strategy drives sustainable earnings growth, but for long‑term investors focused on AI exposure, Meta’s scale and ambition make it a central name to watch.